Merchant Cash Advance

Get a merchant cash advance through Funding Agent and turn your card sales into fast, flexible funding. We match your profile to trusted UK providers, so you receive a clear offer, a fixed total to repay via factor rate, and repayments that move with your takings. No long forms, quick decisions, and support from a specialist when you need it. Start your eligibility check in 60 seconds.

- Quick and easy application process

- Loan disbursed within 24 hours

- No additional charges for early repayment

We Like To Keep Things Simple

to

£500K

zero hidden fees

What is a merchant cash advance?

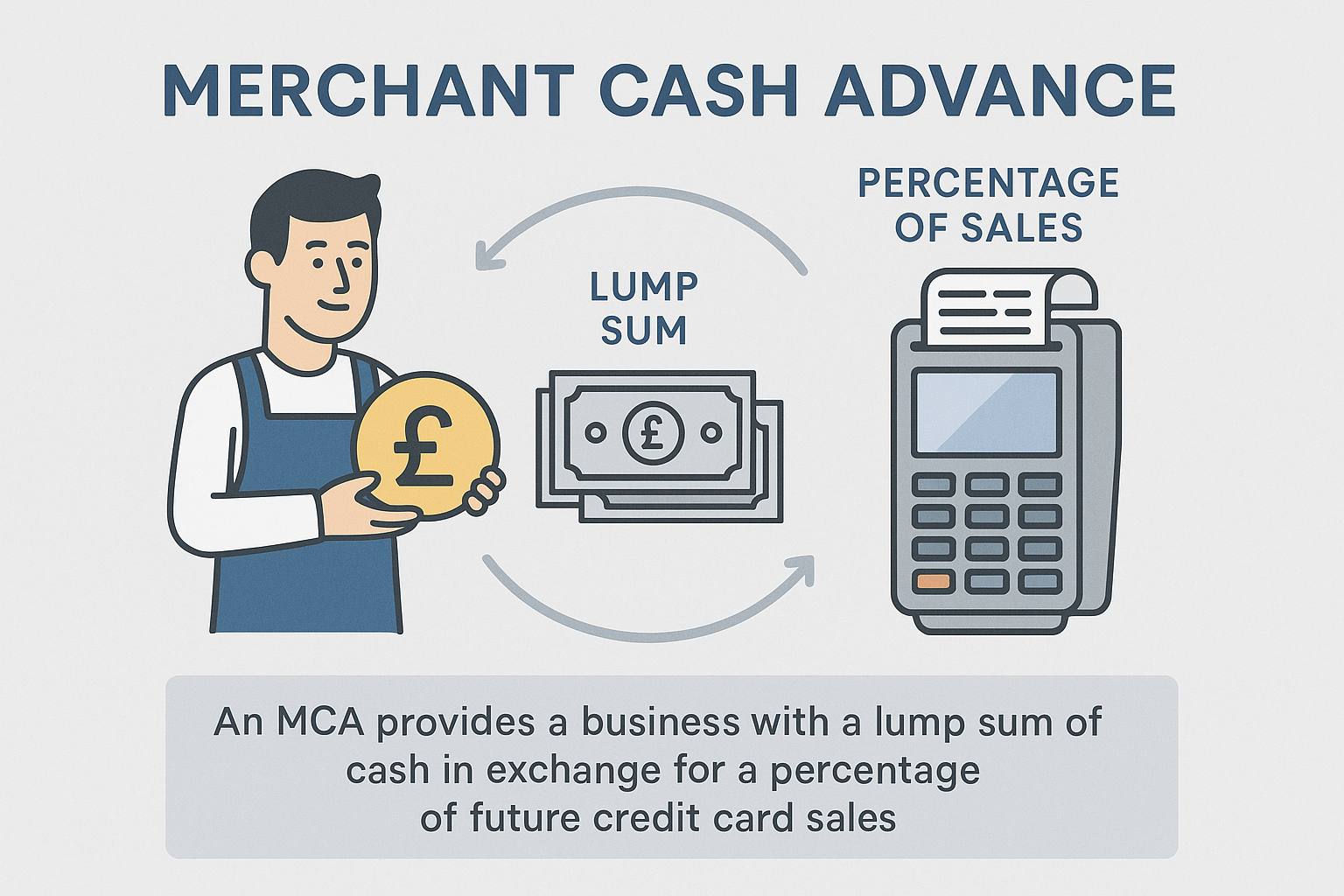

A merchant cash advance is financing that gives your business a lump sum now, then collects repayment as a fixed percentage of your card sales until a pre-agreed total is repaid. Instead of interest, pricing is set by a factor rate that determines the total you will repay. Because repayments rise and fall with your takings, MCAs can suit card-taking businesses that want speed, simple pricing, and flexibility during quieter trading periods.

How a Merchant Cash Advance Helps Your Business

A merchant cash advance provides fast working capital that moves in step with your takings. You receive a lump sum upfront, then repay as a fixed share of card sales until a pre-agreed total is cleared. This keeps cash flow steady during quieter periods and speeds up growth when trade is strong.

Heading

Heading

Test

Heading

TEST

Heading

Test

How a Merchant Cash Advance Works

With a merchant cash advance, your repayments are directly linked to your card sales. If your sales dip, your payments dip too. Here is how it works with Funding Agent:

Merchant cash advance pros and cons

Pros of a Merchant Cash Advance

Cons of a Merchant Cash Advance

- Higher total cost vs many loans: on an equivalent APR basis it can be pricier.

- Amount limited by card sales: advances are sized against recent takings, so caps can feel tight.

- Daily or near-daily collections: constant deductions can be tricky if margins are thin.

- Not a fit for cash or invoice-heavy firms: works best where card revenue is consistent.

- Less standardisation across providers: factor rates, holdback percentages, and terms vary, so comparisons matter.