Accelerated Payments vs 365 Finance Comparison

.png)

This guide compares Accelerated Payments and 365 Finance. It is written for UK SMEs weighing invoice-based funding against card takings finance. We look at products, costs, speed, and eligibility. The aim is to help you decide what fits your cash flow now.

Invoice funding vs card-takings finance: see where each lender fits

This dashboard turns the comparison into eight quick charts. Each tab shows a single view for Accelerated Payments and 365 Finance. Read ranges as bars and typical points as dots. Use it to judge price shape, usable amounts, likely timelines, and practical frictions. It helps a UK SME decide which route supports cash flow today and what to ask before you apply.

Products and Terms at a Glance

Accelerated Payments overview, loan sizes, fees, repayment style, terms, eligibility

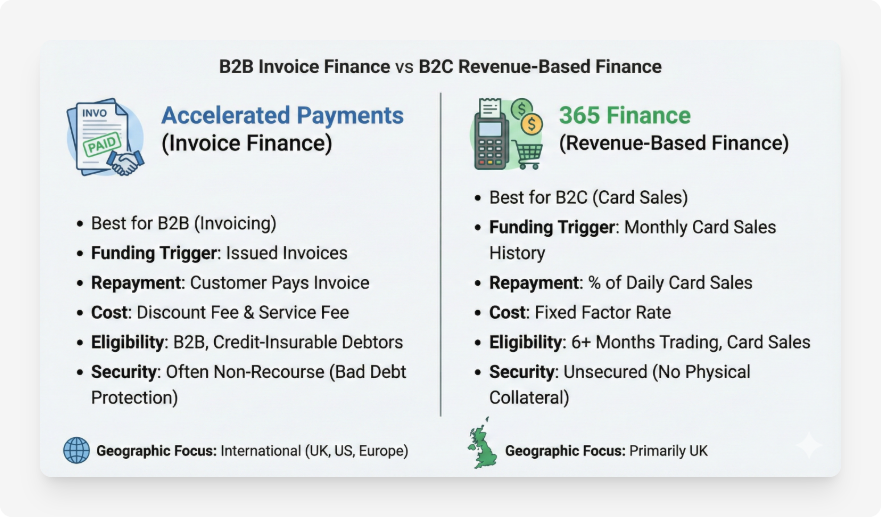

Product: Selective invoice finance on a non‑recourse basis. You choose which receivables to fund and when.

Typical facility and transaction sizes: Case studies show single receivables comfortably above £1 million are possible, with facilities in the £1–3 million range for suitable firms. Smaller SME deals are common too.

Pricing: Discount fee on the financed receivable for the days outstanding. May include a service fee. No personal guarantee stated for standard facilities.

Repayment style: Your customer pays the invoice into a designated account on due date. The advance plus fees are settled from that payment. No fixed monthly instalments.

Speed: Buyer approval and onboarding are streamlined. Decisions and funding can occur within 24 hours once receivables are approved.

Eligibility: Limited companies with c. £250k+ annual turnover, selling to credit‑insurable buyers in OECD markets. Export receivables supported. Sector agnostic.

Sources: Accelerated Payments product pages confirming selective receivables finance, non‑recourse structure, 24‑hour approvals, no personal guarantees, export capability, and large single receivable funding examples.

Pros of Accelerated Payments

- Non‑recourse structure can include bad debt protection on approved buyers.

- Select individual invoices. No need to finance the whole ledger.

- No personal guarantees stated for typical facilities. Useful for directors.

- Works for exports and multi‑currency receivables.

- Can fund large single invoices when concentration is high.

Cons of Accelerated Payments

- Best suited to B2B invoicing with creditworthy buyers. Retail or cash businesses may not fit.

- Overall cost depends on the time to payment. Slow‑paying debtors can raise fees.

- Requires buyer verification and eligibility checks, which takes coordination with customers.

365 Finance overview, loan sizes, fees, repayment style, terms, eligibility

Product: Merchant cash advance (revenue‑based finance) branded as Rev&U.

Advance size: Typically £10,000 to £500,000. Amount ties to monthly card takings.

Pricing: One fixed cost agreed up front using a factor rate. No APR. No fixed term.

Repayment style: A small pre‑agreed percentage of daily card sales, often 5% to 15%, is collected automatically until the balance is cleared.

Speed: Approval targeted within 24 hours, with funding into your account within days once approved.

Eligibility: UK trading for at least 6 months, and at least £10,000 per month in card sales. No asset security required. A personal guarantee is commonly required.

Sources: 365 Finance product and eligibility pages confirming £10k–£500k advances, 6 months trading, £10k+ card takings, fixed fee, and 5%–15% repayment percentage.

Pros of 365 Finance

- Repayments flex with sales. Slower months mean smaller deductions.

- No asset security. Set‑up and underwriting are lightweight for most SMEs.

- Single fixed cost known up front. No compounding interest.

- Quick decisions and simple application. Renewal and top‑ups available.

Cons of 365 Finance

- Cost per pound can be higher than bank loans. Factor rates vary by risk.

- Only suits businesses with strong card takings. Bank transfer or invoice‑heavy firms may not qualify.

- Daily holdbacks reduce cash received from card settlements until repaid.

Costs and Repayments in Practice

Pricing works differently. Invoice finance uses a discount fee on the value advanced against each invoice for the days outstanding. Some lenders add a service fee. A merchant cash advance uses a factor rate to set a single total repayable. Repayments happen as a share of daily card sales rather than a fixed monthly amount.

Worked example: Accelerated Payments (assumptions for illustration only). Your firm raises a £50,000 B2B invoice on 30‑day terms. You select it for finance and receive an 85% advance, so £42,500 on day 1. Assume a discount fee equivalent to 2.5% for 45 days (customer pays a bit late) plus a service fee of 0.5% of invoice value. Total fees ≈ £1,250 + £250 = £1,500. When your customer pays £50,000, the lender deducts the £42,500 advance plus £1,500 fees. You receive the remaining £6,000. Effective cost ≈ 3.0% of invoice for 45 days. This is an example only. Actual pricing varies by debtor risk and days funded.

Worked example: 365 Finance (factor‑rate model). You take a £50,000 merchant cash advance at a factor rate of 1.25. The total repayable is £62,500. Repayments are set at 12% of your daily card sales. If your card sales average £80,000 per month, 12% equals £9,600 collected per month. The advance would clear in roughly £62,500 ÷ £9,600 ≈ 6.5 months. There are no extra interest charges if you repay faster or slower. Cash received from card settlements is reduced by the holdback until the balance is cleared. This is an example only. Actual factor rates and holdbacks vary by risk and sector.

Speed and Service

Both lenders emphasise rapid decisions. Accelerated Payments highlights buyer approval and receivable funding in as little as 24 hours once invoices are verified. 365 Finance states decisions within 24 hours and funding within days after approval. Real‑world timelines can vary by how quickly you provide data and, for invoice finance, how quickly customers verify receivables.

Who Each Lender Suits

Typical scenario for Accelerated Payments

A manufacturing supplier invoices an approved UK retailer for £250,000 on 60‑day terms. The supplier wants immediate working capital to buy materials. Selective non‑recourse invoice finance releases cash on that single invoice, with bad debt protection tied to the buyer. It works even better for exporters invoicing OECD buyers in hard currency.

Typical scenario for 365 Finance

An established café group takes £120,000 per month via card terminals. A merchant cash advance of £80,000 helps fund a refurb and marketing. Repayments track turnover at, say, 10% of card sales, so quieter months are easier on cash flow. No asset security is needed. A director guarantee is usually required.

How to Apply

Application steps and documentation required for each lender

Accelerated Payments. Apply online. Provide company details, recent accounts or management information, debtor lists, and sample invoices. They approve buyers, then specific receivables. Expect to share invoice copies and proof of delivery. Once a receivable is approved and verified, funds can be advanced and settle when the debtor pays.

365 Finance. Apply online. Share trading history, card processing statements, bank statements, and ID for directors. If eligible, you receive terms showing advance size, fixed cost, and a proposed holdback percentage. On acceptance, funds are sent to your business account. Repayments are deducted from daily card settlements automatically.

Final Verdict: Which Lender Fits Your Business Best

Choose Accelerated Payments if…

- Your revenue is mainly B2B on credit terms and your customers are credit‑insurable.

- You want non‑recourse cover and to avoid personal guarantees where possible.

- You need to pick specific invoices to fund, including large or export receivables.

- You prefer repayment from debtor proceeds rather than fixed instalments.

Choose 365 Finance if…

- Your takings are mostly by card and at least £10,000 per month.

- You want a single fixed cost with repayments that flex with sales.

- You need fast, unsecured funding for inventory, refurb, or seasonal costs.

- You are comfortable with a daily holdback from card settlements until repaid.

Still unsure which route to take? Compare wider options like unsecured business loans, working capital loans, and term loans. Speak with Funding Agent or send the enquiry form. We will outline options and help you compare terms.

Sources

- Accelerated Payments: Selective Receivables Finance product page

- Accelerated Payments: How it works and 24‑hour approvals

- Accelerated Payments: non‑recourse and export references

- 365 Finance: Merchant Cash Advance main page

- 365 Finance: Eligibility and application guidance

- Capitalise: 365 Finance Rev&U ranges and repayment method

- BMCAA: 365 Finance eligibility snapshot and Trustpilot rating

- Moneyfacts: Invoice finance explained

- Swoop: Merchant cash advance calculator and holdback concept

- Merchant Savvy: Factor rate worked example

FAQs

Accelerated Payments generally provides more competitive loan interest rates compared to 365 Finance, but it is important to consider specific loan products as rates may vary.

Accelerated Payments requires businesses to have a minimum turnover, while 365 Finance may have more flexible requirements based on loan type and amount.

Both lenders charge fees, but Accelerated Payments may include fewer hidden fees compared to 365 Finance, making the costs more transparent.

Accelerated Payments is known for its quick application process, often approving and disbursing loans faster than 365 Finance.

Both lenders offer good customer support, but Accelerated Payments is commended for its proactive communication and personalised service.

Accelerated Payments offers invoice financing with flexible terms, while 365 Finance specialises in short-term business loans with rapid approval.