How AI Is Revolutionising Business Loans for UK SMEs

.png)

UK small and medium-sized businesses often need money fast. But traditional loans can take weeks and come with lots of paperwork. AI-powered business loans change this. They use smart computer programs and new data to judge credit risk in minutes, not days. They also help “thin-file” borrowers and cut costs for lenders. The Bank of England and FCA AI in Financial Services Survey 2024 shows banks are speeding up AI adoption. And the British Business Bank Small Business Finance Markets Factsheet 2024 reports growing SME demand for quick funding.

In this post, we explain AI loans and how they differ from traditional options. We share real success stories and show how the technology works. We list benefits and risks for SMEs and end with key trends shaping the future of SME finance. For more on alternative lending, see our UK alternative lending statistics guide.

What Are AI-Powered Business Loans?

AI-powered business loans use smart computer programs and new data sources to judge credit risk. Instead of only looking at past financial statements and credit scores, they use live bank transactions, cash-flow numbers and signals like online reviews. These AI models spot patterns that old systems miss. Borrowers get fast decisions and clear explanations. Lenders gain deeper risk insights and can automate most of the process. To learn more, read our What is Funding Agent? article.

Why AI Is Gaining Traction Among Lenders and Borrowers

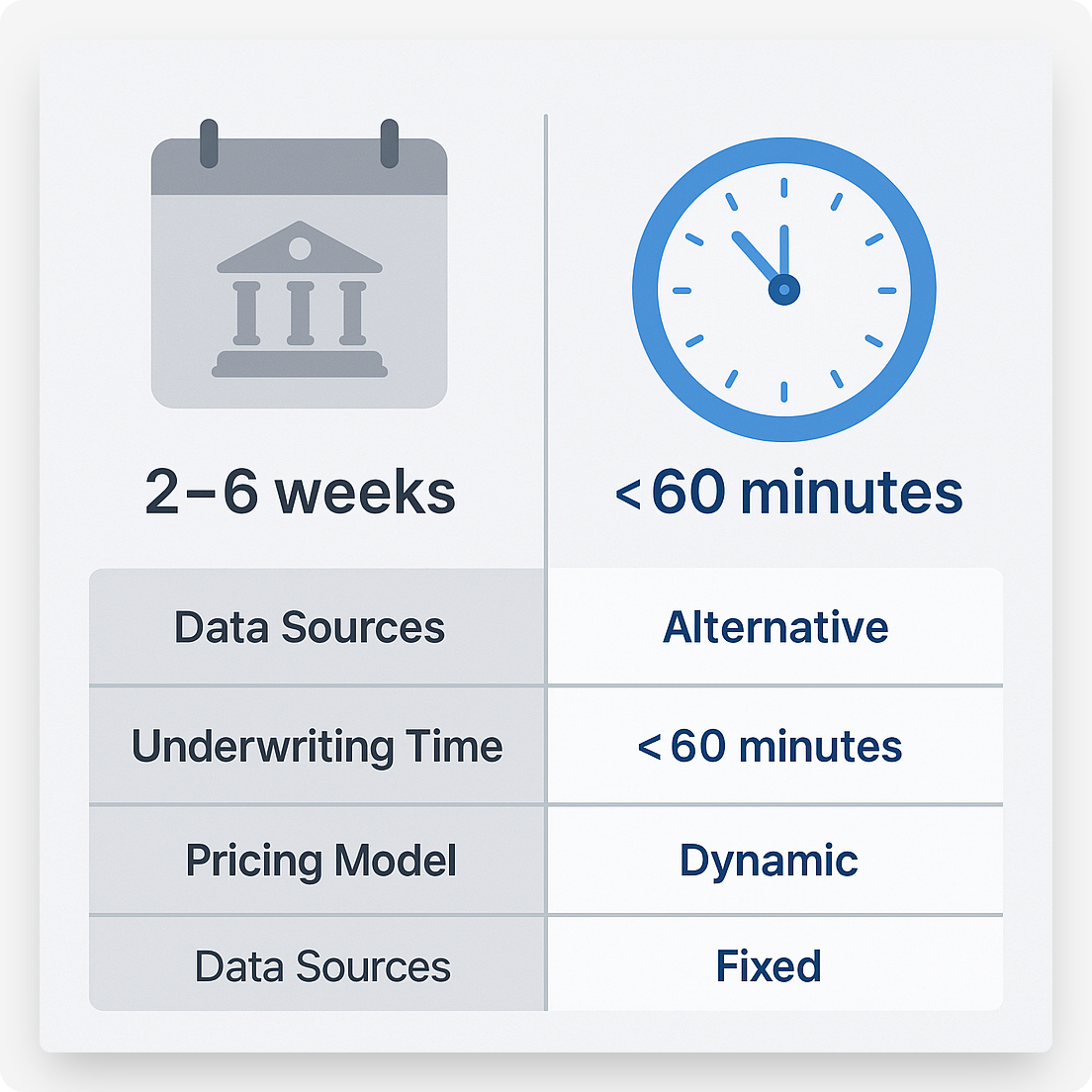

Speed, From Weeks to Minutes

Automated data pulls and instant scoring cut underwriting time from weeks to under an hour. SMEs no longer need to gather piles of documents or wait for manual reviews.

Inclusion, Serving Thin-File and Startup Portfolios

AI can assess businesses with little or no credit history. This opens funding to new or shifting companies.

Cost Efficiency, Cutting Manual Review Expenses

AI cuts manual tasks like document checks and risk calls. Lenders report up to 60 percent savings in processing costs. They can pass these savings to borrowers through lower rates or fees. Try our business loan calculator to see what you might pay.

AI Loans vs Traditional Bank Loans

Traditional bank loans rely on fixed credit scores, manual statements and collateral checks. AI loans use live data feeds, auto decision engines and constant monitoring. Below is a quick comparison:

Traditional bank loans rely on fixed credit scores, manual statements and collateral checks. AI loans use live data feeds, auto decision engines and constant monitoring. Below is a quick comparison:

Traditional bank loan approvals typically span multiple weeks or even months, depending on loan type and documentation requirements. For example, SBA 7(a) loans can take between 30 to 90 days to fund, and commercial lines of credit often require three to four weeks (21–28 days) for underwriting and approval.

According to the FDIC’s 2024 Small Business Lending Survey, three-in-four banks can approve a small and simple loan within five business days, while three-in-ten can approve one within a single business day.

By contrast, AI-powered platforms radically compress that timeline. Upstart delivers underwriting decisions in minutes and can fund loans in as little as one business day, OnDeck routinely provides small-business funding within 24 hours, and innovators like Iwoca report automated approvals in under three minutes.

Real-World Examples

Upstart: Machine-Learning Underwriting

Upstart analyzes over 1,500 data features, including education level, employment history, and bank-feed signals, to predict creditworthiness more accurately than FICO alone (PR Newswire). Its AI engine delivers approvals in minutes and dynamically adjusts credit lines as borrower performance data updates (GlobeNewswire).

OnDeck & Kabbage: Real-Time Credit Lines

OnDeck integrates accounting-software and bank-transaction data to underwrite small-business loans within 24 hours, offering lines of credit up to £250k with same-day funding for qualified firms (PR Newswire, Investopedia). Kabbage (American Express) similarly uses AI to monitor merchant sales in real time, scaling credit limits up or down automatically with revenue fluctuations (MarketsandMarkets, PwC).

Fundbox & LendingClub: Predictive Advances

Fundbox employs predictive analytics on accounts-receivable to auto-approve invoice-factoring advances within hours, based on AI-derived risk scores (MarketsandMarkets, industryarc.com). LendingClub’s marketplace uses machine-learning to match borrowers with investors, dynamically pricing risk across thousands of loans to reduce defaults and optimize yields (Yahoo Finance, Market.us).

Zest AI: Explainable Scoring

Zest AI delivers “explainable” credit scores by integrating thousands of variables ranging from payment history to device fingerprinting, while providing human-readable rationales for each decision (PwC). Clients see up to 15% more approved loans without increased losses.

OakNorth: Generative AI in Commercial Lending

OakNorth's Credit Intelligence Suite uses generative AI tools (in partnership with OpenAI) for digital deal structuring, real-time query handling, and bespoke loan documentation, enabling lending over £17 billion with high efficiency (Grand View Research, The Economic Times).

How AI Lending Works: The AI Lending Workflow

- Data Ingestion, secure APIs pull bank transactions, accounting records and digital footprints.

- Feature Engineering, the system turns raw data into key signs like revenue swings and average payment times.

- Model Training & Scoring, AI models learn from past data to spot future defaults and ensure fairness. For details, see How Aggressively Should a Bank Pursue AI?.

- Decisioning & Explanation, the platform gives an instant yes or no, plus top risk factors and a credit limit.

- Ongoing Monitoring, the system watches for signs like sudden revenue drops or market shocks. For more, read the OECD’s Financing SMEs and Entrepreneurs 2024 report.

Benefits for SMEs

- Predictable cash flow planning, fast decisions help you plan working capital with confidence.

- Flexible credit limits, limits adjust to your revenue so you avoid fixed caps.

- Transparent risk drivers, clear reasons help you see strengths and fix weak spots.

Risks and Safeguards

AI can carry bias if data is unbalanced. Top lenders run fairness audits and retrain models to treat all groups fairly. They follow GDPR rules and use strong encryption to protect data. Lenders also keep humans in the loop for unusual cases.

Model Bias & Fairness

AI can perpetuate historical biases in training data, leading to unfair declines or pricing for protected groups (arXiv). Explainable-AI frameworks and regular bias audits are essential mitigations (Grand View Research).

Data Privacy & Compliance

Aggregating extensive alternative data raises GDPR, CCPA, and sector-specific privacy challenges. Robust consent mechanisms and encryption are critical .

Systemic Risk

Widespread reliance on similar AI models could amplify market shocks, creating correlated risk exposures. Diversifying model architectures and retaining human oversight helps manage systemic vulnerabilities (arXiv).

Over-Automation

Purely algorithmic declines may overlook qualitative context (e.g., a one-time anomaly). Hybrid workflows that escalate edge cases to human underwriters preserve judgment where needed (PR Newswire, PwC).

Future Trends in AI-Driven SME Finance

Embedded finance will put AI loans inside accounting, e-commerce and ERP tools. Agentic AI assistants will guide you through funding via chat. Regulators will demand clear explanations, so lenders will build systems that show how they make decisions.

Embedded Finance Everywhere

AI-powered lending will be woven into non-financial platforms, from e-commerce sites offering checkout financing to B2B marketplaces embedding credit at point of sale (PwC, Yahoo Finance).

Agentic AI Assistants

Agentic AI systems will autonomously execute complex lending workflows, gathering docs, negotiating terms, and advising on optimal financing structures, with minimal human intervention (Grand View Research, Grand View Research).

Explainability & Trust

Demand for interpretable AI will drive adoption of XAI toolkits and regulatory guidance mandating transparency in credit decisions (Grand View Research, arXiv).

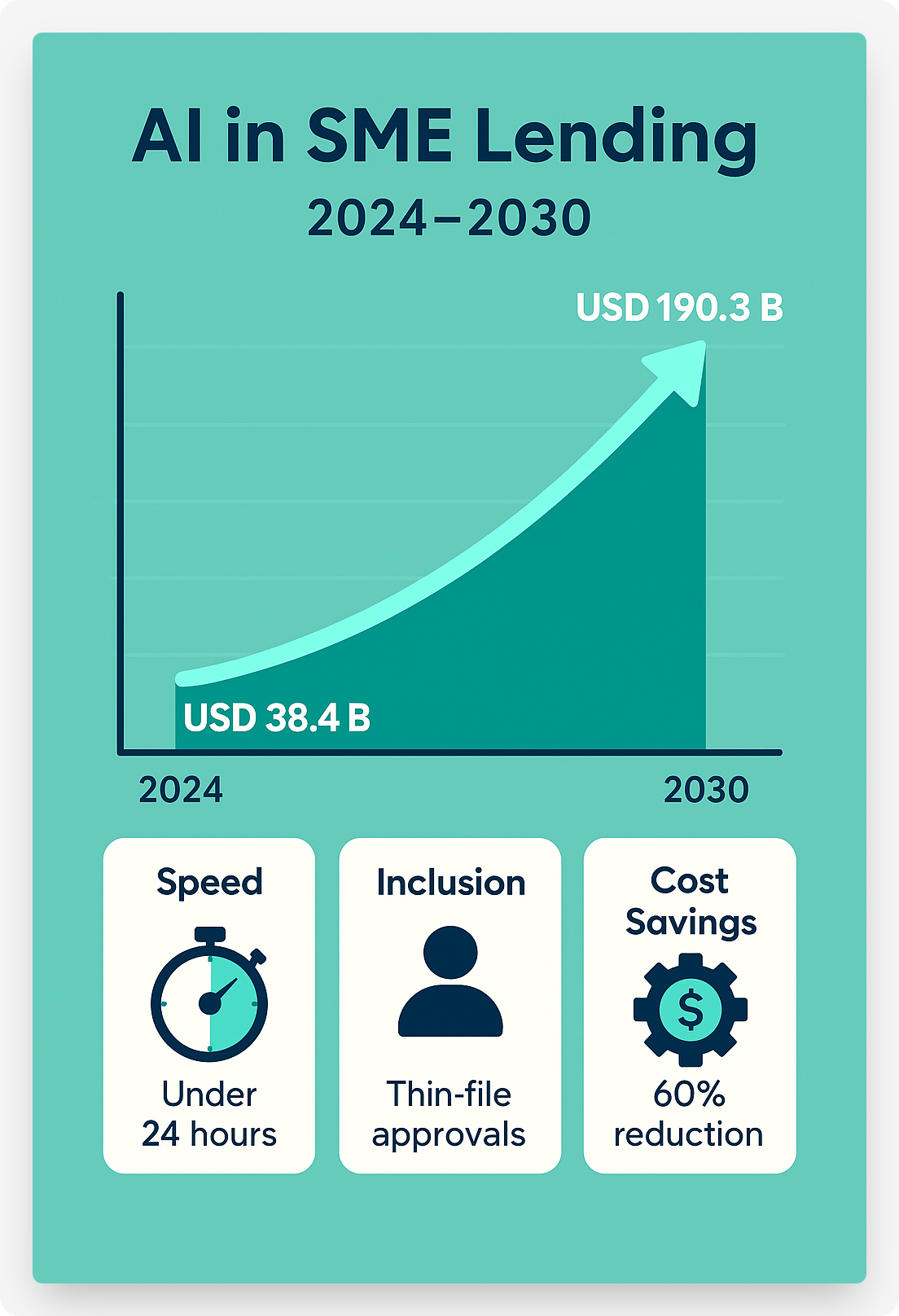

Market Growth

The global AI in finance market is projected to swell to USD 190.33 billion by 2030 at a 30.6% CAGR (MarketsandMarkets), while the AI-agents segment is set for a 45.4% CAGR, reaching USD 4.49 billion by 2030 (Grand View Research).

What Does This Mean For SMEs?

AI-powered loans are changing SME finance. They bring speed, more access and cost savings. UK businesses should check data security, model transparency and approval history in their sector. To learn more, see our guides on equity finance and asset finance. Early adopters will gain an edge with faster access to flexible capital.

At Funding Agent, our AI-driven platform removes the complexity of finding the right business loan, delivering personalised options in under 24 hours. Visit our Contact page to ask any questions, or complete our funding form to get matched with the best lenders today.