How to Use Business Loan Refinancing to Cut Costs and Strengthen Cash Flow

.png)

What is business loan refinancing?

Business loan refinancing is when you take out a new finance facility to pay off one or more existing business loans. You then repay the new facility instead of the old ones. The goal is usually to achieve better terms, such as a lower interest rate, a different type of facility or a longer repayment schedule that supports cash flow.

The British Business Bank describes refinancing as restructuring existing borrowing to change factors such as the repayment profile, the cost of debt or the security used. Refinancing can apply whether you have a single business loan or several different finance products in place.

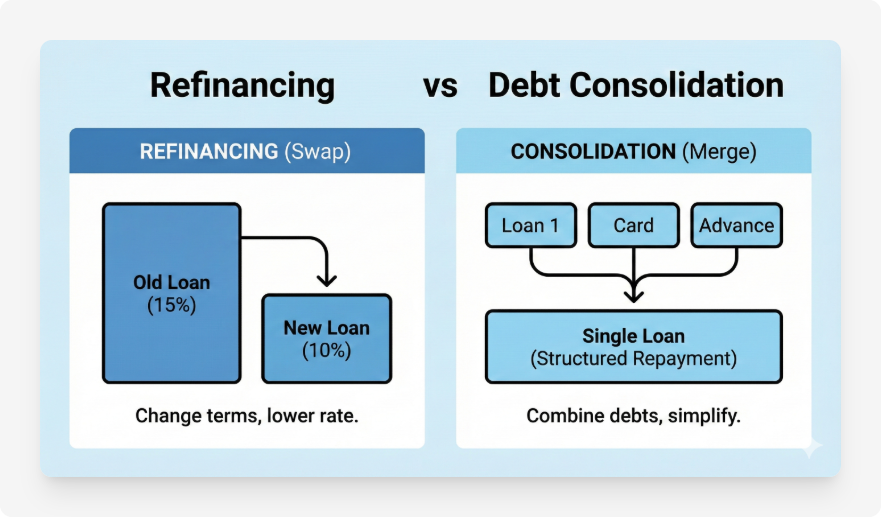

Refinancing vs debt consolidation

These two phrases are often used together but they describe slightly different strategies:

- Refinancing usually means replacing one existing loan with a new facility that has different terms. For example, switching an expensive fixed term loan into a cheaper variable rate loan.

- Debt consolidation usually means combining several separate loans or credit lines into a single new facility with one monthly repayment. As explained in the British Business Bank guidance on debt consolidation , this is often used to simplify budgeting and potentially reduce the overall monthly outgoings.

In practice, a refinance deal can do both. A single refinance facility might pay off several short term loans, credit cards and merchant cash advances so that you end up with one structured repayment schedule instead of many.

Why UK businesses refinance their loans

There is no single reason to refinance. Most UK SMEs consider refinancing as part of a wider plan to improve the quality of their balance sheet and free up cash for everyday trading or growth. Common goals include:

1. Reducing the cost of borrowing

The most obvious driver is to lower interest costs. If your business took out credit when it was younger or riskier, you may now qualify for sharper pricing. Moving from a high cost short term lender to a mainstream bank or specialist lender can cut the cost of debt significantly.

2. Improving monthly cash flow

Refinancing can extend your repayment term, spreading the remaining balance over a longer period. Even if the total amount of interest paid ends up higher over the life of the facility, the day to day benefit of lower monthly repayments can help stabilise cash flow and remove pressure from the working capital cycle.

3. Simplifying multiple debts into one repayment

Many businesses come out of a growth phase with several overlapping loans, for example a term loan, an overdraft, a merchant cash advance and perhaps a tax funding facility. Consolidating these into a single refinance loan can reduce admin, make cash flow planning easier and reduce the risk of missing a payment.

4. Changing the type of finance

Refinancing is also useful when the original product no longer fits how the business operates. Examples include:

- Refinancing a short term business loan into a longer term secured facility.

- Moving from an overdraft that is always at its limit into a structured term loan or cash flow facility.

- Switching from generic loans into asset backed finance, such as equipment finance or a commercial mortgage, which can sometimes support higher limits or lower pricing.

5. Releasing security or director guarantees

Some refinance deals are structured to change how the lending is secured. For example, you might refinance several personally guaranteed loans into one facility that is secured on a commercial property instead, or restructure lending so that guarantees can be shared across directors or limited to a lower amount.

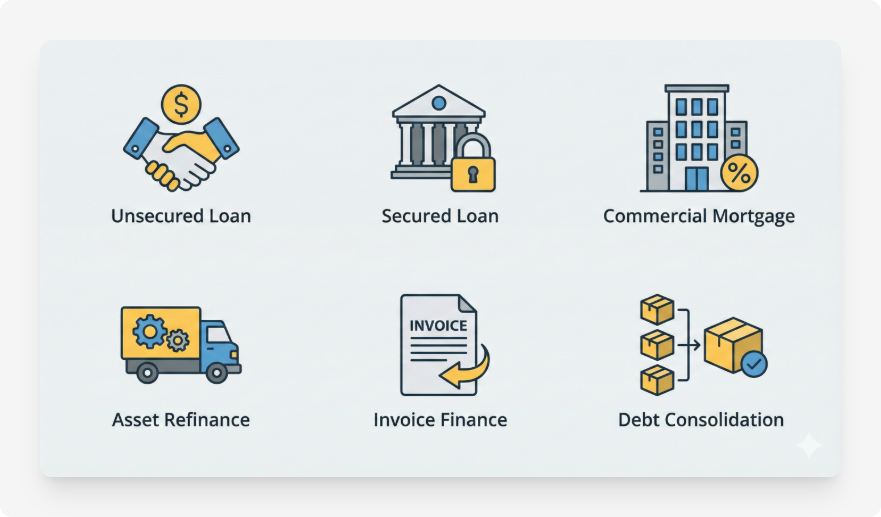

Typical business finance products used for refinancing

Different types of borrowing can be used to refinance existing debt. The right structure depends on what you are refinancing, the strength of your business and the assets available.

Unsecured business loans

Unsecured term loans are often used to refinance existing unsecured borrowing. They are normally based on the trading performance of the business rather than specific collateral, although many lenders will still ask for a personal guarantee from directors. These loans can be used to refinance expensive short term facilities or to consolidate several smaller loans into one.

Secured business loans

Secured loans are backed by specific business or personal assets, such as commercial property, vehicles or equipment. Lenders will typically advance a percentage of the asset value and may be willing to refinance existing borrowing with a longer term or lower interest rate if there is sufficient equity in the security.

Commercial mortgages and property refinance

If your business owns its trading premises or investment property, a commercial remortgage can be used to refinance existing loans or raise extra capital. Major high street banks and specialist lenders provide property backed refinance deals, which can combine an outstanding commercial mortgage and other unsecured borrowing into a single facility.

Asset refinance

Asset refinance involves borrowing against assets you already own outright, such as vehicles, machinery or equipment. The lender takes security over the asset and releases cash into the business, which can then be used to repay existing loans or overdrafts. This can be attractive for capital intensive sectors that have valuable equipment on the balance sheet.

Invoice finance refinancing

If you already use invoice factoring or discounting, it may be possible to refinance your ledger with a different provider that offers better advance rates or lower service fees. Some businesses also use funds released from invoice finance to pay down other short term borrowing.

Debt consolidation loans

Specialist consolidation loans are designed specifically to combine multiple existing debts into one facility. As guides from providers such as money.co.uk explain, these are often structured as standard term loans with a fixed monthly repayment over a set period.

When refinancing a business loan can be a smart move

Refinancing is not automatically positive, but there are common situations where it can be a powerful tool for UK SMEs.

Your current borrowing is clearly overpriced

If your existing facility was taken during a period when your credit profile was weaker, or through a high cost lender, the market may now offer lower rates. Comparing alternative offers against your current interest rate and fees is the first step to seeing whether there is a meaningful saving.

You are juggling multiple repayments

Where a business has stacked several short term loans, merchant cash advances or revenue based facilities, the total monthly repayment can become unmanageable. Consolidating these into a single structured facility can stop the situation escalating and provide breathing space for the business to stabilise.

Your business model has matured

Startups often rely on flexible but expensive products that are easy to access quickly. As the company grows, it may qualify for longer term funding from banks or specialist lenders on better terms. Refinancing is the mechanism that lets you move from early stage products to more sustainable long term debt.

You want to remove or reduce personal guarantees

If directors are carrying multiple unlimited guarantees, it can make it harder to raise further finance or plan exits. Refinancing into a facility with limited or shared guarantees, or one that relies on property security instead, can reduce personal exposure.

Situations where you should be cautious about refinancing

Refinancing is not always the right answer. In some circumstances, taking on a new loan could store up problems for later. Consider alternatives or professional advice if:

- Your business is already struggling to meet core liabilities such as PAYE, VAT or rent.

- The only refinance offers available involve significantly higher interest rates or heavy fees.

- You would need to offer essential business assets or personal property as security to replace unsecured debt.

- The main benefit is a lower monthly payment created by stretching the term far beyond the useful life of the asset or the timeframe for your current strategy.

The Rangewell guide to refinancing business debt points out that while refinancing can improve monthly affordability, it does not reduce the headline amount you owe and can sometimes increase the total cost if the term is extended too far.

Key costs and risks to analyse before you refinance

A thorough cost comparison is essential. Before signing a new agreement, work through these points carefully.

1. Early repayment charges and exit fees

Many business loans include early settlement fees if you repay before the end of the term. You may also face break costs on fixed rate facilities. Lenders and guidance sites such as money.co.uk stress that you should factor these charges into your savings calculation so that the refinance delivers a real net benefit, not just a headline rate reduction.

2. Arrangement, broker and legal fees

New facilities often come with arrangement or origination fees, sometimes expressed as a percentage of the loan amount. If you use a broker, there may be a separate fee or commission. For secured lending, you may need to pay valuation and legal costs as well. These should all be added into the total cost picture.

3. Total cost over the life of the loan

A refinance deal that cuts your monthly payments can still cost more overall if the term is significantly longer. To compare fairly, look at the total amount payable on your existing facility from today until the end of the term, then compare it with the total amount payable on the proposed refinance.

4. Impact on security and guarantees

Refinancing can change what is at risk if your business cannot repay. Moving from unsecured borrowing to a secured loan might reduce the interest rate but place your property or key assets at risk. Alternatively, you might be able to use refinancing to reduce personal guarantee exposure. Either way, document the before and after position clearly.

5. Alignment with your business plan

Finally, check whether the refinance supports where you want the business to be in two to five years. If you are planning to sell the company, take on investors or pivot into a new model, make sure the repayment schedule and covenants in your refinance agreement will not restrict those choices.

What lenders typically look for in a refinance application

From a lender perspective, a refinance application is similar to a standard business loan request. The provider will want to understand your current financial position and how the new facility will improve it.

- Trading history: many lenders prefer at least 12 to 24 months of trading, although some alternative lenders will consider younger businesses.

- Affordability: historic and forecast cash flow will be tested to ensure the new repayments are sustainable.

- Existing debt profile: the lender will review your current facilities, how they have been managed and whether there are any arrears or defaults.

- Security: for secured refinance, the strength and value of available assets will be assessed.

- Management and sector risk: lenders will consider the experience of the directors, as well as the risk profile of your industry.

Guides from providers such as Swoop recommend preparing full financial accounts, management information, bank statements, details of all existing loans and a clear explanation of how the refinance will strengthen the business.

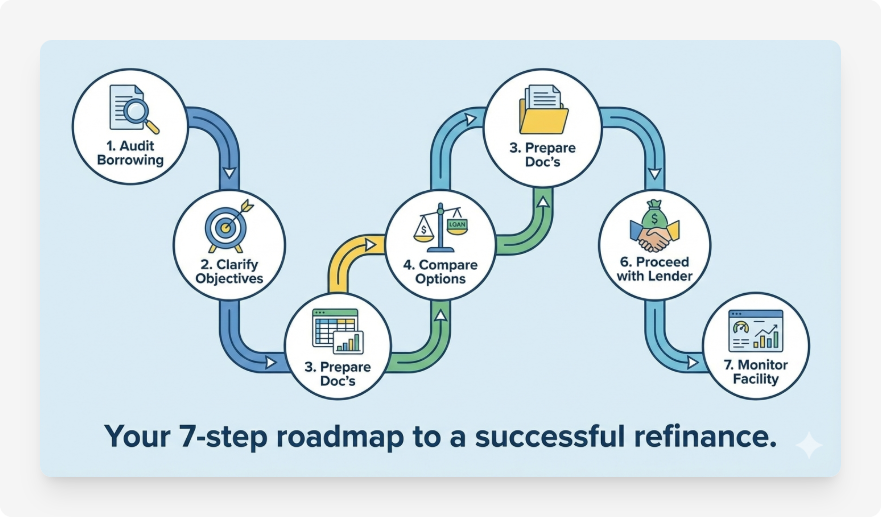

Step by step: how to refinance a business loan in the UK

The practical process can be broken into clear stages.

Step 1: audit your existing borrowing

List every facility in a simple table: lender name, outstanding balance, monthly repayment, interest rate, remaining term, security and any early repayment charges. This becomes the baseline for comparing potential refinance options.

Step 2: clarify your objectives

Decide what matters most. Is it reducing monthly outgoings, lowering total interest, simplifying admin, changing the security position or a combination of these? If you are not clear on your goals, it is harder to judge whether a proposal is actually an improvement.

Step 3: prepare your documentation

Gather recent bank statements, filed accounts, management accounts, a cash flow forecast, details of existing facilities and copies of any security documents or guarantees. Being organised will help lenders or brokers assess options quickly and can improve your chances of approval.

Step 4: compare refinance options

Approach multiple lenders directly, use comparison tools or work with an independent broker to explore the market. Compare interest rates, fees, security requirements, covenants and flexibility, such as the ability to make overpayments without penalty.

Step 5: model the before and after position

Use a spreadsheet or calculator to compare:

- Total monthly repayments before refinancing versus after.

- Total interest and fees payable over the remaining life of the current facilities versus the proposed new one.

- How security and guarantees change.

This step is where you can see clearly whether the refinance is delivering real value or simply shifting the problem into the future.

Step 6: proceed with the chosen lender

Once you are confident that a particular offer meets your objectives, move ahead with the full application and provide any additional information requested. After approval, the new lender will usually handle paying off the existing facilities directly or will provide funds for you to do so.

Step 7: monitor the new facility

After completion, keep the refinance under regular review. Monitor covenants, maintain strong financial reporting and make use of any flexibility to overpay if your cash flow improves. Treat the refinance as part of an ongoing funding strategy rather than a one off event.

Use a refinance calculator before you change lender

Before you sign a new agreement, it helps to model the numbers carefully. The Business Loan Refinance Calculator lets you plug in your current balance, rate and remaining term and compare them with a proposed offer side by side. You can see how monthly repayments change, how much interest you could save or add and how extending the term affects total cost.

If you are still exploring options, you can also test scenarios with the broader Business Loan Calculator and Unsecured Business Loan Calculator . For asset backed refinancing, try the Asset Finance Calculator or browse all tools on the calculator hub .

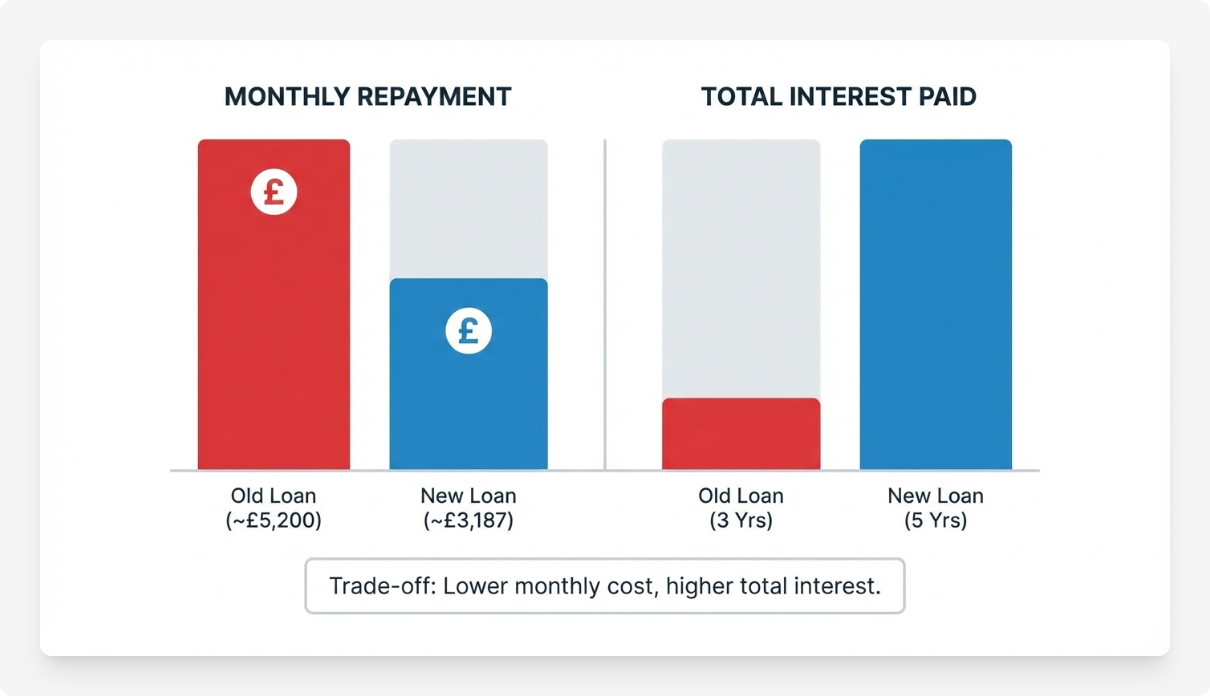

Worked example: how refinancing can change cash flow and total cost

To illustrate the trade offs, imagine a business with the following existing loan:

- Outstanding balance: £150,000.

- Interest rate: 15 percent per year (fixed).

- Remaining term: 3 years.

- Monthly repayment: approximately £5,200.

The business is offered a refinance loan with these terms:

- New balance: £150,000.

- Interest rate: 10 percent per year (fixed).

- New term: 5 years.

- Monthly repayment: approximately £3,187.

- Arrangement fee: 3 percent added to the loan.

In this scenario, the monthly cash outflow drops by just over £2,000, which could make a big difference to day to day liquidity. However, because the term is longer, the total interest paid over 5 years will still be substantial. The business needs to decide whether the cash flow relief and lower rate outweigh the extra years of repayments and the arrangement fee. Running the numbers clearly is crucial.

Recent trends in UK business refinancing

Recent reporting has highlighted a rise in UK SMEs looking to refinance expensive loans taken from alternative or non bank lenders, particularly where multiple short term facilities have been stacked on top of each other. Community development finance institutions and specialist lenders have been working with businesses to consolidate these debts into longer term, more sustainable structures while also providing additional working capital in some cases.

This trend underlines the importance of understanding the full cost and structure of any finance you take on. Refinancing can be a valuable way to repair a legacy debt position and stabilise the business, but it works best when it is part of a broader plan to improve profitability and cash generation.

Bringing it all together

Refinancing business loans in the UK can be a powerful way to reduce the cost of debt, stabilise cash flow and simplify the financial structure of your company. It can allow you to move away from legacy high cost facilities into more suitable long term borrowing that matches the current strength and strategy of the business.

The most successful refinance deals are those that are carefully planned. Start by auditing existing borrowing, defining clear objectives and preparing high quality financial information. Take time to compare offers from multiple lenders or work with a trusted broker, and pay close attention to total cost, security and covenants, not just the headline interest rate.

Handled well, business loan refinancing can form part of a broader plan to build a stronger balance sheet and support sustainable growth. Handled hastily, it can simply delay hard decisions or increase long term costs. Treat it as a strategic tool, run the numbers thoroughly and seek independent advice where needed, and it can help put your business on a firmer financial footing for the years ahead.

FAQs

Many facilities originally advanced under government guarantee schemes have now been refinanced into standard commercial facilities where the business case is strong. Lenders will consider each situation on its merits, and you should always check scheme terms and any early repayment conditions before proceeding.

Searching for and taking out new finance can lead to new credit checks, which may cause a short term dip in your credit profile. Over the medium term, successfully managing a well structured refinance and keeping up repayments should support your credit record, particularly if the refinance is used to clear previous arrears or reduce multiple short term debts.

Timeframes vary by lender and product. Some unsecured refinance loans can be approved within days if your documentation is ready, whereas secured property backed refinancing may take several weeks to allow for valuations and legal work. Building in some time for due diligence and comparison is usually worthwhile to avoid rushing into the first offer.

No. If fees are high or the term is much longer, you may end up paying more overall even with a lower rate. The key test is whether the refinance improves both the sustainability of your cash flow and the total cost relative to sticking with your existing facilities. In some situations, alternative actions such as negotiating with current lenders, reducing costs or raising equity may be more appropriate.

Eligibility depends on the lender and on your business profile. Most providers will look at your credit score, annual turnover, recent performance and trading history, and whether you are up to date on existing repayments. In general, the new facility must be used to refinance genuine business debt rather than personal borrowing, and lenders will want to see that the new structure is affordable on realistic cash flow forecasts. Eligibility criteria vary between high street banks, challenger banks and specialist lenders, so it is worth comparing offers rather than assuming that one answer applies across the whole market.

Before you refinance, it is important to look beyond the headline interest rate. Check for early repayment charges on your current facility, arrangement or broker fees on the new loan and any extra legal or valuation costs if the refinance will be secured on property or equipment. Compare the total amount you will repay over the remaining term of your existing borrowing with the total cost of the proposed refinance, including all fees, to see whether there is a genuine saving. You should also think about how the security and personal guarantees will change, and whether the new structure supports your longer term plans for the business. If you are already struggling to meet priority bills such as tax or rent, it may be more appropriate to seek independent debt advice before taking on further borrowing.