HSBC Vs Barclays: Business Loans Comparison

.png)

UK SMEs often compare HSBC business loans and Barclays business loans when they need working capital, equipment finance or a larger term loan. This guide sets out the differences in products, costs, speed, eligibility and service so you can choose with confidence. All facts are taken from current bank pages and reputable sources, and we explain where each lender tends to fit. If you want side by side numbers and worked examples, keep reading.

HSBC vs Barclays, quick decision dashboard

This dashboard compares rates, amounts, terms, speed, fees, arrangement charges, digital capability and ratings. Read each tab left to right, look for ranges then check the typical marker where shown. Use it to judge monthly impact, time to cash and service fit today. It helps a UK SME choose the lender that best matches risk, documents, and timeline. Pair the visuals with your own affordability and security position.

Products and Terms at a Glance

HSBC overview, loan sizes, fees, repayment style, typical terms, eligibility

Small Business Loan (SBL). Fixed-rate loans £1,000 to £25,000, 12 months to 10 years, with representative APRs of 11.3% up to £10k and 8.6% over £10k. HSBC states no arrangement fee, fixed monthly repayments, optional first-payment deferral or a January holiday, and the ability to overpay or settle with a defined rebate method.

Commercial Business Loan. Fixed-rate £25,001 to £300,000, 12 months to 10 years. Shows an arrangement fee of 1.5% and the option to request capital repayment holidays up to 24 months, subject to status.

Flexible Business Loan. Fixed or variable, from £25,001, with typical maximums up to £10m fixed and up to £25m variable, and terms up to 20 years. Repayment holidays up to 24 months may be available. Early repayment on fixed may incur break fees; arrangement and other fees can apply.

Eligibility notes. Product pages highlight case-by-case underwriting. The Commercial Business Loan page explicitly lists no minimum turnover. Security may be required. HSBC confirms open banking capabilities for integrations.

Regulatory status. HSBC Bank plc appears on the FCA Register (FRN 114216).

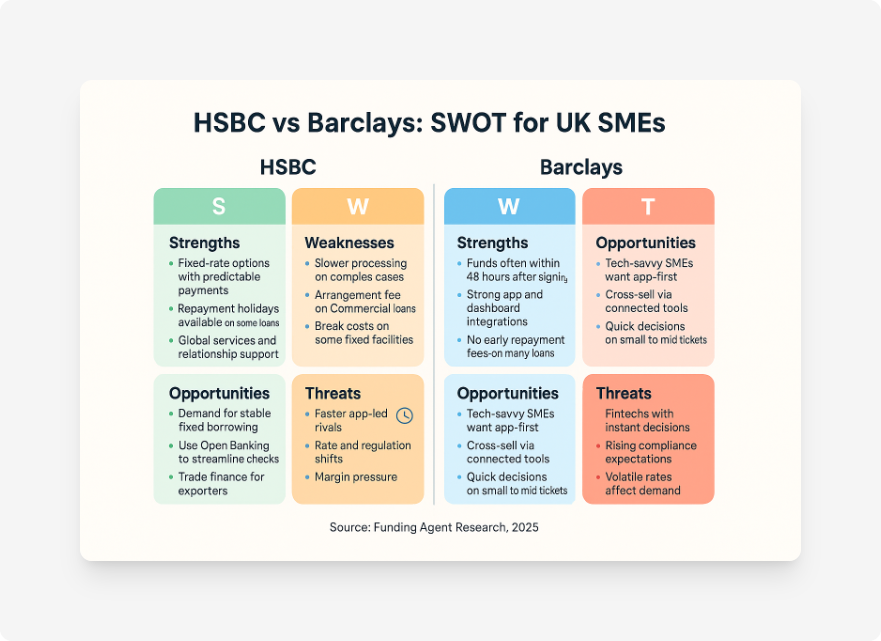

Pros of HSBC

- Clear representative APRs on the Small Business Loan page and fixed repayments for predictable cash flow.

- Capital repayment holidays available on some loans, as outlined on the Commercial Business Loan and Flexible Business Loan pages, subject to status.

- Broad ladder of products for small to large borrowing; variable or fixed on Flexible.

Cons of HSBC

- Some products include arrangement or prepayment fees and fixed-rate break costs on early settlement for fixed facilities.

- Funding timelines vary with due diligence and documentation.

Barclays overview, loan sizes, fees, repayment style, typical terms, eligibility

Unsecured business loans. Commonly cited up to £100,000 for eligible applicants, with fixed terms often between 1 and 10 years. Barclays highlights fast disbursement: funds usually within about 48 hours after paperwork is signed.

Secured and larger facilities. Barclays offers fixed or variable structures with longer terms for secured borrowing. Its digital tooling includes a SmartBusiness Dashboard integrating data sources like QuickBooks and PayPal to help with management.

Early settlement. Barclays commonly states no early repayment fees on many business loans, with interest recalculated to the date you settle.

Regulatory status. Barclays Bank PLC appears on the FCA Register (FRN 122702).

Pros of Barclays

- For many unsecured loans, funds are usually available within about 48 hours after you sign.

- No early repayment fees on many business loans, so early settlement is straightforward on fixed unsecured facilities.

- Strong mobile experience and a unified view through the SmartBusiness Dashboard.

Cons of Barclays

- Representative APRs are not always listed on the product page; rates vary by profile and product.

- Complex or secured structures can involve additional documentation and take longer.

Costs and Repayments in Practice

Fee models differ by product. HSBC’s SBL is simple: fixed interest, no arrangement fee, and clearly shown representative APRs. Commercial and Flexible loans introduce arrangement fees or prepayment charges depending on rate type and timing. Barclays commonly signals no early repayment fees on many business loans, so total interest falls if you settle early, but your quoted rate and any product-specific terms still apply.

Worked example: HSBC fixed loan

Assumptions: £25,000 over 5 years at 8.6% APR, fixed, no arrangement fee. Monthly repayment is about £514.12 and total repay about £30,847.14. This follows standard amortisation and aligns with HSBC’s fixed-rate structure shown on the Small Business Loan page.

Worked example: Barclays unsecured loan

Assumptions: £50,000 over 3 years at 7.0% fixed, no early repayment fee. Monthly repayment is about £1,543.85 and total repay about £55,578.77. If your rate rose to 8.0% on a variable deal, the monthly would be about £1,566.82, roughly £23 more per month. Barclays indicates funds are usually available within about 48 hours after you sign.

Speed and Service

HSBC. Timelines are case-by-case and depend on the product and documents. Commercial and Flexible loans can allow capital repayment holidays, which can support cash flow but increase total interest. HSBC’s business app and internet banking support day-to-day control, with open banking options for integrations.

Barclays. The bank regularly signals that funds are typically available within about 48 hours after signing the agreement for many unsecured loans. Its mobile and dashboard tooling is a strength for ongoing management.

Note on outages. All large banks experience occasional disruptions; for example, Reuters reported an HSBC UK digital outage on 27 August 2025 that was resolved the same day.

Who Each Lender Suits

Scenario 1: Established manufacturer expanding - why HSBC often fits

You want long-dated fixed repayments and the option to smooth cash flow during a ramp-up. HSBC’s Commercial Business Loan and Flexible Business Loan combine fixed options, potential capital repayment holidays, and large upper limits, which suit plant upgrades and expansion projects.

Scenario 2: Tech or services SME scaling - why Barclays often fits

You want fast funds after signing and simple early settlement. Barclays’ unsecured path is well known for speed and straightforward overpayments, and its app and dashboard, including the SmartBusiness Dashboard, can help a lean team stay on top of cash flow.

How to Apply

HSBC steps and requirements

- Choose product: Small Business Loan for £1k to £25k fixed, Commercial for £25k to £300k fixed, or Flexible for larger or variable needs.

- Apply online or with a relationship team. Commercial and Flexible may require phone or RM support.

- Prepare documents. Expect recent accounts, cash flow forecasts and a clear plan for use of funds; HSBC lists these typical items on its Growth Guarantee Scheme pages.

- Confirm fees. SBL shows no arrangement fee, while Commercial lists 1.5% and Flexible mentions case-by-case fees.

Barclays steps and requirements

- Start online for unsecured borrowing or speak to the business team for larger secured options.

- Provide financials and ID. Third-party overviews such as NerdWallet UK describe common asks, including recent accounts, forecasts and details of existing debt.

- On approval, sign the agreement. Barclays often funds within about 48 hours after signing for many unsecured loans.

Final Verdict, Which Lender Fits Your Business Best

Choose HSBC if…

- You prioritise fixed repayments with clear representative APRs.

- You want options like capital repayment holidays on larger loans.

- You need the flexibility of fixed or variable structures with upper limits into the millions.

Choose Barclays if…

- You value speed, with funds often within about 48 hours after signing on many unsecured loans.

- You want the ability to settle early without fees on many products.

- You prefer a strong app-led and dashboard experience for day-to-day control.

Bottom line. Both lenders are FCA-authorised and serve UK SMEs at scale. HSBC leans into fixed-rate clarity and structured options for larger projects. Barclays stands out for quick post-signature funding and polished digital servicing. If you would like an independent shortlist and rates from a panel of lenders, speak to Funding Agent or send your details via our enquiry form.

Sources

- HSBC Small Business Loan

- HSBC Commercial Business Loan

- HSBC Flexible Business Loan

- HSBC Business Internet Banking

- HSBC Open Banking

- FCA Register - HSBC Bank plc (FRN 114216)

- FCA Register - Barclays Bank PLC (FRN 122702)

- Barclays business loans

- Barclays SmartBusiness Dashboard

- Barclays business loans - NerdWallet UK overview

- Barclays business loans - Forbes Advisor UK review

- Reuters - HSBC UK restores banking services after outage (27 Aug 2025)

FAQs

HSBC offers interest rates between 4% and 9.5%.

Funds are available 1 to 3 business days post-decision.

Barclays offers app-based loan management and document uploads.

No, Barclays does not charge for early repayment.

HSBC targets SMEs and large enterprises.

Yes, Barclays restricts loans for the gambling sector.