NatWest vs Barclays: Which Bank Is Right for Your UK Business?

.png)

This guide compares NatWest business loans and Barclays business loans for UK SMEs. We look at products and terms, costs and repayments, speed and service, and who each lender suits. Where possible, we verify facts against each bank’s own pages. If you are exploring a business loan for growth or refinancing, this will help you choose a route that fits your plans today. NatWest offers both small business loans and larger fixed or variable facilities, while Barclays provides unsecured loans and a growing range of green finance.

NatWest vs Barclays, Visual Comparison Dashboard

These charts translate the research into clear visuals. Compare rate ranges and typical pricing, headline loan sizes and terms, indicative speed from application to funding, fees, digital capability, and customer sentiment. Values reflect the supplied research and are illustrative where noted.

Products and Terms at a Glance

NatWest overview, loan sizes, fees, repayment style, typical terms, eligibility

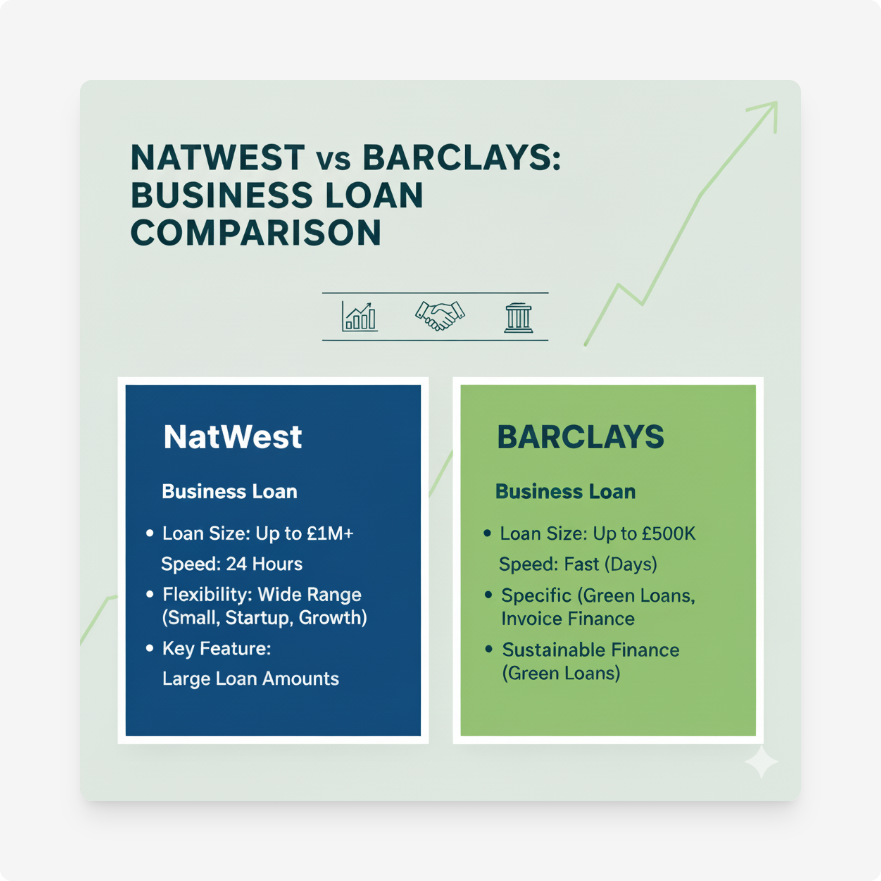

NatWest’s Small Business Loan offers fixed-rate borrowing from £1,000 to £100,000, with terms from 1 to 7 years, and it highlights no early repayment or closure fees for this product. For larger needs, NatWest’s Fixed and Variable Rate Business Loans cover £25,001 to £10m on a fixed rate and no upper limit on a variable rate, with repayment terms up to 25 years and no early repayment fees according to the product FAQs.

Application is online, with NatWest stating that approved borrowers may receive funds within 24 hours, and even same-day payout if certain cut-off times are met on weekdays. The small business loan page lists information you will need such as turnover, profit, and details of existing lending.

Pros of NatWest

- Choice of small business fixed-rate loans or larger fixed or variable facilities with terms up to 25 years.

- No early repayment fees indicated on both small business loans and fixed or variable loans; flexible repayment options noted in the detailed pages.

- Clear online journey with fast indicative timelines once approved.

Cons of NatWest

- Rates and margins vary by risk; security or guarantees may be required for larger facilities.

- For complex cases, extra documentation or underwriting steps can extend timelines.

Barclays overview, loan sizes, fees, repayment style, typical terms, eligibility

Barclays’ business borrowing hub shows fixed or variable business loans with flexible terms and states there are no early repayment fees on many business loans. Barclays’ pages also note unsecured lending from £1,000 up to £100,000, with money usually available within about 48 hours after you sign the paperwork. Shorter unsecured loans can run from 1 to 10 years, while larger or secured structures can extend longer.

Barclays also markets Green Loans for Business, a secured solution with discounted interest rates for eligible green assets. This can suit retrofit, energy, and sustainability upgrades where there is a clear environmental benefit.

Pros of Barclays

- Clear stance on no early repayment fees for many business loans; simple early settlement.

- Green finance options with discounted rates for eligible assets.

- Fast post-signature funding in typical cases, often within about 48 hours.

Cons of Barclays

- Larger secured loans or property finance may involve different fee rules and prepayment considerations.

- Eligibility for green loans requires proof of an eligible asset and may require additional checks.

Costs and Repayments in Practice

The examples below are for illustration. Your actual rate and fees depend on credit, security, sector, and term. Always check the lender’s calculator or speak to a broker before you proceed.

Worked example, NatWest

Assume a £100,000 fixed-rate small business loan over 5 years at 8.2% representative APR. Monthly repayment would be about £2,037; total repay about £122,233. This uses standard amortisation and assumes no arrangement fee and no early repayment fees. If you repay early, you reduce total interest due to fewer months outstanding.

Worked example, Barclays

Assume a £300,000 business loan over 7 years at a typical 6.5% rate. Monthly repayment would be about £4,455; total repay about £374,206. Barclays states no early repayment fees on many business loans. If you settle early, your total interest falls; always confirm the exact product terms before signing.

Speed and Service

NatWest highlights an online journey, with an instant decision for some products and potential funding within 24 hours after approval if you meet the weekday cut-off. Barclays indicates that once approved and paperwork is signed, funds are usually available within about 48 hours. In both cases, complex deals or additional checks can extend timelines.

Who Each Lender Suits

Scenario 1, why NatWest often fits

You want a simple fixed-rate small business loan, or you need a larger facility up to £10m with repayment terms up to 25 years, and you prefer the clarity of no early repayment fees across the listed products. This can suit a retail or services firm planning a refurbishment, a fit-out, or a larger asset purchase where predictable monthly costs are helpful.

Scenario 2, why Barclays often fits

You want straightforward unsecured borrowing with quick access to funds after signing, or you are investing in eligible sustainability upgrades and want access to discounted green finance. This can suit technology, light manufacturing, or office-based firms pursuing energy savings and brand-aligned ESG improvements.

How to Apply

NatWest steps and requirements

- Start online and get a quote. NatWest explains the small business loan flow, including a 10 minute application time for many cases.

- Have details to hand, for example start date, last 12 months’ turnover, projected turnover, net profit, and existing lending.

- If approved and documents are signed by the weekday cut-off, funds can reach you the same day or within 24 hours.

Barclays steps and requirements

- Explore business borrowing options online, then apply for the loan product that fits your use case.

- On approval, sign the paperwork. Barclays notes funds usually arrive within about 48 hours after signatures are completed.

- For sustainability projects, consider green loans for eligible assets and prepare evidence of the asset or works planned.

Final Verdict, Which Lender Fits Your Business Best

Choose NatWest if…

- You want a fixed-rate small business loan with simple early settlement.

- You may need a larger facility up to £10m, with terms up to 25 years on fixed or variable structures.

- You prefer a clear online journey with fast potential payout after approval.

Choose Barclays if…

- You want no-nonsense unsecured borrowing with money often available within about 48 hours after signing.

- You are investing in energy-saving or sustainability projects and want discounted green finance for eligible assets.

- You want flexibility to repay early without fees on many products.

Both banks can work well. If you need structured large-ticket options and long terms, NatWest’s fixed and variable range is broad. If you want a simple experience, quick funding after signatures, or a sustainability-linked product, Barclays has an edge. To compare offers across a wider panel and get support with documents and eligibility checks, speak to Funding Agent or start with our enquiry form.

Sources

- NatWest Small Business Loan

- NatWest Fixed & Variable Rate Business Loans

- NatWest Growth Guarantee Scheme

- Barclays Business Borrowing

- Barclays Business Funding Options

- Barclays Business Loans and Calculator

- Barclays Green Loans for Business

Notes: Rates, fees, and eligibility change over time. Product names and terms differ by loan type. Use the lender pages above for the latest details and consider broker support if you want to compare multiple offers side by side.

FAQs

NatWest focuses on UK SMEs with varied financial needs.

Yes, Barclays offers green loans focusing on sustainability.

NatWest processes applications in 1 to 5 days.

No early repayment charges for Barclays green loans.

Barclays has superior digital and mobile integration.

Barclays has higher customer satisfaction due to efficient service and digital tools.