Secured vs Unsecured Loans in the UK, Which Is Best for Your Situation?

Choosing between a secured and unsecured business loan affects price, speed, risk and how much you can borrow. A secured facility uses an asset as collateral, which reduces lender risk and can unlock larger amounts and longer terms. An unsecured facility relies on your creditworthiness and affordability with no specific asset pledged, which usually means smaller limits and a higher price. For clear plain-English definitions, see MoneyHelper, and for the rules on creditworthiness and affordability checks, see FCA CONC 5.2A.

At a glance

- Secured business loans: Asset pledged as security, for example property, vehicles, plant, or a debenture over business assets. Often larger amounts, longer terms, and lower rates. Asset is at risk if you do not keep up repayments. See MoneyHelper on second charges and UK Finance on asset-based lending.

- Unsecured business loans: No specific asset pledged. Decisions lean on credit files, income and commitments, and sustainability of repayments, which lenders must assess under FCA CONC 5.2A.

How each loan type works in the UK

Secured business lending

Security can be a fixed charge over a specific asset such as property or equipment, or a floating charge across wider business assets through a debenture. Many facilities, including asset finance and asset-based lending, rely on the value in plant, machinery, vehicles, receivables or stock. Because the lender has recourse to an asset, pricing can be sharper and limits can be higher.

Unsecured business lending

Unsecured loans rely on your credit profile and affordability. Lenders assess your company’s financials and director credit files, and they often use personal guarantees as an extra layer of comfort even though no specific asset is pledged. Eligibility varies by lender. Lenders must test whether repayments are sustainable under FCA creditworthiness rules.

Secured vs unsecured business loans, side-by-side

When each route makes sense

Use a secured loan when

- You need a larger amount and a longer term and you have valuable assets or equity to support it.

- You prefer a lower price and can accept security over assets such as vehicles, plant, receivables or property. See UK Finance on asset-based finance.

- You are financing specific kit and want the facility matched to that asset. See Finance & Leasing Association for market context on equipment and vehicle funding.

Use an unsecured loan when

- You want speed and simplicity with no security documented against an asset.

- Your requirement is modest to medium sized, and your credit profile is strong enough for approval.

- You are early stage and want to avoid charges over assets. Government backed Start Up Loans are unsecured personal loans for business use with mentoring support.

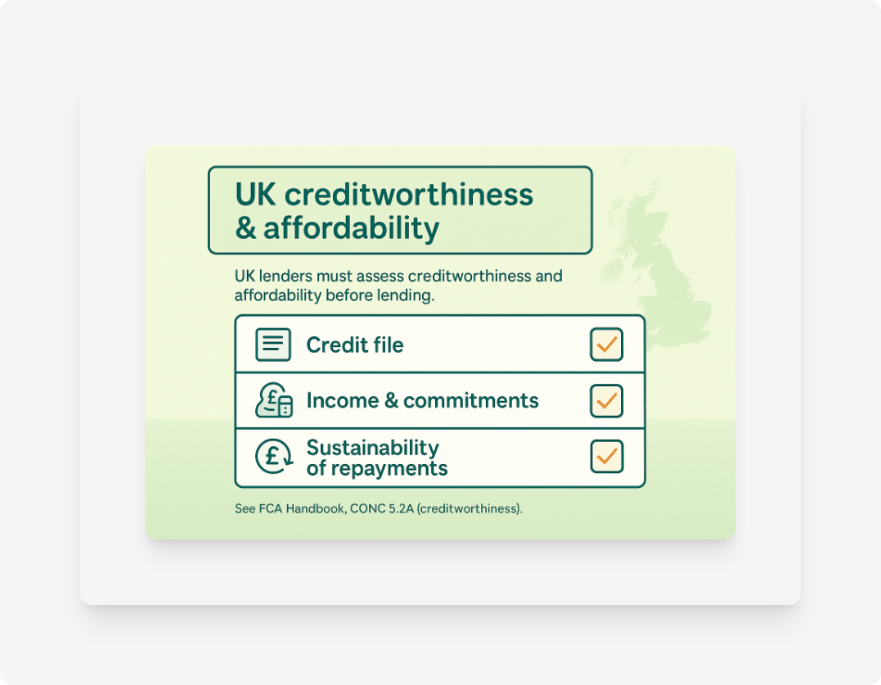

What UK lenders check before making an offer

Regulated firms must assess creditworthiness and affordability. Expect checks on credit files, income and commitments, and whether repayments are sustainable. See FCA CONC 5.2A. Common items include:

- Company accounts, bank statements and management information

- Trading history and cash flow forecasts

- Director credit files and identification checks

- Security valuation and legal due diligence for secured proposals

Pricing, fees and what to compare

Look beyond headline APR. Compare the total cost of credit after fees, any broker charges, and early settlement terms. For secured deals, add valuation, legal and charge registration fees. For invoice finance and asset-based lending, compare service fees, discount margins and audit charges. Guidance on unsecured and secured borrowing is set out by MoneyHelper.

Risks and protections

- Asset at risk on secured borrowing. Missed payments can lead to enforcement on the charged asset.

- No pledged asset with unsecured borrowing, but arrears can escalate to court action and a charging order that secures the debt on property.

- Right to repay early is protected for regulated consumer credit under the Consumer Credit Act and Early Settlement Regulations. Business lending can also include early settlement rights in the contract. Check your agreement.

Which sectors tend to use which products

Asset-heavy sectors such as manufacturing, construction, agriculture, transport and logistics often use asset finance and asset-based lending to fund vehicles and equipment, or to unlock cash tied up in receivables and stock. Service businesses, agencies, hospitality, retail and early stage firms often lean on unsecured term loans, overdrafts and Start Up Loans. See Start Up Loans and MoneyHelper on personal loans for general context on unsecured borrowing.

How Funding Agent can help

Tell us how much you want to borrow and how quickly you need the funds. We compare secured and unsecured options across trusted UK lenders with one simple enquiry. If you prefer asset-backed borrowing, start with our guide to asset finance. If you want a fast unsecured route, use our quick enquiry form and we will match you to suitable lenders.