Skipton vs Bibby: Compare Rates & Services

.png)

.png)

This comparison is for UK owners and finance managers weighing two established invoice finance providers. We look at products, fees, service and who each lender suits in 2025. First mentions: Skipton Business Finance and Bibby Financial Services. If cash is tight because customers pay on terms, the right partner can stabilise working capital fast.

Skipton vs Bibby: the invoice finance head to head

This dashboard compares pricing, limits, terms, speed, fees, setup costs, digital features and ratings for two UK invoice finance lenders. Read each chart as a pairwise view. Grouped bars show minima and maxima. Dots mark typical points where shown. Use the tabs to focus on one factor at a time. It helps a UK SME choose a facility that fits cash flow, sector risk and service needs today.

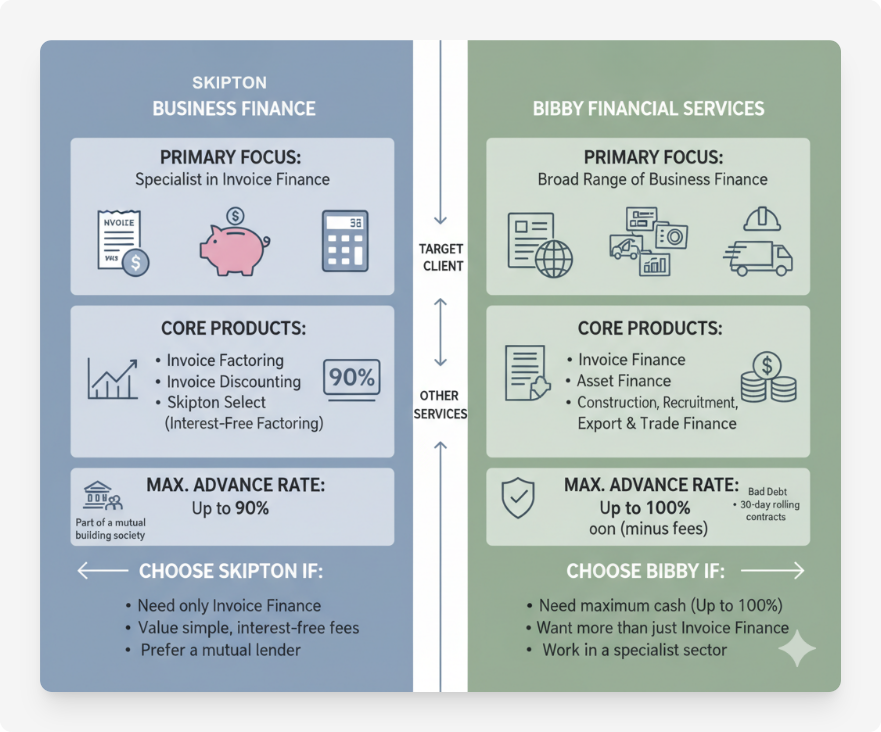

Products and Terms at a Glance

Both lenders provide invoice finance to convert sales on terms into same-day cash. Headline features vary by facility, sector and risk.

Notes: published advances and features depend on sector, debtor quality and facility type. Always check your specific offer.

Skipton Business Finance overview, loan sizes, fees, repayment style, terms, eligibility

Skipton specialises in invoice finance for UK SMEs. Its factoring page states advances of up to 90% with cash the day you raise the invoice, and its discounting page mirrors the 90% headline. See the official factoring and discounting pages.

A stand-out feature is Skipton Select. This is an interest-free factoring option. You pay a setup fee and a turnover-based service charge, with no discount-rate interest on drawings. That simplifies cost forecasting.

Eligibility focuses on trading B2B and issuing invoices on credit terms. Skipton’s FAQs emphasise that a long credit history is not essential compared with traditional bank lending. See Invoice Finance FAQs.

Market round-ups place common SME facility sizes in the £25,000 to £5,000,000 range and note typical advances of up to 90%. See recent comparisons from Capitalise and Startups.

Pros of Skipton

- Interest-free plan available, which removes interest cost from the equation for many users.

- Clear fees and personal service with a named relationship manager.

- Fast access to cash on the day you raise invoices for factoring.

- Confidential options if you want to manage collections in-house.

Cons of Skipton

- Product set is focused on invoice finance rather than a full corporate toolkit.

- The interest-free plan still carries a service charge and a setup fee.

- Advance rates and eligibility vary by sector and debtor quality, as with all providers.

Bibby Financial Services overview, loan sizes, fees, repayment style, terms, eligibility

Bibby is one of the UK’s largest independent SME funders. Its invoice finance pages highlight access to cash within 24 hours of setting up a facility and a choice of factoring or confidential discounting. See Invoice Finance products and the invoice discounting page.

Bibby literature and brochures reference advances up to around 90% of approved receivables. Its overview for recruiters gives a 90% example and 24-hour access after setup. Bibby also offers add-ons such as Bad Debt Protection that can cover up to 90% of losses, plus top-up cashflow loans alongside invoice finance.

Eligibility depends on trading B2B with credit terms and having basic financial information to hand. Bibby’s guidance sets out typical criteria such as 30 to 90 day terms and viable trading history. See eligibility points and this article.

Pros of Bibby

- Broad product range and sector coverage. Construction, export and FX services are available in the group.

- Bad debt protection and extra headroom options, such as cashflow top-ups linked to your facility.

- Scale and resources across the UK with a relationship-led approach.

Cons of Bibby

- Standard pricing includes interest on drawn funds plus a service fee, which can be higher for slow-paying ledgers.

- More options can add complexity when choosing the right product variant.

Costs and Repayments in Practice

Most invoice finance uses two charges. A service fee, often a small percentage of monthly turnover. And discount-rate interest on the cash you draw, charged until the customer pays. Independent guides quote typical discount fees of about 1.5% to 3% and service fees from about 0.25% to 3%, with wide variation by risk and scale. See this Expert Market explainer.

Skipton’s Skipton Select changes the structure. It removes interest on drawings and replaces it with a clear service charge and a setup fee. That suits firms whose customers pay reasonably quickly. Bibby follows the classic model, but adds options such as Bad Debt Protection and a Cashflow Advance that sits alongside the facility.

Worked example: Skipton Business Finance

Assumptions: £50,000 invoice. 90% advance. Customer pays in 45 days. Using Skipton Select at a flat 1.0% service charge. Ignoring the one-off setup fee for simplicity. Real pricing varies by risk and volume.

- Day 1 advance: 90% of £50,000 = £45,000.

- Service charge: 1.0% of £50,000 = £500.

- On payment, the remaining 10% (£5,000) is released less the £500 fee = £4,500.

- Total cash received: £45,000 + £4,500 = £49,500.

- Total cost: £500, equal to 1.0% of the invoice.

Why it can be attractive: no interest accrues while you wait for payment. Simplicity helps forecasting.

Worked example: Bibby Financial Services

Assumptions: £50,000 invoice. 90% advance. Customer pays in 45 days. Service fee 0.75% of invoice. Discount-rate interest 7.0% per year on funds drawn. Real pricing depends on sector, ledger quality and volume.

- Day 1 advance: 90% of £50,000 = £45,000.

- Service fee: 0.75% of £50,000 = £375.

- Interest on drawings: £45,000 × 7.0% × 45/365 = £388.36.

- Total fees: £375 + £388.36 = £763.36 (about 1.53% of the invoice).

- On payment, the remaining 10% (£5,000) is released less £763.36 = £4,236.64.

- Total cash received: £45,000 + £4,236.64 = £49,236.64.

Why it can be attractive: you can add bad debt protection and request temporary headroom. The trade-off is interest on drawings.

Comparing costs with alternatives such as working capital loans or term loans is useful. Invoice finance scales with sales and does not create a fixed monthly repayment. Loans give certainty of repayment amounts but draw interest on the full balance from day one.

Speed and Service

After onboarding, both lenders highlight rapid access to cash. Bibby says you can access cash within 24 hours of setting up a facility. See product page and the invoice finance landing page. Skipton’s factoring page states you can get up to 90% on the day you raise the invoice. See Skipton.

Service style differs. Skipton leans into named relationship managers and quick decision-making. Bibby combines relationship managers with national scale and a 24/7 client portal, plus optional add-ons like Bad Debt Protection and corporate funding top-ups.

Who Each Lender Suits

Typical scenario for Skipton Business Finance

You are a growing B2B SME that invoices on 30 to 60 day terms. You want simple pricing and predictable costs. You like the idea of an interest-free factoring plan. You prefer a relationship-led approach and value continuity with a named manager. You want to keep options open for confidential discounting later.

Typical scenario for Bibby Financial Services

You need flexibility across sectors or complex debtors. You may want to add bad debt protection, construction-friendly structures, or an extra cashflow loan tied to your facility. You value a large provider with national reach and sector expertise, from manufacturing and transport to recruitment.

How to Apply

Application steps and documentation required for each lender

Skipton Business Finance. Start with an enquiry and a discussion of funding needs. Expect a review of your sales ledger, main debtors, and standard terms. Typical documents include recent management accounts, aged debtor and creditor reports, key customer contracts or purchase orders, and three to six months of business bank statements. Skipton’s FAQs explain that extensive credit history is not essential compared to bank loans.

Bibby Financial Services. Begin with an enquiry and eligibility check. Bibby looks for B2B invoicing on 30 to 90 day terms, viable trading and basic controls. The invoice discounting page lists common criteria. You will provide management accounts, aged debtor and creditor schedules, bank statements and details of your largest customers. Bibby outlines what providers look for in this guide.

Tip: before you apply, reconcile your ledger and chase overdue items. Cleaner ledgers tend to secure better advance rates and fees.

Final Verdict: Which Lender Fits Your Business Best

Choose Skipton Business Finance if…

- You want an interest-free factoring option with a clear service charge.

- Your customers pay reliably within agreed terms, so simplicity beats flexibility.

- You prefer close, relationship-led service with fast decisions.

- You want the option of confidential discounting as you grow.

Choose Bibby Financial Services if…

- You need a wider toolkit such as bad debt protection or sector-specific structures.

- You value national scale and a long-standing provider.

- Your ledger has seasonal swings and you may need extra headroom via top-up loans.

- You operate in sectors like construction where specialist support helps.

Both lenders can unlock working capital quickly. The best choice is the one that matches your ledger profile and service expectations. If you want independent help shortlisting and negotiating the right facility, speak to Funding Agent or use our enquiry form.

Sources

- Skipton Business Finance – Invoice Factoring

- Skipton Business Finance – Invoice Discounting

- Skipton Select – clear-fee, interest-free overview

- Skipton – Invoice Finance FAQs

- Bibby Financial Services – Invoice Finance products

- Bibby – Invoice Finance landing page

- Bibby – Invoice Discounting

- Bibby – Bad Debt Protection

- Bibby – Overview of our finance solutions (PDF)

- Bibby – Cashflow Advance factsheet (PDF)

- Bibby – Construction Funding Fast

- Expert Market – typical invoice finance fees

- Capitalise – 2025 invoice finance round-up

- Startups – invoice factoring providers overview

FAQs

Bibby Financial Services is known for tailored invoice financing with competitive rates, while Skipton Business Finance typically offers flexibility in loan terms. Comparing precise rates would depend on specific business needs.

Yes, you can apply to Bibby Financial Services even if Skipton has rejected your application. Bibby offers a variety of financial solutions that may cater to different eligibility criteria than Skipton.

Skipton Business Finance often includes fees like arrangement or administrative costs, while Bibby might charge based on the percentage of invoice value. It's important to review fee structures directly with each lender.

Skipton typically processes applications swiftly due to streamlined procedures, often within a few days. Bibby also offers quick processing, but exact timing may vary depending on the complexity of the financial requirement.

Both Skipton and Bibby offer dedicated customer support with varied channels. Skipton often receives praise for personalised service, while Bibby is known for industry-specific expertise and support.

Skipton provides flexible funding options suitable for seasonal businesses, while Bibby's expertise in invoice finance supports cash flow management across various industries. Understanding these features can guide better decision-making.