The Hidden Costs in UK Business Loans

.png)

What Most Lenders Do Not Highlight — And How to Calculate the True Cost Before You Sign

When you compare business loans, most lenders put one number front and centre: the interest rate. It is clean, simple, and easy to advertise.

But for many UK businesses, the headline rate is only part of the story. Arrangement fees, early repayment penalties, compulsory insurance, and a handful of other charges can quietly add thousands of pounds to the total cost of borrowing — costs that are rarely mentioned in the opening quote.

This guide breaks down every significant hidden fee you may encounter in UK business loans in 2026, explains how each one works in practice, and shows you how to calculate your true cost before you commit to anything.

What Counts as a 'Hidden Fee' in a Business Loan?

A hidden fee is not necessarily one that a lender is concealing. More often, it is a charge that sits in the small print rather than the headline offer — easy to overlook when you are focused on monthly repayments or the APR being advertised.

A lender might promote: 'From 6.9% APR'. But that figure may not fully capture:

- Arrangement or origination fees charged at drawdown

- Broker commissions added to your loan balance

- Early repayment charges if your plans change

- Legal and valuation fees on secured lending

- Compulsory insurance products bundled with the loan

- Annual facility or non-utilisation fees on revolving credit

Understanding these charges in advance is not about distrust. It is about making an accurate comparison between lenders so you choose the loan that costs least for your specific situation.

The Complete List of Hidden Fees in UK Business Loans

Here is a full reference table covering the most common fees, their typical ranges, and how to spot them:

1. Arrangement or Origination Fees

This is the most common additional charge in UK business lending. The lender charges a one-off fee — typically between 1% and 3% of the loan — to cover the cost of processing and setting up the facility.

On a £100,000 loan with a 2% arrangement fee, that is £2,000 added before you receive a penny. The critical detail: some lenders deduct this from the funds advanced, meaning you receive £98,000 but repay £100,000 plus interest. Others add it to the loan balance — so you also pay interest on the fee itself throughout the term.

Always ask: is the fee deducted or capitalised? The answer changes your effective cost significantly.

2. Broker Fees

If you source your loan through a broker or comparison service, there may be a separate fee on top of any lender charges. Broker fees can take several forms: a fixed advisory fee, a percentage commission, or both.

Some brokers are paid entirely by the lender and charge you nothing directly. Others pass a cost to the borrower, sometimes by adding it to the loan balance. The FCA requires brokers to be transparent about remuneration — but not all are as clear as they should be.

3. Early Repayment Charges

This is the fee that surprises borrowers most often. Many assume that paying a loan off early saves money — and it usually does in terms of interest. But a growing number of UK lenders include early repayment charges (ERCs) that offset or eliminate those savings.

ERCs typically take one of two forms: a percentage of the remaining balance at the point of repayment, or a set number of months' interest (often two to six months). In some fixed-fee lending products — common with merchant cash advances and certain fintech lenders — you may be required to pay the full interest regardless of when you settle.

If there is any chance your business plans will change — an acquisition, a refinance, a windfall — the ERC clause should be one of the first things you check.

4. Late Payment and Default Fees

Missing a repayment date triggers a late payment fee in most loan agreements. These are typically fixed amounts ranging from £25 to £150 per missed payment, though some lenders also apply a rate increase on outstanding balances.

The compounding effect matters. Two or three missed payments in a difficult trading period can create a material additional cost — and sustained default may trigger collection costs and impact your business credit file, making future borrowing more expensive.

5. Facility and Non-Utilisation Fees

Most common with revolving credit facilities, overdrafts, and invoice finance arrangements, these fees are charged whether or not you draw on the facility. An annual facility fee might be 0.5%–2% of the agreed limit. A non-utilisation fee (sometimes called a commitment fee) is charged on the portion of the facility you have not drawn.

For a business that maintains a £200,000 revolving credit facility but typically uses only £50,000, a 1% non-utilisation fee on the undrawn £150,000 amounts to £1,500 per year — with no corresponding benefit.

6. Legal and Valuation Costs

Secured business loans — those backed by property, equipment, or other assets — often require a formal valuation and legal documentation of the security charge. These costs are separate from the loan itself and are usually payable by the borrower.

Depending on the asset being secured and the complexity of the documentation, costs can range from a few hundred pounds to several thousand. Crucially, they are typically payable upfront, even if the loan ultimately does not proceed — so clarify what happens to these fees if the deal falls through.

7. Compulsory Insurance Products

Some lenders require borrowers to take out a specific insurance product — often a business interruption or payment protection policy — as a condition of the loan. The premium is usually added to the loan balance, which means you pay interest on the insurance as well as the premium itself.

This practice has attracted regulatory attention in consumer lending. In business lending it remains relatively common. If a lender requires insurance, ask whether you can source equivalent cover independently at a lower cost, and whether refusal would affect the loan terms.

8. Personal Guarantee Costs

Not a fee in the conventional sense, but a personal guarantee is a significant financial commitment that deserves mention. Many unsecured business loans — particularly for smaller or newer businesses — require a director to personally guarantee the debt.

This means your personal assets are at risk if the business defaults. Some lenders require indemnity insurance to protect against this exposure, which adds another layer of cost. The guarantee itself may also appear on personal credit records and affect your ability to borrow elsewhere.

Does APR Tell You the Full Story?

In theory, the Annual Percentage Rate (APR) is meant to reflect the total annual cost of borrowing, including interest and standard fees. In practice, the picture is more complicated.

First, a representative APR means that only 51% of successful applicants need to receive that rate. The rate you are actually offered may be meaningfully higher, depending on your credit profile, sector, and the size of the loan.

Second, some fees may be excluded from the APR calculation depending on how the loan is structured — particularly conditional fees, charges payable only on default, and costs that fall outside the standard loan term.

Third, APR does not account for early repayment. If you settle the loan after 18 months of a 5-year term, the effective cost of an arrangement fee becomes dramatically higher on an annualised basis than the APR implied.

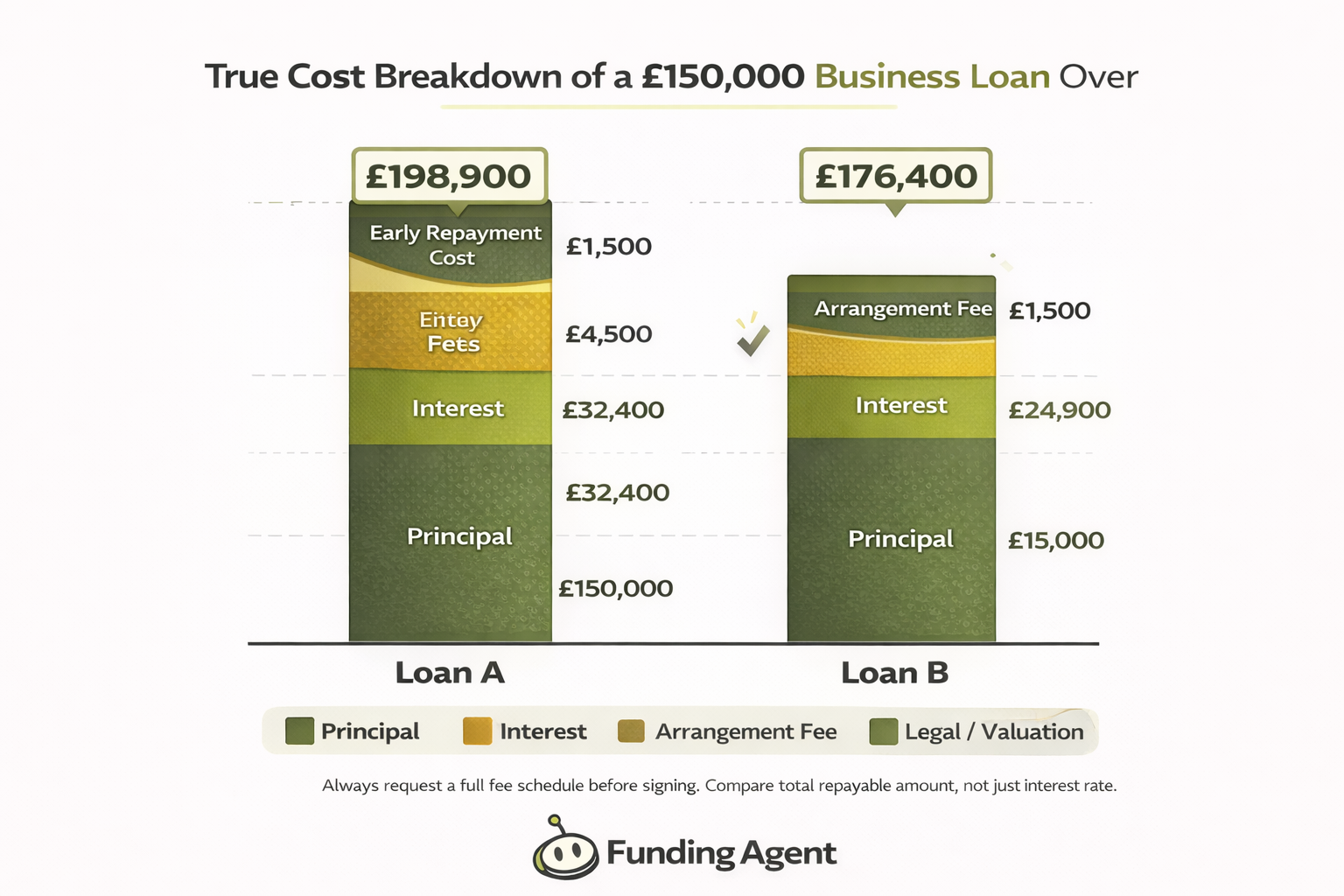

A Real Example: How Hidden Fees Change the True Cost

To illustrate why total cost matters more than interest rate, consider two loans on £100,000 over 3 years:

Loan A appears to be the cheaper option based on interest rate alone. But once you add the £3,000 arrangement fee and factor in the loss of flexibility from the early repayment clause, Loan B is materially better for most businesses — particularly those that may refinance or have surplus cash to repay early.

The lesson is consistent: a lower rate does not mean a lower total cost.

How to Calculate the True Cost of a Business Loan

Before accepting any loan offer, request the following from the lender:

- Total amount repayable (the single most important number)

- Full breakdown of all fees — origination, legal, insurance, broker

- Monthly repayment amount

- Early settlement terms and any applicable charges

- What happens to fees paid if the loan does not complete

Armed with these figures, you can compare loans accurately by total repayable rather than by interest rate. A business loan calculator can help you model different scenarios — including the cost of early settlement at different points in the term.

If a lender is reluctant to provide a full fee breakdown before you submit a full application, treat that as a warning sign.

Red Flags That Suggest Hidden Costs

Not all additional costs are inevitable or unreasonable. But certain patterns in loan documentation or lender behaviour should prompt closer scrutiny:

- Arrangement fees above 3% without clear justification

- Vague references to 'administration costs' without specified amounts

- Early repayment charges that exceed 6 months' interest

- Compulsory insurance that cannot be sourced independently

- A representative APR that differs substantially from your quoted rate

- Complex fee structures that are difficult to explain in plain terms

- Pressure to sign before receiving a complete fee schedule

A reputable lender will be willing to itemise every cost clearly and give you time to review it. Transparency about fees is one of the clearest signals of a lender worth working with.

How to Reduce or Avoid Hidden Fees

Several practical steps can reduce the total cost of borrowing:

Negotiate the arrangement fee

Arrangement fees are often negotiable, particularly for stronger businesses or larger loan amounts. Many borrowers assume fees are fixed and do not ask. A well-presented application from a business with a solid credit profile can frequently secure a reduction.

Improve your credit profile before applying

Your business credit score affects not just the interest rate you are offered, but the fee structure too. Lenders reserve their most competitive terms — including lower or waived origination fees — for lower-risk borrowers. Checking and improving your score before applying is time well spent.

Compare total repayable, not just rate

Use a business loan calculator that incorporates fees. Input the total amount repayable — not just interest — when comparing products side by side. A fee-free loan at 8.5% may cost less over your term than a 7% loan with a 3% arrangement fee.

Ask about fee-free lenders

A growing number of alternative lenders — particularly challenger banks and fintech platforms — offer genuinely fee-free business loans, covering their margin entirely through the interest rate. These products are not always visible in headline comparison tables, so it is worth asking directly.

Borrow only what you need

Arrangement fees are typically percentage-based, so borrowing more than you need directly increases the fee. A disciplined approach to loan sizing can reduce both the fee and the total interest payable.

The Hidden Costs That Are Not Listed in Any Fee Schedule

Even a complete fee breakdown does not capture every cost of borrowing. Some of the most significant impacts on your business are harder to quantify but equally important to consider:

Cash flow strain from high monthly repayments

A loan with a competitive interest rate may still impose monthly repayments that constrain your operating budget — particularly in the early months after drawdown. Model your cash flow under realistic trading conditions, not optimistic projections.

Risk to secured assets

For secured loans, the true cost of default is the loss of the asset securing the loan — which may include business premises or key equipment. The headline loan cost does not capture this contingent exposure.

Impact on future borrowing capacity

Taking on debt reduces your capacity to borrow for other purposes. Lenders assessing future applications will see your existing commitments and may apply tighter criteria or higher rates as a result. The indirect cost of reduced financial flexibility is real, even if it does not appear on a fee schedule.

Director guarantee liability

Where a personal guarantee is required, your personal financial position is exposed to the business's performance. This is not a fee, but it is a cost — one that can have serious long-term consequences if the business encounters difficulties.

Your Pre-Signing Checklist

Before you sign any business loan agreement, work through these questions:

- What is the total amount repayable, including all fees?

- Is there an arrangement fee, and is it deducted or capitalised?

- Is a broker involved? How are they compensated, and does any cost fall to me?

- What are the early repayment terms? Is there a penalty?

- Are there any compulsory insurance or ancillary products?

- What fees apply to missed or late payments?

- For secured loans: what are the valuation and legal costs, and who pays if the deal does not complete?

- Is there a personal guarantee? What are the precise terms?

- Does the APR quoted include every fee in this list?

If any of these questions cannot be answered clearly in writing before you sign, request that they are addressed. A good lender will have no hesitation in providing this information.

Final Thoughts

Business loans remain one of the most useful tools available for funding growth, managing cash flow, or investing in new capacity. The fees associated with them are not inherently problematic — most are reasonable compensation for the work involved in underwriting and managing a facility.

The issue arises when those fees are unclear, excessive, or structured in a way that makes meaningful comparison difficult. The businesses that pay too much for their borrowing are usually the ones that focused on the headline rate and signed before getting the full picture.

The single most important habit to develop when comparing business loans is this: always ask for the total amount repayable, including all fees, before you decide. That number — not the APR, not the monthly repayment — is the only accurate basis for comparison.

With that figure in hand, you are in a much stronger negotiating position and far less likely to encounter a surprise once funds have landed.