What is a Revolving Credit Loan?

.png)

A revolving credit loan is a pre-approved line of credit that allows businesses to withdraw money up to a certain limit whenever needed. You only pay interest on what you borrow, not the entire facility.

For example, if your business secures a £100,000 revolving credit facility but only draws £25,000, you’ll only pay interest on the £25,000. Once repaid, the full £100,000 limit becomes available again. This flexibility makes revolving credit especially valuable for SMEs facing unpredictable cash flow, seasonal demand, or unexpected expenses.

Why Revolving Credit Matters Now

Cash flow remains one of the toughest challenges for UK SMEs. According to the British Business Bank’s Small Business Finance Markets Report 2025, over 60% of SMEs report cash-flow constraints linked to late payments and rising operational costs. Traditional term loans often don’t suit businesses whose income fluctuates, particularly in the service sector. This is where revolving credit loans, sometimes called revolving credit facilities, play a critical role.

A revolving credit loan gives businesses flexible access to funds up to an agreed limit. Unlike a fixed loan, you can draw, repay, and redraw funds repeatedly. Think of it as a flexible financial “safety net” that grows and shrinks alongside your cash-flow needs.

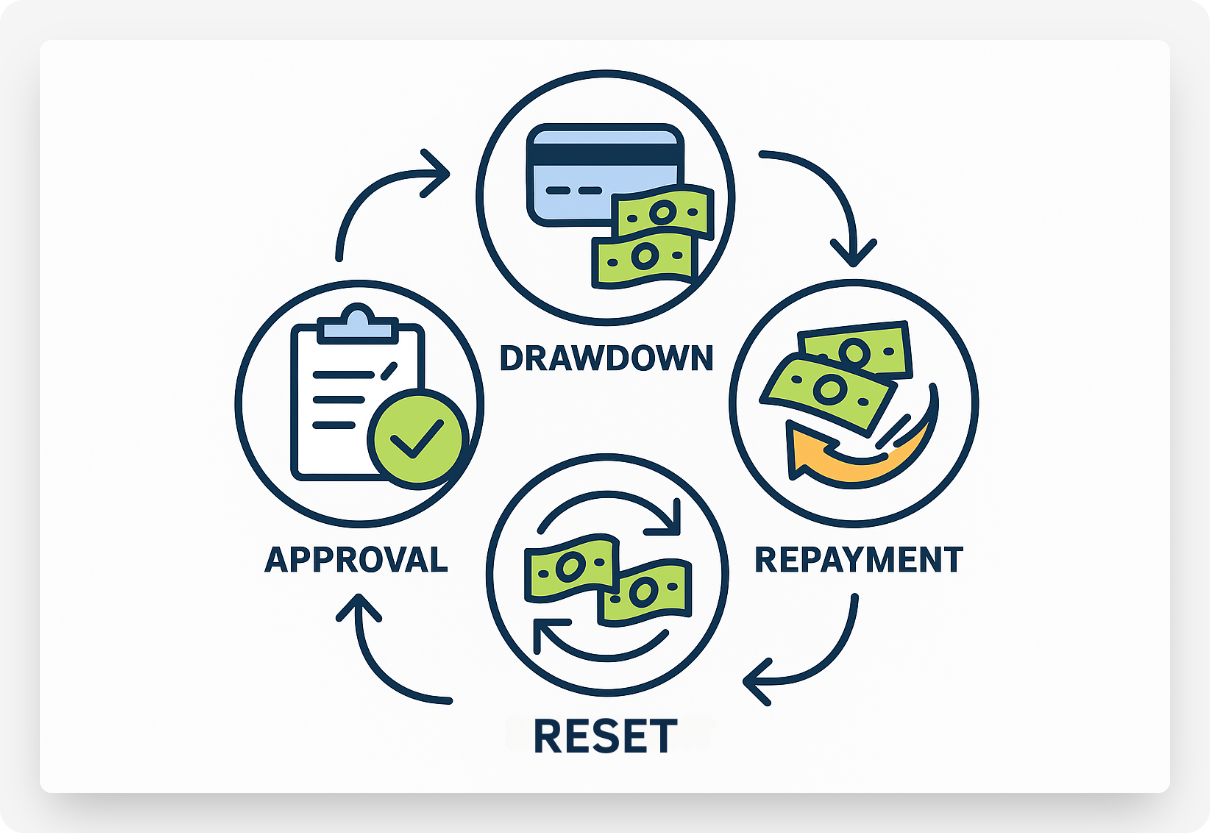

How Does a Revolving Credit Loan Work?

When approved for a revolving credit facility, your business is given a credit limit, such as £50,000. You can draw funds whenever needed and repay at your own pace. Interest is charged only on the portion you borrow. Once repayments are made, the full limit becomes available again, without needing to reapply. Many facilities also include an arrangement fee or an annual renewal cost. In practice, it works like a business credit card but usually with larger limits and lower rates (Money.co.uk).

Why UK SMEs Use Revolving Credit Loans

Different industries use revolving credit facilities for different reasons. Recruitment agencies rely on them to bridge payroll gaps when contractors must be paid weekly but client invoices take 60+ days to settle. Marketing agencies use them to cover campaign costs upfront, ensuring suppliers and freelancers are paid before client invoices clear. Manufacturers and wholesalers draw on revolving credit to purchase raw materials in bulk, securing discounts without depleting cash reserves. IT service providers often use revolving facilities to cover unexpected project costs, ensuring delivery without cash-flow disruptions. Each sector benefits because the facility flexes with income cycles, reducing the pressure of fixed repayments (British Business Bank).

Benefits of a Revolving Credit Loan

Revolving credit loans give businesses the flexibility to borrow what they need, when they need it. They help smooth cash flow during unpredictable income periods and reduce reliance on fixed-term debt. Because interest is charged only on funds used, they can be cost-effective. Once repaid, funds are available again without having to reapply. For SMEs, this means an ongoing safety net that adjusts to their financial rhythm.

Drawbacks and Risks

Despite their advantages, revolving credit loans do have risks. Facilities may come with annual or renewal fees, and interest rates are often higher than secured loans. Because funds are always available, businesses may over-borrow and fall into dependency. Credit limits are often smaller than traditional secured term loans, and providers can reassess or reduce limits at annual reviews. Many lenders also require a director’s personal guarantee, meaning business debts could impact personal finances if repayments fall behind. For SMEs, it’s important to weigh these risks carefully against the benefits (No1 Copperpot Credit Union).

Revolving Credit vs Other Funding Options

How does a revolving credit facility compare with other popular SME funding choices?

Revolving credit sits between an overdraft and a term loan, providing greater flexibility than a term loan and often larger limits and lower costs than overdrafts.

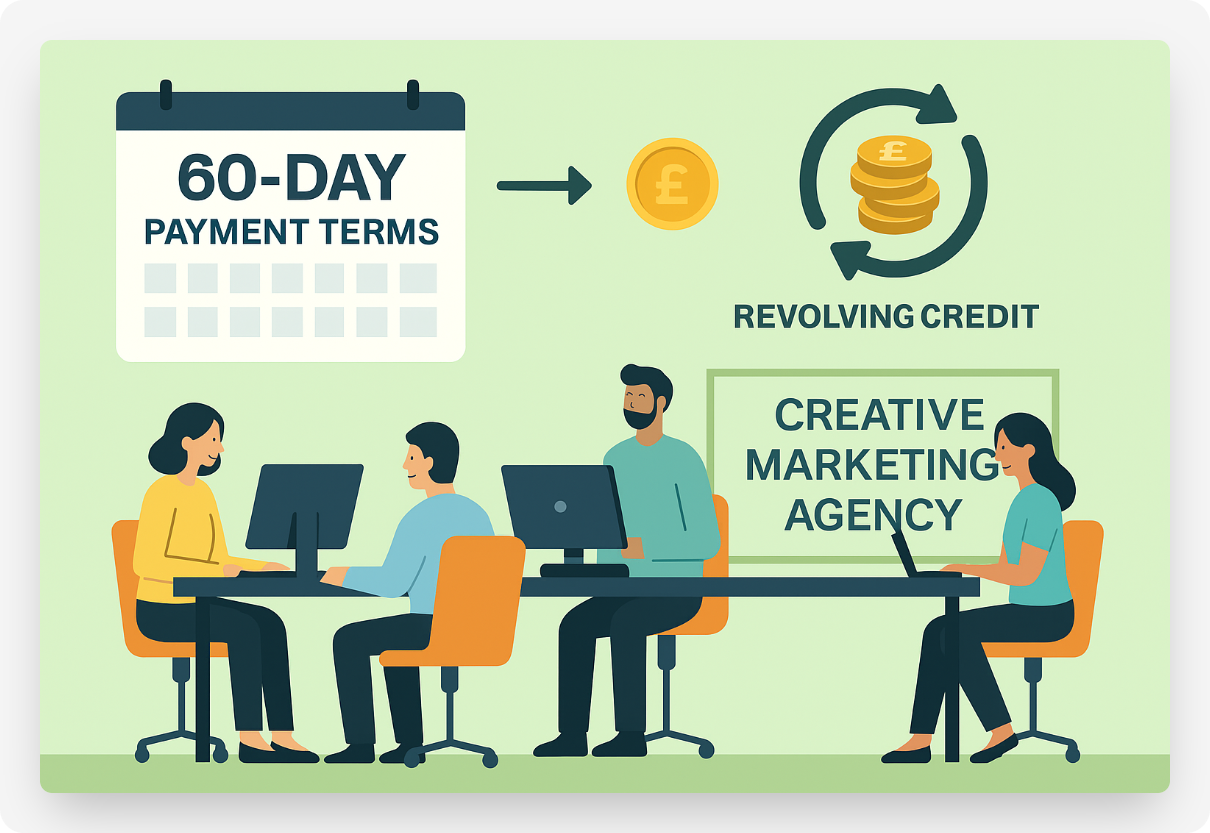

Real-World Example

Imagine a marketing agency with an annual turnover of £2 million. The agency often faces 60-day client payment terms while freelancers and suppliers must be paid within 14 days. By securing a £150,000 revolving credit facility, the agency covers payroll and supplier costs immediately. When client payments arrive, the agency repays the facility. This cycle repeats, ensuring consistent operations without long-term debt. For this business, revolving credit is less about borrowing for expansion and more about smoothing daily financial pressures.

Why Revolving Credit Is Growing Among SMEs

Revolving Credit vs Traditional Loans (2020–2025)

Over the past half decade, SMEs have quietly shifted away from fixed-term borrowing toward more flexible revolving credit. The SME Finance Monitor shows that the share of UK SMEs currently using an overdraft-style revolving facility edged up from about 10 percent in 2020 to 14 percent by early 2025, while reliance on traditional bank loans slipped from 15 percent to single digits over the same period. UK Finance’s Business Finance Review (Q1 2025) confirms the trend, noting that overdraft utilisation is recovering even as term-loan demand remains below pre-Covid norms.

Average Facility Size by Sector (2025)

Typical facility sizes vary sharply by sector. A recent Multifi case study records a £150 000 revolving line powering a fast-growing London marketing agency, while Multifi’s product page advertises unsecured limits up to £350 000, a ceiling often reached by larger IT-services consultancies. In recruitment, brokers such as Aurora Capital cite funding requirements that start from £5 000 and run to £500 000, placing the modal draw for payroll-heavy agencies around £75 000 – £100 000. Manufacturing firms, which must buffer longer production cycles and stock costs, tend to push toward the upper end of what mainstream lenders call small-business-friendly limits; sector guides put the typical cap near £250 000. Across the Atlantic, fintech platforms such as North One set comparable unsecured lines up to $250 000, underscoring how £250 000 has become an accepted working-capital benchmark for mid-market producers. Legal practitioners also treat £250 000 tranches as a standard building block inside larger revolving-credit mandates, reinforcing that number as a market norm.

Trusted UK Providers

Some of the UK’s well-known revolving credit providers include

- MarketFinance, which offers flexible revolving credit integrated with invoice finance;

- Funding Circle, which provides revolving credit up to £250,000; and high street banks such as

- Lloyds and Barclays, which provide traditional revolving facilities with annual renewals.

When comparing providers, it’s important to review not just rates but fees, renewal terms, and any personal guarantee requirements.

Key Takeaways

Revolving credit loans give SMEs flexible access to short-term funding that adapts to cash-flow cycles. They help businesses pay suppliers, meet payroll, and fund projects without locking into long-term debt. While costs and risks exist, particularly around renewal reviews and potential personal guarantees, their flexibility makes them invaluable for service-based and cash-flow-sensitive sectors.

Final Thoughts and Next Steps

Revolving credit loans are becoming an essential part of the SME funding toolkit in the UK. They offer flexibility and peace of mind for service-sector businesses and beyond. However, businesses must compare options carefully and manage borrowing responsibly.

If you want to see how a revolving credit loan compares to other flexible finance options, start by using Funding Agent’s business loan calculator or exploring alternatives like invoice financing and unsecured business loans. By weighing these choices side by side, you can find the funding that best supports your business’s growth and stability.

FAQs

Not exactly. While both let you borrow and repay flexibly, revolving credit usually offers higher limits and lower rates than business credit cards.

Most UK providers can approve revolving credit facilities within a week, and funds are often available as soon as the agreement is signed.

Eligibility checks are usually soft searches, so your credit score won’t be impacted until you formally apply. Using and repaying the facility responsibly can even strengthen your profile.

Recruitment agencies, marketing firms, IT service providers, and manufacturers are the main beneficiaries. Recruitment firms need it to cover payroll before invoices are paid, while manufacturers and wholesalers use it for raw material purchases. Marketing and IT businesses lean on it to manage unpredictable project expenses.

Costs vary by lender, but interest usually falls between 6% and 15% annually, with possible fees for arrangement or renewal. Because you only pay interest on what you use, it can be cheaper than a fixed loan if managed well.

Facilities are often reviewed annually. The lender can choose to renew, reduce, or withdraw the facility depending on your business performance and credit standing