Choosing Between Asset Finance and a Business Loan in 2025

With borrowing costs shifting and approval rates tightening, choosing the right type of finance is more critical than ever for UK businesses. Whether you're eyeing new equipment or need to cover broader operating costs, understanding the trade-offs between asset finance and business loans can help you make the smartest move for your bottom line.

Why the Right Funding Choice Matters in 2025

Interest rates on new SME loans peaked at 7.65% in mid-2024 before easing to 7.16% by Q4. But that doesn’t mean borrowing is easy. Approval rates for small business loans have dropped to around 50%, down from nearly 80% in 2018. For many, choosing the right product is the key to unlocking funding at all.

The new Growth Guarantee Scheme (GGS), running through March 2026, gives lenders a 70% government-backed guarantee. That can make both asset finance and business loans more accessible, especially for SMEs needing up to £2 million.

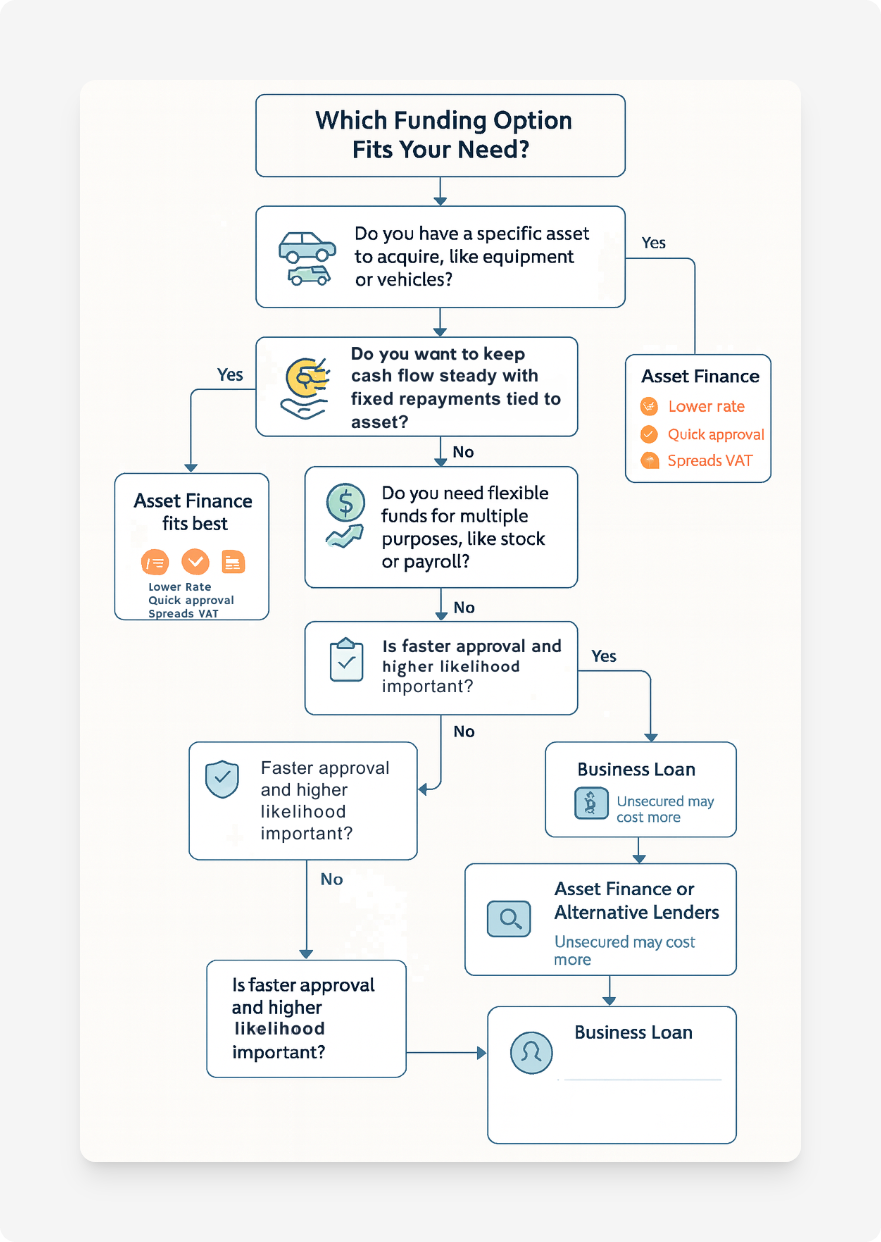

Asset Finance vs Business Loan – At a Glance

Here’s a quick breakdown of what each funding type is for:

- Asset Finance: Used to buy or lease tangible assets like vehicles, equipment, or machinery. The asset itself secures the funding. Learn more here.

- Business Loan: A flexible lump sum used for general purposes, hiring, stock, marketing, payroll, or even multiple smaller assets. Learn more here.

Which one suits you depends on your purpose, flexibility needs, and whether you want to preserve your working capital.

Total Cost Comparison

Comparing costs goes beyond the headline interest rate. Here’s what to factor in:

- Rates: Asset finance can offer lower rates due to built-in collateral. Business loans may be higher, especially unsecured loans.

- Fees: Look for arrangement, documentation, and early settlement fees.

- VAT Timing: HP usually requires full VAT upfront; leases spread it across payments. If VAT timing is a concern, consider VAT loans.

- Tax Relief: HP and long leases allow capital allowances. Operating leases count as a deductible expense.

Example: Buying a £50k machine through HP vs a business loan? The upfront VAT, monthly costs, and tax relief will vary significantly.

Tax and VAT Treatment Explained

If you own the asset, via hire purchase or a qualifying long lease, you may claim capital allowances, including the Annual Investment Allowance (AIA) of £1 million or full expensing on new equipment. This can slash your tax bill.

VAT treatment also differs:

- HP: VAT is charged upfront as if you're buying the asset. More here.

- Lease: VAT is spread across rentals. Car leases typically only allow 50% VAT recovery. More here.

What Lenders Look For

Lenders have become more cautious. Business loans typically require:

- Bank statements and filed accounts

- Business plans and forecasts for newer companies

- Personal guarantees for unsecured loans

Asset finance is often easier to approve, especially if the asset is essential and has a clear resale value. You'll usually need a quote or invoice for the item upfront.

With GGS support, both types may be easier to access if you qualify.

Real-World Scenarios

Buying a CNC machine? Asset finance via HP might be best. You’ll get capital allowances and match payments to the machine’s life.

Launching a new store? Use a business loan to cover fit-out, staff, stock, and marketing, all under one facility.

Upgrading to an EV fleet? Compare lease vs contract hire. Leasing spreads VAT and may offer more flexibility, while HP enables ownership.

Your 2025 Funding Checklist

- What’s the purpose, asset-specific or general use?

- Can you reclaim VAT or access capital allowances?

- Do you want to own the asset?

- How would early settlement or refinancing affect you?

- Are you comfortable with a personal guarantee?

- How will monthly payments affect your cash flow?

Final Thoughts

There’s no one-size-fits-all. Asset finance helps businesses scale without draining cash flow. Business loans offer the flexibility to handle multiple needs. Understand your objective, weigh the costs, and align the structure to your business model.

If you’re still unsure, contact us or use our finance comparison tool to model both options side by side.