Funding Options For Restaurants And Hospitality in the UK

.png)

Running a restaurant, bar or hotel in the UK is capital intensive and incredibly sensitive to costs. The hospitality sector now includes more than 170,000 businesses across the UK, and many venues are operating on thin margins while facing higher wages, energy bills and business rates. Recent research from the House of Commons Library shows that hospitality openings and closures have been volatile since 2020, which makes access to the right type of finance more important than ever.

This guide walks through the main funding options available to UK restaurants and hospitality businesses, when each one is useful, and what to think about before you apply. It is written for owners and finance managers who want to protect cash flow, invest in growth and avoid expensive mistakes.

Why funding is such a big issue for UK hospitality

The last few years have been tough for hospitality. Rising food prices, higher wage costs and energy volatility have squeezed margins. Industry bodies warn that tax and cost pressures are contributing to venue closures, especially among independent pubs and restaurants. At the same time, banks have tightened their criteria and are more cautious about lending to small businesses in general. Surveys of small business finance intermediaries suggest that more than four out of five advisers see gaps in the supply of finance for UK SMEs, and the challenge is even greater for start ups that have limited trading history. You can read a summary of these trends in the British Business Bank SME Intermediary Research.

Restaurants and hospitality venues feel these gaps first. They rely on predictable footfall and card spend, yet their costs, from ingredients to insurance, are largely fixed. Finance cannot fix a broken business model, but the right mix of facilities can help a viable venue to survive seasonal dips, fund refurbishments and keep investing in the customer experience.

What do restaurants and hospitality venues need funding for?

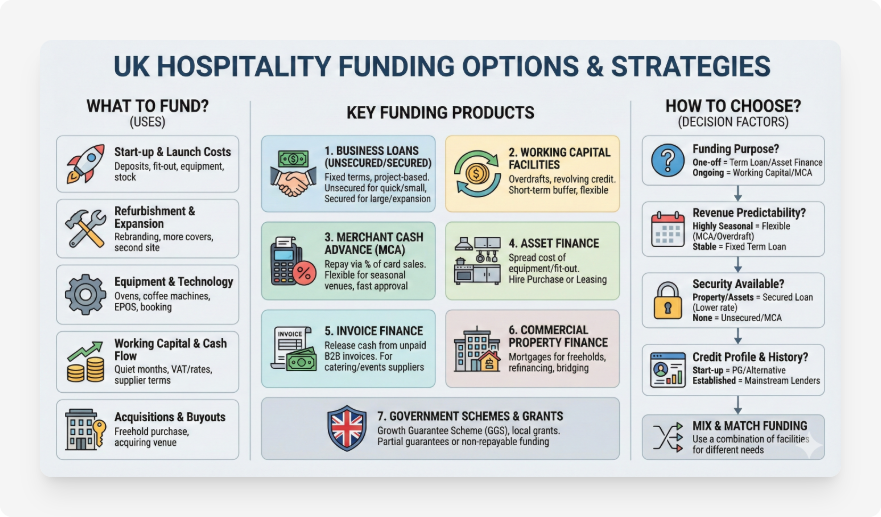

Before you look at specific products, it helps to be clear about what you are trying to fund. Hospitality businesses typically use external finance for:

- Start up and launch costs, such as deposits, fit out, licences, kitchen equipment and initial stock.

- Refurbishment and expansion, for example rebranding an existing site, adding more covers or opening a second location.

- Equipment and technology, including ovens, refrigeration, coffee machines, EPOS systems, booking platforms and delivery integrations.

- Working capital and cash flow, to bridge quieter months, cover VAT or rates bills, or manage supplier terms.

- Acquisitions and buy outs, such as buying the freehold or acquiring another venue.

Once you know whether you are dealing with a one off investment or an ongoing cash flow need, you can match the funding to the job it needs to do.

1. Unsecured and secured business loans

Business loans are one of the most common ways to fund restaurants and hospitality venues. Lenders offer both unsecured and secured facilities:

- Unsecured business loans are based on the strength of your trading history and credit profile rather than specific assets. They are typically used for smaller amounts and shorter terms, for example to fund a refit or marketing campaign. Specialist hospitality lenders and finance brokers such as Active Business Finance and Millwood Finance highlight unsecured loans as a flexible option when you need funding quickly.

- Secured business loans require security, such as a property, debenture or other assets. In return, they can offer larger loan sizes and lower rates. For established groups with multiple sites or a strong balance sheet, secured lending can fund significant expansion or a freehold purchase.

Business loans are usually repaid in fixed monthly instalments over one to seven years. They work well where you have a clear project with a defined budget, such as refurbishing a dining room or building an outdoor seating area. They are less suitable as a permanent solution to ongoing cash flow problems, because you are committing to regular repayments regardless of sales.

2. Working capital and cash flow facilities

Hospitality is seasonal by nature. Many restaurants and hotels see peaks around holidays and local events, followed by quieter periods. To smooth these ups and downs, you can use working capital products such as:

- Revolving credit facilities or lines of credit, which let you draw down, repay and redraw within an agreed limit.

- Business overdrafts, which can be useful as a short term buffer if your account dips into the red.

- Short term working capital loans, which are repaid over six to eighteen months and are designed to cover temporary gaps in cash flow.

Guides from sector specialists such as Swoop and Novuna Business Cash Flow point out that cash flow problems are a leading cause of restaurant failure. A well structured working capital facility, based on realistic forecasts, can give you headroom so you are not forced into last minute, high cost borrowing.

3. Merchant cash advance for card taking venues

Merchant cash advances are popular in hospitality because repayments flex with your card sales. Instead of paying a fixed monthly amount, you agree to pay a small percentage of each card transaction until the advance plus fees have been repaid. This structure is a good fit for restaurants, bars and cafes that take most of their revenue through card terminals.

According to finance providers such as Touch Financial and sector lenders listed by brokers like Rangewell, a merchant cash advance is usually unsecured and can be approved quickly, based mainly on your historic card takings.

Advantages for hospitality include:

- Repayments that rise and fall with trade, which can relieve pressure in quieter weeks.

- No need to provide physical security, because the provider looks at your card revenue instead.

- Fast decisions and minimal paperwork, useful when you need to act quickly.

Points to watch include the total cost of the advance compared with a standard loan, and the impact on your card income during busy periods. It is important to understand the factor rate and to compare offers from more than one provider so that you do not pay more than you need to.

4. Asset finance for kitchen and venue equipment

Restaurants and hotels rely on high quality equipment, from commercial ovens and extraction systems to furniture, EPOS and booking technology. Buying these assets outright can drain cash reserves. Asset finance lets you spread the cost over the useful life of the equipment.

Specialist hospitality finance firms, such as PMD Business Finance, Active Business Finance and Millbrook Business Finance, highlight several benefits:

- You can match repayments to the revenue the equipment helps to generate.

- You preserve working capital for wages, stock and marketing.

- In some cases, you may be able to fund soft assets such as fit out and furnishings alongside hard assets.

Common structures include hire purchase, where you own the asset at the end of the term, and leasing, where you rent it and may upgrade at renewal. Each structure has different tax and ownership implications, so it is wise to discuss them with your accountant.

5. Invoice finance for hospitality suppliers and event businesses

Not every hospitality business operates on a pay at table model. If you run an event catering company, supply food and drink to corporate clients, or host weddings and conferences, you may issue invoices on terms such as 30 or 60 days. This can create cash flow pressure, especially if you need to pay staff and suppliers before you are paid yourself.

Invoice finance releases a percentage of the value of your unpaid invoices, often within 24 hours of raising them. Lenders listed on sector pages like Rangewell and hospitality finance guides from brokers such as PMD and Novuna note that invoice finance can be a useful tool for venues and suppliers that have lumpy, project based income.

Invoice finance works best when you invoice business customers rather than consumers, and when your contracts and credit control processes are strong. It can be structured as a confidential facility, where your customers are unaware of the funding, or a disclosed arrangement with the lender collecting payments.

6. Commercial mortgages and property finance

If you are buying the freehold of a restaurant, hotel or bar, or refinancing an existing mortgage, commercial property finance comes into play. Brokers that specialise in hospitality, such as Rangewell and PMD Business Finance, arrange:

- Owner occupier commercial mortgages, where your business trades from the property.

- Investment mortgages, if you let the premises to another operator.

- Bridging finance, to secure a property quickly before refinancing onto a longer term facility.

Property finance is usually secured against the building itself and sometimes backed by additional security. Lenders will assess trading performance, location, planning use class and the experience of the operator as well as the property value.

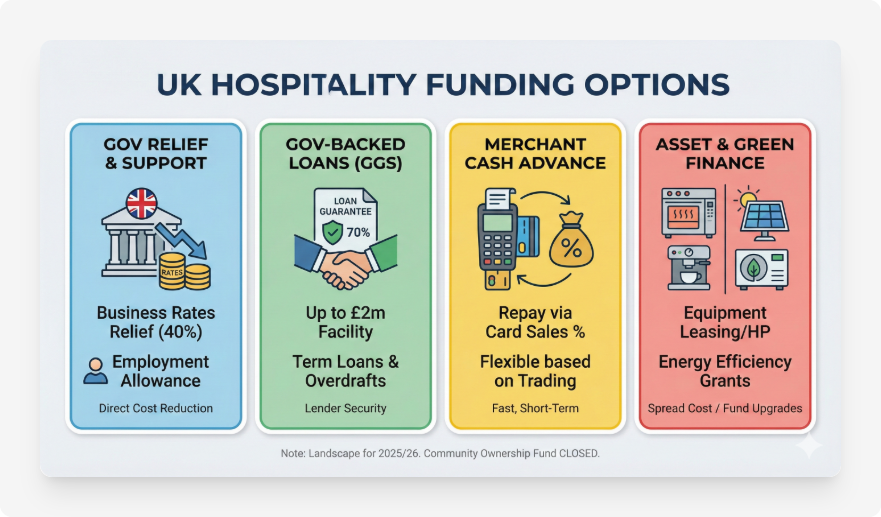

7. Government backed schemes, guarantees and grants

The UK government has periodically offered schemes to help viable SMEs access finance. The original Recovery Loan Scheme supported businesses after the pandemic and has now been succeeded by the Growth Guarantee Scheme, which is delivered through the British Business Bank and accredited lenders. According to guidance summarised by bodies such as the Institute of Chartered Accountants in England and Wales and advisory firms like HLC Accountants, the Growth Guarantee Scheme will run until at least March 2026, providing government backed guarantees on loans of up to £2 million per business in most parts of the UK.

These schemes do not remove your responsibility to repay, but they give lenders a partial guarantee, which can make them more willing to support businesses that lack property security. Hospitality venues that were affected by the pandemic or rising costs may be able to access term loans, overdrafts, asset finance or invoice finance under the scheme, subject to eligibility and lender assessment.

Alongside national schemes, there are often local grants and incentives aimed at tourism, regeneration or energy efficiency. VisitBritain maintains an overview of funding programmes relevant to tourism and hospitality on its business advice pages, which are a useful starting point when you are looking for grants rather than loans. You can explore current opportunities on the VisitBritain funding hub.

8. How to choose the right funding mix

With so many options on the market, it is easy to feel overwhelmed. A simple way to narrow the choices is to ask four questions about your venue:

- What is the funding for? One off investments such as a new kitchen are usually best matched with term loans or asset finance, while ongoing cash flow needs point to revolving credit, overdrafts or merchant cash advances.

- How predictable is your revenue? Highly seasonal or event driven businesses benefit from flexible repayments, whereas stable venues can often access better pricing with fixed term loans.

- What security can you offer? If you have property or strong assets, secured lending may give you access to larger amounts at lower cost. If not, unsecured loans and merchant cash advances are more likely to be realistic.

- What is your credit profile and trading history? Start ups and recently opened venues may need to rely on personal guarantees or alternative products, whereas established restaurants with strong accounts can usually access mainstream lenders.

It is rarely wise to rely on a single facility for everything. Many successful operators use a combination, for example a commercial mortgage on the property, asset finance for kitchen equipment, and a working capital line to smooth seasonal cash flow.

How Funding Agent can help restaurants and hospitality businesses

Understanding the options is one thing, navigating individual lenders is another. Each bank and specialist lender has its own appetite for different types of venue, preferred deal sizes and credit criteria. Applying one by one is slow and can lead to unnecessary declines on your credit file.

Funding Agent is a UK business finance platform that connects restaurants, bars, hotels and hospitality suppliers with a wide panel of lenders. Instead of filling out multiple forms, you complete one digital application. We use data enrichment and lender criteria to narrow the field, then route your details to lenders that are more likely to say yes for your type of venue and funding requirement.

For hospitality businesses, that can mean:

- Comparing unsecured loans, secured loans, merchant cash advances, asset finance and invoice finance from different providers side by side.

- Saving time on paperwork, since much of your application data can be pre filled and reused across lenders.

- Getting support from people who understand how lenders view restaurants and hospitality risk, so you can position your application clearly.

Our goal is not just to help you find money, it is to help you find sustainable finance that fits the rhythm of your venue and leaves room for future investment.

Next steps

If you are planning a refurbishment, dealing with rising costs, or looking at expansion, the best time to review your funding options is before you are under pressure. Map out your cash flow, talk to your accountant, and then explore facilities that match your plans rather than simply reacting to the first offer you receive.

When you are ready to see what is available, you can start an application with Funding Agent in a few minutes. Share some basic details about your business, your recent trading and what you need funding for, and we will match you with lenders that specialise in supporting UK restaurants and hospitality businesses.

FAQs

UK hospitality businesses can access unsecured and secured business loans, working capital facilities, merchant cash advances, asset finance, invoice finance and commercial property finance, along with government backed schemes such as the Growth Guarantee Scheme that support viable SMEs through accredited lenders.

For refurbishments and fit outs, term loans and asset finance are often the best fit. Asset finance lets you spread the cost of kitchen equipment, EPOS systems and furniture over the life of the assets, while unsecured or secured business loans can cover wider project costs such as design, contractors and branding.

A merchant cash advance gives you an upfront lump sum that you repay as a fixed percentage of future card takings, instead of fixed monthly repayments. This can suit restaurants, bars and cafes where most customers pay by card, because repayments naturally fall in quieter periods and rise when trade is strong.

Start up or newly opened venues may still be able to access funding, but options are usually more limited and may require personal guarantees. Lenders focus on factors such as personal credit history, business plans, projected cash flow and any security available. Some government backed schemes and start up programmes offer unsecured funding for newer businesses that meet their criteria.

Security depends on the product. Commercial mortgages and many larger loans are secured on property or other assets. Asset finance is usually secured on the equipment being funded. Merchant cash advances are typically unsecured and based on your card revenue, and some working capital loans are offered on an unsecured basis, although personal guarantees are common for SMEs.

Start by clarifying what you need the money for, how stable your revenue is, what assets you can offer as security and how quickly you need the funds. Short term cash flow gaps often point towards working capital facilities or merchant cash advances, while long term investments such as property or major equipment are better matched with commercial mortgages or asset finance. Speaking with a specialist broker that understands hospitality can help you compare costs and structure a mix of products that fits your venue.