Understanding Personal Guarantees in Business Loans

.png)

A personal guarantee is a binding promise by a business owner or director to repay a loan if the business defaults. This means if the company cannot meet its debt obligations, the guarantor is personally liable. It acts as a fallback for lenders, who can recover losses from the guarantor’s assets. This type of arrangement is particularly common among SMEs and startups without a strong credit history or collateral. Learn more from the British Business Bank or NerdWallet UK.

Why Lenders Require Personal Guarantees

Lenders use personal guarantees to reduce risk. It provides a safety net if the business fails to repay. This is especially common for unsecured business loans or new businesses. When company assets are not enough, the lender has legal grounds to pursue the guarantor’s personal finances. In turn, this makes it easier for businesses with limited trading history to secure funding.

How Guarantees Work Across Loan Types

Unsecured Loans

With no collateral involved, unsecured loans often rely on personal guarantees to protect the lender. These are typical in short-term loans and lines of credit. Lenders like Funding Circle frequently require director guarantees. Personal guarantees here are seen as a substitute for physical security, offering lenders confidence that a loan will be repaid even if the business fails. This allows earlier-stage businesses to access capital without needing to pledge hard assets.

Secured Loans

Even when loans are backed by business assets, personal guarantees may be added to cover shortfalls if assets are insufficient. For example, if the sale of the secured asset does not fully clear the debt, the lender can pursue the guarantor for the remaining balance. This is especially relevant for depreciating assets or volatile markets. Personal guarantees in secured lending are often negotiated as a “top-up” measure and may be limited in amount, especially for directors with less equity in the business.

Invoice and Asset Finance

In invoice finance, performance guarantees may cover risks related to invoice disputes or fraud. These guarantees help ensure the business doesn’t overstate receivables or misrepresent payment timelines. In asset finance, a capped guarantee may be used for businesses with a weak credit profile or minimal trading history. Here, the equipment or vehicle being financed often serves as primary security, but the personal guarantee may be layered in as a condition for approval or better rates.

Government-Backed Loans

Under the UK Growth Guarantee Scheme, the government backs a portion of the loan, but the borrower and guarantors remain liable. Protections exist, such as restrictions on charges over directors' homes, but personal guarantees may still be required, particularly for loans above certain thresholds. These guarantees ensure that lenders remain cautious and engaged in due diligence, even when part of the risk is underwritten by the government. Additional perspectives: NatWest, ICAEW.

Personal Guarantee Policies by Lender Type

Different lenders have their own policies when it comes to personal guarantees. Traditional banks may be more flexible with established businesses, while peer-to-peer platforms often impose strict PGs due to the way loans are funded by multiple investors. Alternative lenders and government-backed schemes strike a balance by sometimes offering capped guarantees or excluding certain personal assets like a home. It’s important to ask early and negotiate terms where possible.

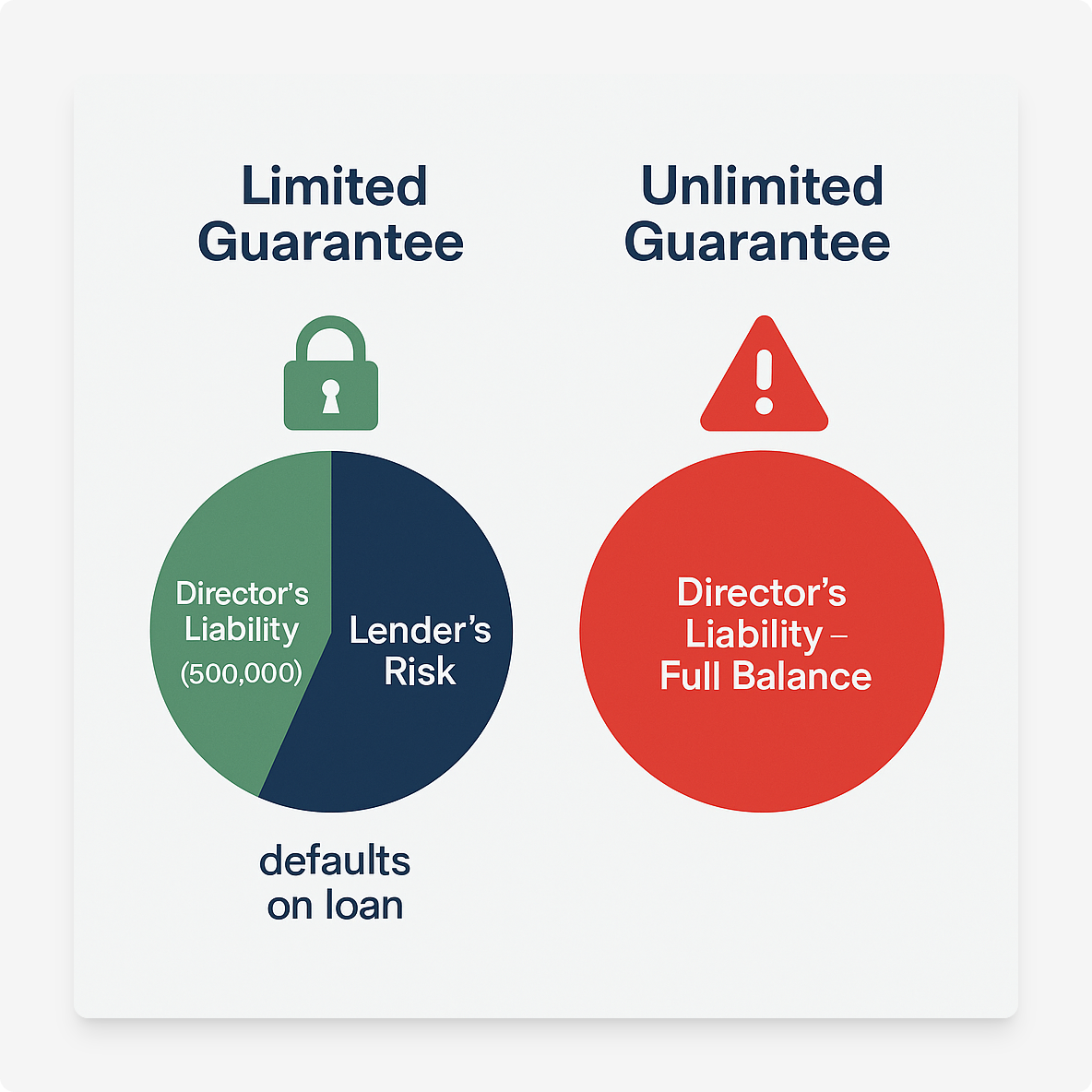

Limited vs Unlimited Guarantees

A limited guarantee caps the guarantor’s liability, either by a fixed amount or percentage. An unlimited guarantee covers the entire outstanding loan plus associated costs. Most SMEs seek limited guarantees, but lenders may push for broader coverage depending on the risk profile. See guidance from Myers Solicitors and Investopedia.

Joint and Several Liability Among Directors

When multiple directors sign a guarantee, they are usually jointly and severally liable. This means the lender can demand the full repayment from any one of the signatories. Internal agreements between directors may split the liability, but the lender is not bound by these.

Key Risks for Guarantors

- Loss of personal assets, including savings and property.

- Damage to personal credit score.

- Risk of bankruptcy if unable to repay.

- Stress and strain on personal relationships.

How to Reduce Personal Risk

- Negotiate capped guarantees instead of unlimited ones.

- Use shared guarantees among multiple directors.

- Explore personal guarantee insurance to reduce exposure.

- Take independent legal advice to understand full implications.

Policy and Regulatory Considerations

Regulators and trade bodies like the British Business Bank have raised concerns about the fairness of personal guarantees for microbusinesses. MPs have called for a review of lending practices that place undue burden on small company directors. Read reports in the Financial Times and The Guardian.

Quick Checklist Before You Sign

- Have you assessed the business’s ability to repay?

- Can you personally afford the repayments if the business fails?

- Is there a way to limit your liability?

- Have you discussed the risk with co-directors?

- Did you get independent legal advice?

Need Help Comparing Loan Offers?

Funding Agent helps SMEs understand personal guarantees, compare lenders, and secure funding with better terms. You can start your search using our funding request form, or check out our loan calculators to estimate repayments and liability under different scenarios.

FAQs

A limited guarantee caps your liability to a specific amount. An unlimited guarantee makes you responsible for the full loan balance plus interest and costs.

Sometimes. You may avoid it with strong business collateral or by negotiating with the lender. But many SME loans require it, especially if unsecured.

They are usually jointly and severally liable. This means the lender can chase any one director for the full debt.

It can reduce your financial exposure if you’re forced to repay. However, it may not cover the full amount and often comes with conditions.

Yes. Independent legal advice ensures you understand the risks and may be a lender requirement.