What Is Invoice Finance? A Smart Way for UK SMEs to Improve Cash Flow

.png)

Late payments cost UK small businesses over £23 billion a year in lost revenue and productivity. For many SMEs, unpaid invoices tie up vital working capital that could otherwise be used to pay staff, invest in stock, or grow operations. That’s where invoice finance comes in, a flexible, fast funding solution that helps businesses unlock cash from their unpaid invoices.

In this guide, we’ll break down exactly what invoice finance is, how it works, the pros and cons, and how UK businesses can qualify and choose the right provider.

What Is Invoice Finance?

Invoice finance allows businesses to receive most of the money owed on their invoices immediately, usually around 85–90%. Instead of waiting weeks or even months, you can get paid within just a day or two, which helps maintain healthy cash flow.

Think of it as borrowing against money you're already owed.

Before diving into your options, it helps to see how invoice finance stacks up against other popular funding methods. The dashboard below offers a quick visual comparison—highlighting key differences in speed, collateral requirements, and flexibility. Whether you're considering a loan, overdraft, or asset finance, this snapshot helps you understand where invoice finance stands out.

How Does Invoice Finance Work?

When you send an invoice to your customer, you also share this invoice with an invoice finance provider. The provider then pays you up to 90% of that invoice amount within 24–48 hours. When your customer eventually pays the invoice, the provider sends you the remaining balance minus their small fee.

For example, if you have a £10,000 invoice, you might receive £9,000 immediately. Once your customer pays the invoice, you get the remaining £1,000 minus a small fee for the service.

You can also compare invoice finance with other funding options to understand which suits your business best.

Types of Invoice Finance

There are two main types of invoice finance:

Invoice Factoring

With factoring, the provider takes care of collecting payments from your customers for you. This means you spend less time chasing payments, and more time growing your business. Factoring can be very helpful for smaller businesses without a dedicated finance team.

Invoice Discounting

Discounting is more discreet. You continue handling customer relationships and collecting payments, so your customers won’t know you're using invoice finance. This can be valuable for businesses that want to maintain direct customer interactions.

You can also choose to fund specific invoices (selective factoring) or use reverse factoring, where your suppliers get paid immediately, and you repay the finance provider later.

To better understand your choices, explore our complete guide to business funding options.

Who Benefits from Invoice Finance?

Invoice finance is ideal for businesses regularly invoicing other businesses, like recruitment firms, marketing agencies, wholesalers, or manufacturers. It especially suits companies facing rapid growth or those dealing with seasonal fluctuations.

For example, recruitment companies use invoice finance to reliably cover weekly wages, even when client payments are slow. Marketing agencies can take on large projects without worrying about cash shortages.

If you’re unsure whether your sector qualifies, browse the invoice finance by industry section for tailored guidance.

Key Benefits and Things to Think About

Invoice finance offers immediate cash flow, grows with your business, and means you rely less on traditional loans or overdrafts.

However, there are costs involved, and some businesses might worry about how customers perceive invoice factoring. It’s important to understand clearly any fees or conditions before you commit.

If invoice finance doesn’t seem the right fit, you might consider an unsecured business loan or asset finance to meet your funding needs.

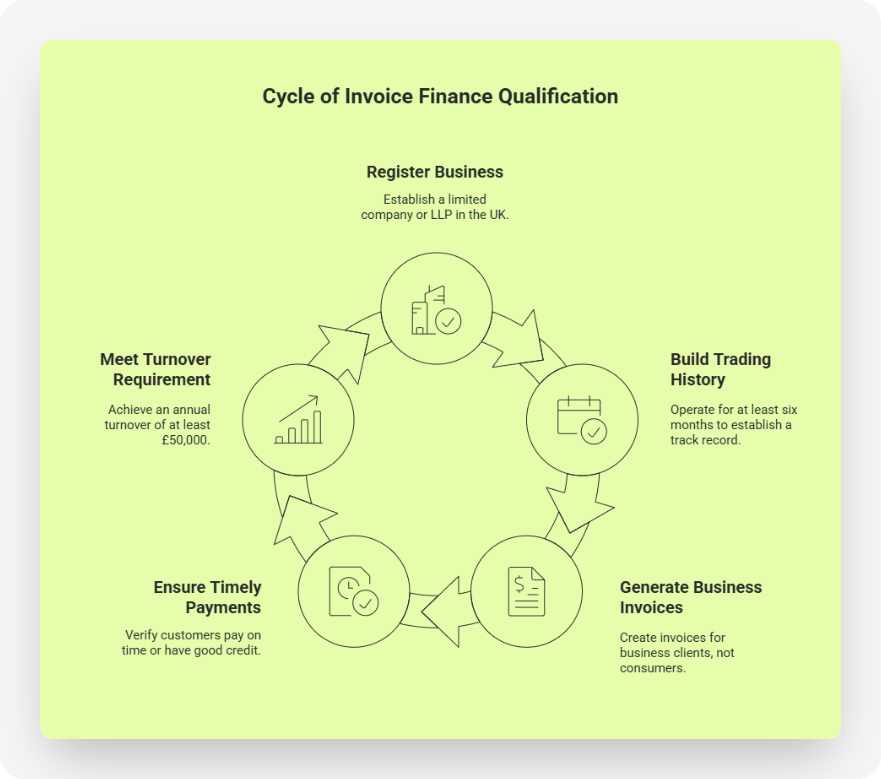

Qualifying for Invoice Finance

To use invoice finance, typically your business should have been operating for at least six months, have an annual turnover of over £50,000, and invoice reliable businesses. Providers will look at your customers' payment history, your industry, and your financial stability.

To estimate how much you might qualify for, use our business loan calculator.

How Invoice Finance Helps Your Cash Flow

How Much Can You Borrow?

How much you can borrow depends on your turnover. For instance, a business with £250,000 turnover might access up to around £225,000, whereas one with £1 million turnover might secure up to around £900,000. The funding grows as your sales increase, which makes invoice finance flexible.

Use our loan calculator to model what you could access based on your monthly invoices.

Estimate Your Invoice Finance Potential

Understanding how much you could unlock from your unpaid invoices is key to planning cash flow confidently. Use our free invoice finance calculator below to get a quick estimate of your potential advance based on your average monthly invoicing. It’s fast, simple, and requires no personal details. Whether you're considering factoring or discounting, this tool gives you clarity before you commit.

Comparing Invoice Finance to Other Options

Compared to loans or overdrafts, invoice finance provides faster cash, is flexible, and usually easier to access without needing heavy collateral or guarantees. Unlike fixed-term loans, it adjusts directly to your sales, making it ideal for businesses experiencing growth or variable income.

For a side-by-side breakdown, view our guide to alternative business funding.

Trusted Invoice Finance Providers in the UK

There are dozens of reputable providers in the UK. Some of the best include:

- Bibby Financial Services

- MarketFinance

- Close Brothers Invoice Finance

- Aldermore Invoice Finance

- Boost Capital

- Ultimate Finance

We’ve compared the best invoice finance providers to help you understand their strengths.

Is Invoice Finance Right for Your Business?

Invoice finance could be perfect if you regularly invoice customers and need reliable, flexible cash flow to manage and grow your business without worrying about slow-paying clients.

If you're in a fast-moving sector like recruitment, manufacturing or consultancy, visit our industry-specific funding hub to see what options are available.

How Funding Agent Makes Invoice Finance Easy

Funding Agent helps you easily compare invoice finance options tailored to your specific needs. Our simple online platform matches you with trusted lenders, ensuring you get clear and fair quotes without harming your credit score.

We also support term loans and asset finance, so you can explore all routes to growth in one place.

Find the Best Invoice Finance for Your Business →

Final Thoughts

Invoice finance is one of the most practical ways for UK SMEs to turn unpaid invoices into immediate growth capital. Whether you’re struggling with cash flow gaps or simply want to smooth working capital, this flexible funding model is well worth exploring.

Don’t let unpaid invoices stall your growth. With Funding Agent, you can unlock the cash tied up in your receivables and keep your business moving forward. Our platform connects you with trusted UK invoice finance providers in minutes, no hard credit checks, no paperwork headaches. You can check your eligibility instantly or use our Invoice Finance Calculator to see how much working capital you could access today.