Working Capital Loans vs Term Loans

.png)

Choosing between short term liquidity and long term investment is not a rate game, it is a fit question; if the challenge is timing, smoothing cash flow with working capital loans keeps payroll, stock, and VAT moving through seasonal dips, whereas if you are buying an asset or funding expansion that will pay back over years, a term loan spreads the cost into predictable instalments so planning stays clean; the right call rests on your cash cycle, the life of what you are funding, and how much security and documentation you are comfortable with.

Funding reality, seen in four quick charts

Use the tabs to compare market rates, typical term ranges, invoice finance advances, and how balances fall over time. Think of a local wholesaler borrowing £100,000, a 12 month working capital facility solves a timing crunch fast, while a 60 month term loan lowers monthly strain and keeps cash freer for payroll and stock.

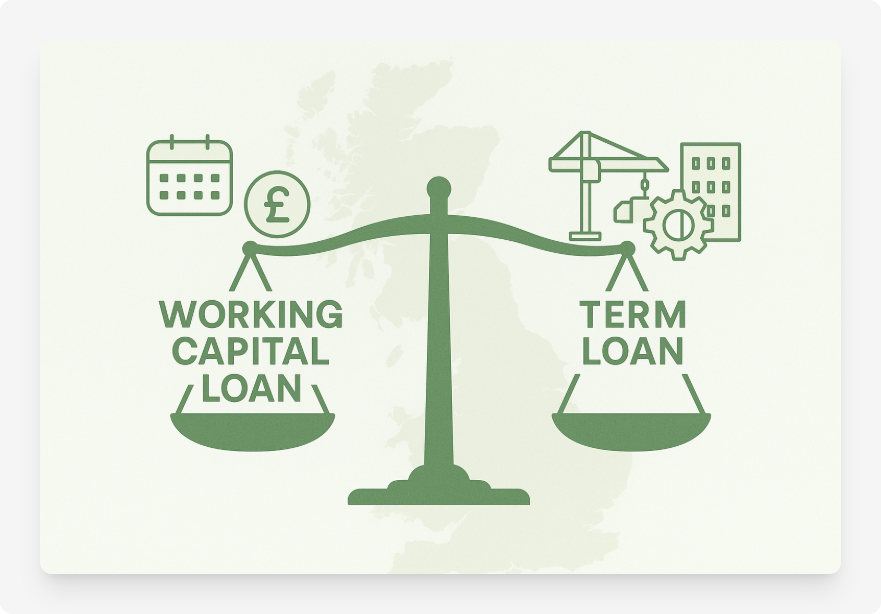

What each loan type is for

A working capital loan supports day to day needs when cash inflows and outflows do not line up, for example covering payroll, inventory, rent, or VAT during a slow collections cycle. UK guidance describes working capital finance as funding for the activities that keep the lights on, as in the British Business Bank overview that also discusses overdrafts and invoice finance in the same context.

A term loan fits larger projects with multi year benefit, such as machinery purchases or a premises refit, and the fixed schedule can simplify planning when cash flows are stable, which aligns with the British Business Bank’s explanations of common loan types including term debt used by UK SMEs.

Quick comparison

Pros and cons at a glance

Working capital loans, pros

- Addresses timing gaps quickly when income is uneven within the month or quarter.

- Faster applications and simpler documentation than longer term facilities in many cases.

- Can align with debtor cycles when combined with receivables solutions like invoice financing in B2B models, improving liquidity during slow collections.

Working capital loans, cons

- Shorter terms and higher perceived risk often translate into higher pricing than secured term debt, as general guides on working capital explain on the British Business Bank’s working capital pages where different structures are outlined.

- Using a short term facility for a long lived need can create refinancing pressure before the benefit is realised, which strains liquidity during downturns.

- Unsecured facilities may rely on personal guarantees, so directors carry contingent risk that should be weighed against alternatives.

Term loans, pros

- Fixed repayments support budgeting over years, which helps when cash flows are predictable.

- Security on assets can unlock larger amounts and longer terms, as summarised in UK guidance on secured and unsecured loan types for SMEs.

- When used for assets with clear payback, the cost per unit of benefit can compare favourably with shorter facilities that price for speed and flexibility.

Term loans, cons

- Longer processes, more documentation, and potential covenants reduce flexibility if plans change mid term.

- Charges over assets can limit future borrowing capacity, so growth plans should account for available headroom.

- Large obligations during weaker trading can stress cash flow, which is why scenario testing helps before committing.

When a working capital loan fits

Choose working capital when the challenge is timing rather than scale, for example supplier prepayments before receipts land or inventory builds ahead of a seasonal push, then validate affordability by modelling monthly costs in a working capital loan calculator while you test slower receipt assumptions.

Where delays are tied to unpaid invoices, advancing receivables through invoice financing can reduce reliance on generic short term borrowing, which often improves alignment with the working capital cycle.

When a term loan is more suitable

Choose a term loan when funding an asset or project with multi year benefits, such as equipment, fit outs, or an additional site, and keep the comparison grounded by reviewing how term loans typically structure repayments relative to asset life before you size the facility.

Costs, security, and documentation

Pricing depends on credit profile, security, and market conditions; longer term asset backed borrowing typically prices lower than short duration unsecured facilities, which aligns with UK explanations of business loan mechanics that discuss documentation, credit checks, and security.

Documentation also varies by product; working capital facilities often rely on receivables data and bank statements, while term loans may require valuations, statutory accounts, and detailed forecasts, so building a basic cash discipline first pays off when lenders assess readiness.

Cash flow impact and planning

Before deciding, create a simple forecast that includes a mild downside case and overlay repayments from both options, then compare headroom using practical steps from professional bodies like ICAEW, whose cash flow guidance encourages stress testing and cross functional visibility. If forecasts reveal pressure points, incorporating proven debt relief strategies can support better financial resilience.

Alternatives and complements to consider

If cash gaps are driven by slow paying customers, pairing a modest working capital line with invoice financing can scale with sales and reduce the need for repeated short term borrowing during busy periods.

If the requirement is asset heavy, compare a traditional term facility with approaches discussed in asset finance vs invoice finance so you can balance deposit sizes, ownership, and residual value against monthly cash flow.

A simple decision framework

- Define the need, timing gap versus asset or expansion, so the structure matches the problem.

- Match duration, short gap points to working capital, multi year benefit points to term debt with an appropriate schedule.

- Stress test, run a slower receipts case and a small revenue dip, then check coverage after adding fixed monthly costs.

- Choose structure, consider a revolving line or receivables backed option for timing issues, and a fixed schedule for long lived assets.

- Understand security, review guarantees, charges, and any covenants, then confirm you retain headroom for future borrowing.

FAQs

Working Capital Loans are intended to meet short-term operational expenses such as payroll, inventory, and utilities. Term Loans are designed for long-term investments like purchasing equipment, expanding facilities, or real estate acquisition.

Working Capital Loans usually have shorter tenures ranging from a few days to months with flexible repayment options aligned to business cash flow. Term Loans typically have longer fixed tenures from 1 to 15 years, with regular EMI payments.

Term Loans generally have lower or fixed interest rates but often require collateral. Working Capital Loans can have variable or higher interest rates but are frequently unsecured, reducing risk for the borrower

Working Capital Loans tend to be easier to get especially for borrowers with good credit scores due to their short-term and unsecured nature. Term Loans usually require more documentation and financial scrutiny.

Term Loans generally provide larger sums suitable for major investments with longer repayment periods, while Working Capital Loans tend to be smaller amounts tied to the business’s operational turnover and short-term needs.

Working Capital Loans generally have more flexible and easier credit requirements, often accessible to businesses with good credit scores and sometimes unsecured. Term Loans typically require stronger credit profiles, extensive documentation, and collateral since they involve larger amounts and longer repayment periods.