Asset Finance vs Invoice Finance: Which Is Right for Your Business in 2026?

.png)

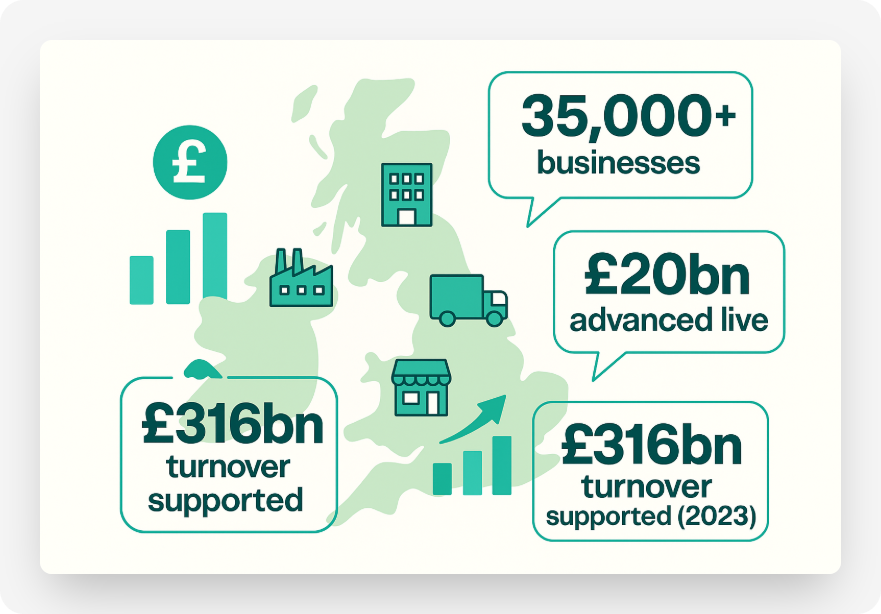

UK SMEs continue to struggle with late payments and capital expenditure needs. According to UK Finance, Invoice Finance and Asset-Based Lending supported over £316 billion in client turnover in 2023 across 35,000 firms. This shows just how vital both facilities have become for keeping the UK’s growth engine alive. But which tool is better for your business, asset finance or invoice finance? The answer depends on whether your pain point is delayed cash inflows or large capital purchases. In this blog we break down definitions, mechanics, costs, sector relevance, and help you decide which option makes sense in 2025.

What Are Asset Finance and Invoice Finance?

Invoice Finance (IF)

Invoice Finance, also known as debtor finance, allows B2B businesses to unlock up to 90 percent of their invoice value within 24–48 hours by selling or advancing against unpaid client invoices. Depending on the product (factoring vs discounting), the lender may take charge of collections, or the business retains confidentiality. Approval hinges primarily on the creditworthiness of your customers, not on your own cash flow or assets, making it ideal for trading firms with good customer credit who need cash fast (LinkedIn).

Asset Finance (AF) / Asset‑Based Lending (ABL)

Asset Finance and ABL extend financing beyond receivables to include machinery, equipment, inventory, or real estate as collateral. They can take forms like hire‑purchase, finance leases, sale‑and‑leaseback, or revolving credit lines secured against assets you already own. Funds are released in proportion to the value of the borrowing base, enabling support for growth, M&A, or turnaround finance (WF Financial Solutions, 1stcommercialcredit.com).

Key Differences: Funding Structure, Cost, and Speed

Cost Breakdown (Invoice vs Asset Finance)

The chart shows how Invoice Finance fees average ~2.5% of invoice value, while Asset Finance’s all-in cost (margin + arrangement, valuation, legal fees) can reach ~5.3% annually. Both can be competitive depending on your facility size and sector.

Which Works Best for Each Sector?

Here’s a sector-by-sector comparison of how Invoice Finance and Asset Finance perform, showing which one works best and why.

Recruitment Agencies

- Invoice Finance works best.

Recruitment firms often have to pay temps and contractors weekly, but clients may take 30–90 days to pay invoices. Invoice Finance bridges this gap by advancing up to 90% of invoice value almost immediately. This ensures wages are covered without drawing on overdrafts. - Asset Finance is less common here, but can still help agencies fund back-office systems, payroll platforms, or office IT on manageable terms.

Manufacturers

- Asset Finance works best.

Manufacturers frequently need expensive machinery, vehicles, and warehouse fit-outs. Asset Finance allows them to spread the cost of these purchases over 3–7 years while keeping working capital free for raw materials and payroll. - Invoice Finance can still be useful if they sell to wholesalers or distributors on long credit terms, as it bridges the cash-flow gap while waiting for large client payments.

Marketing & Creative Agencies

- Invoice Finance works best.

Agencies face long client payment terms (60–90 days) but need immediate funds for campaigns, media spend, and freelancers. Invoice Finance unlocks capital from invoices, ensuring campaigns can launch without delay. - Asset Finance is secondary—sometimes used for high-value kit like cameras, servers, or studio refurbishments.

IT Services & MSPs (Managed Service Providers)

- Asset Finance works best.

IT firms often need to refresh servers, laptops, or data-centre equipment every few years. Asset Finance smooths these lumpy capital expenses into predictable monthly costs. - Invoice Finance can also help service providers with recurring contracts to manage cash flow if clients are slow to pay.

Logistics & Distribution

- Both are often combined.

Asset Finance funds fleets of vans, HGVs, and warehouse equipment, spreading costs over their useful life. Invoice Finance ensures fuel, drivers, and maintenance bills are paid while waiting on slow corporate customers.

This dual-approach is common in haulage, where margins are tight and upfront vehicle costs are steep.

Professional Services (Law, Accounting, Consultancy)

- Invoice Finance is often more relevant.

Client invoices in legal and consulting sectors are usually large and can take months to clear. Invoice Finance advances the cash needed for payroll and rent. - Asset Finance is less critical here, except for IT or office fit-outs, but can still be useful for growing firms scaling infrastructure.

Retail & Hospitality

- Asset Finance works best.

Hotels, restaurants, and retailers need heavy upfront investment in kitchens, refurbishments, and EPOS systems. Asset Finance spreads those costs. - Invoice Finance is less common, as B2C transactions don’t generate trade invoices in the same way.

Construction

- Both play a role.

Asset Finance supports machinery, scaffolding, and vehicles. Invoice Finance bridges lengthy payment cycles with clients or main contractors common in the sector. Many firms use a blend.

Summary Table

Strategic Scenarios: When to Use Each

- Seasonal agency ramping up staff for a big project: Use invoice finance to pay wages early, bridge client terms, and retain funds for marketing without collateral.

- Manufacturer replacing €500k of plant: Asset Finance provides spread costs over 3–5 years and preserves credit lines.

- Rapidly growing service business with minimal assets: Invoice Finance scales automatically with sales, unlike most term loans.

Some businesses operate both: e.g. warehouse logistics firms may fund forklifts via Asset Finance while using Invoice Finance to bridge shipping payments from clients.

UK Market Scale & Evolution

Per UK Finance, combined Invoice Finance & Asset-based Lending (IF/ABL) facilities serviced around 35,000 UK businesses, advancing over £20 billion at any time and supporting £316 billion in client turnover in 2023 (LinkedIn, Clifton Private Finance, Porter Capital, UK Finance).

That breadth demonstrates how central IF/ABL remains to SME liquidity and working capital management across sectors.

Advantages & Limitations

Invoice Finance

Provides rapid cash injection and flexible scale; however the regular fees add up if invoices take long to clear. Factoring may expose customer relationships if they’re contacted directly.

Asset Finance

Delivers structured funding for capital assets and typically lower recurring cost for large facilities, but requires asset quality, stronger underwriting and operational oversight on collateral.

Choosing the Right Fit for Your Business

Both invoice finance and asset finance play crucial but different roles in helping UK SMEs stay liquid and grow. If you’re a recruitment or marketing agency facing long payment terms, invoice finance can free up working capital almost immediately. Manufacturers, logistics firms, and retailers, on the other hand, often benefit more from spreading the cost of vehicles, machinery, or refits through asset finance.

To understand what these options might look like in practice, you can try Funding Agent’s free tools: use the Invoice Finance Calculator to estimate how much of your debtor book could be released today, or test the Asset Finance Calculator to see the monthly cost of leasing or hire purchase.

Exploring both can help you decide which type of facility fits your business model best, or whether a blended approach makes sense. When you’re ready, Funding Agent can connect you with FCA-authorised lenders so you can compare offers side by side and move forward with confidence.

References

- UK Finance, Invoice Finance & Asset-based Lending Report 2023–25 (UK Finance)

- British Business Bank, UK Small Business Finance Markets Report 2025 (provides market scale for IF/ABL) (UK Finance)

- Porter Capital, Invoice Factoring vs Asset-based Lending (Porter Capital)

- 1st Commercial Credit, Cost Comparison of ABL vs Factoring (1stcommercialcredit.com)