Bank Loans vs Alternative Lenders

.png)

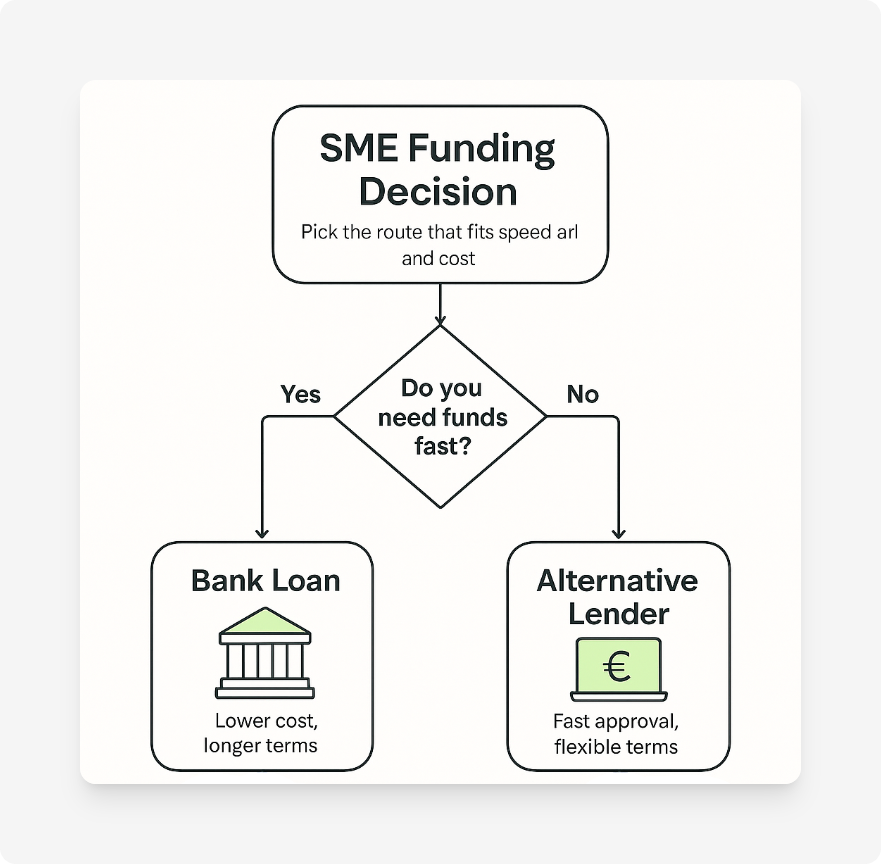

When UK businesses look for funding, the big question is whether to borrow from a traditional bank or an alternative lender. Banks are known for stability and lower costs, but their processes are slow and criteria are strict. Alternative lenders, on the other hand, are faster and more flexible, offering products like invoice finance, merchant cash advances, and short-term working capital loans. The right choice depends on how quickly you need funding, the strength of your accounts, and the type of finance you are seeking.

In short, banks remain the best option if your SME has strong accounts, security to offer, and you want a long-term, low-cost loan. Alternative lenders are often the smarter choice if you need cash quickly, prefer flexible repayment structures, or have struggled to meet strict bank criteria. Many UK SMEs use both, combining the stability of a bank loan with the speed and flexibility of alternative finance products.

For a full breakdown of options, the British Business Bank Finance Hub offers detailed guides on UK funding types.

Defining the Players: Banks vs Alternative Lenders

Traditional Banks

Banks have structured services and require strong credit and collateral. Approval can take weeks. Interest rates are usually lower because banks have access to cheaper money.

Alternative Lenders

These lenders operate online. They approve loans faster and have more flexible rules. They work with businesses that banks may turn away. Products include invoice finance, revenue-based lending, merchant cash advances, and short-term unsecured loans.

Key SME Data Points Dashboard

This dashboard brings together key data points on SME lending in the UK, highlighting how traditional banks and alternative lenders differ in strengths, how overall lending volumes have shifted in recent years, and which types of institutions currently dominate the market. Each chart focuses on one dimension, helping business owners and finance teams see the bigger picture at a glance.

What Lenders Evaluate: The 5 C’s of Credit

Both banks and alternative lenders use the Five C’s to judge your loan application:

- Capacity – Can you repay the loan?

- Capital – Do you have savings or equity to back it up?

- Character – What does your credit history say?

- Conditions – What is the loan for, and what is happening in the wider economy?

- Collateral – What assets can secure the loan?

For secured lending, SMEs should also understand how lenders record charges with Companies House.

Side-by-Side: Key Comparison

In short, banks provide lower-cost finance with longer terms, but are slower and harder to qualify for. Alternative lenders trade higher costs for speed, flexibility, and wider eligibility, making them attractive for SMEs that need fast or tailored funding solutions.

Factors to Consider When Choosing Between Banks and Alternative Lenders

1. Security and Collateral

Banks often want property, machinery, or a director’s personal guarantee before approving larger loans. Alternative lenders sometimes accept looser security or base lending on cash flow, invoices, or card receipts. See our guide on debentures and security to understand how lenders protect themselves.

2. Relationship Banking

Banks may offer additional perks, like overdrafts, cards, and foreign exchange services, if you already bank with them. Alternative lenders focus on a single product and won’t give you that all-in-one relationship. For specialist support, you may prefer tailored funding such as commercial mortgages.

3. Transparency of Fees

Banks are more regulated and typically disclose all charges clearly. Alternative lenders can be more expensive if you miss repayments, with some charging daily or weekly interest instead of monthly. Always compare products carefully, such as those in our guide on invoice finance.

4. Impact on Credit File

Bank loans almost always show on your company credit report and strengthen it if managed well. Alternative lenders vary: some report to credit agencies, others do not, so the impact can be less predictable. If you are considering secured lending, our article on debenture charges explains lender rights in detail.

5. Sector Fit

Banks tend to serve “safer” sectors with long trading histories. Alternative lenders often target niches: e-commerce, construction, or startups. Explore our lender comparison pieces like White Oak vs LendingCrowd to see which lenders work best for your industry.

6. Support and Guidance

Banks may assign a relationship manager who provides broader advice. Alternative lenders lean on digital platforms, so human interaction is limited, but onboarding is faster. To compare the hands-on approach of different funders, see our analysis of Funding Circle vs Iwoca.

7. Regulation and Protection

Banks are tightly regulated under PRA and FCA rules, with deposit protections. Alternative lenders are FCA-authorised but operate with different models; SMEs need to review contracts closely. For more detail on security structures, visit our guide on debentures.

Market Trends and Why Alternatives Matter

In mid-2025, over 60% of SME lending in the UK came from sources outside high street banks. This shift is tracked in the Bank of England Credit Conditions Survey and highlights the role of alternatives.

Community Development Financial Institutions (CDFIs) are helping businesses rejected by banks. They provide flexible local lending, often backed by government and major banks. See The Times coverage for more on their role.

Some SMEs are cautious about borrowing after seeing peers struggle with debt. Reports like the Nesta Alternative Finance Study explain how the market has grown while balancing risks.

Decision Checklist for SMEs

For more insights on SME lending, the Federation of Small Businesses (FSB) provides updated borrowing guidance.

Which Is Best For Your SME?

There is no single best choice. Banks are ideal for low-cost, long-term loans if you qualify. Alternative lenders give speed, easier access, and flexibility. Many SMEs now use both, taking bank loans for stability and turning to alternatives for agility.

To dive deeper, see our guides on invoice finance, debentures, and commercial mortgages to match funding to your strategy.

FAQs

Bank loans usually cost less but take longer to arrange and require strong credit and collateral. Alternative lenders are faster and more flexible, but often charge higher rates.

Yes, many alternative lenders are regulated by the Financial Conduct Authority (FCA). Always check that the provider is FCA-authorised and review their terms before signing.

Banks face tighter regulations and need to manage risk carefully. They usually lend to businesses with a proven track record, strong credit history, and assets to secure the loan.

Alternative lenders work best if you need funding quickly, have weaker credit, or want flexible products such as invoice finance or revenue-based lending.

It depends on the provider. Some report repayments to credit agencies, which can help build your score. Others do not, so the effect may be limited.

Banks typically offer secured business loans, overdrafts, and commercial mortgages. Alternatives provide faster options like unsecured loans, merchant cash advances, and invoice financing.