Best Lenders for Consultancy Firms in the UK

.png)

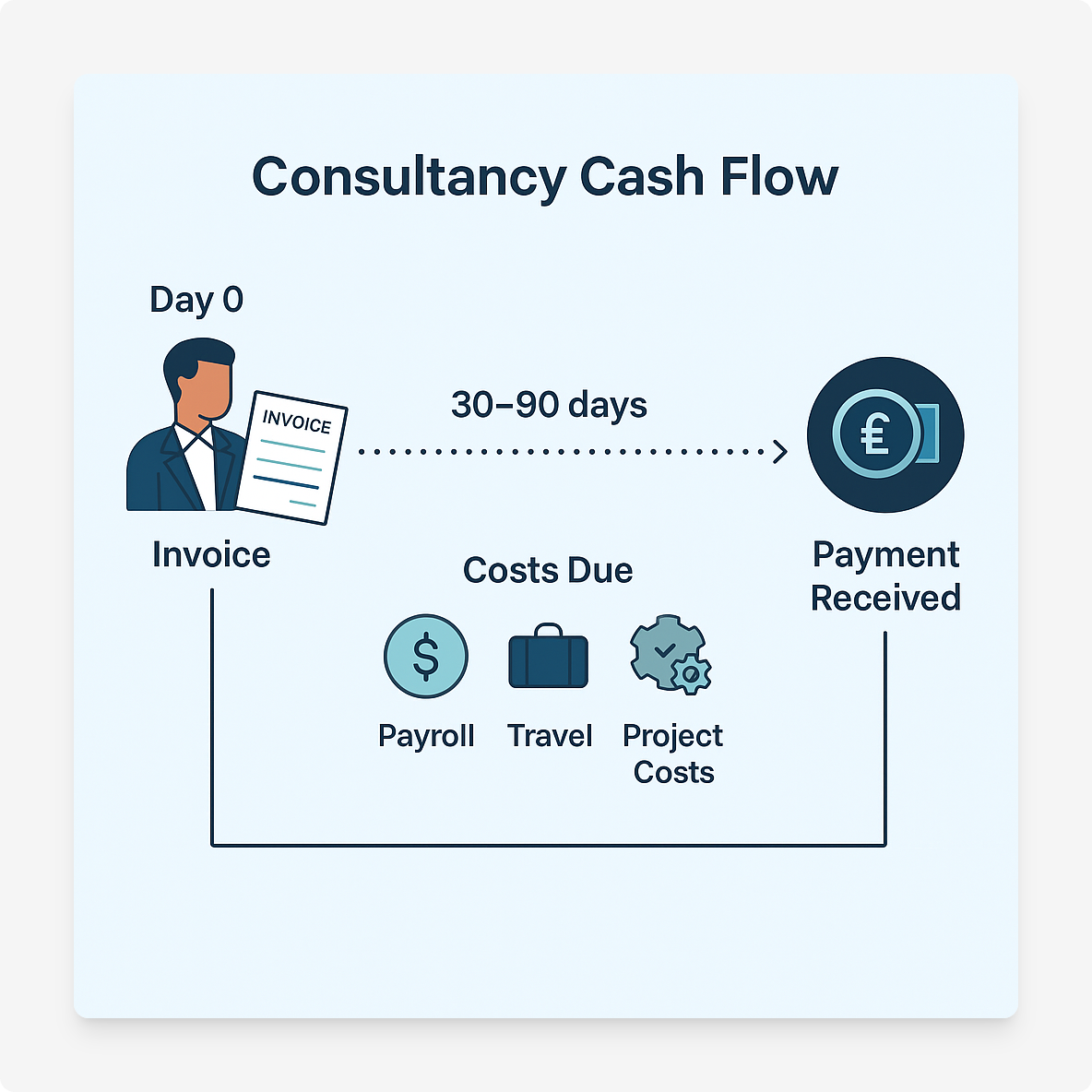

Consultancies run on people, projects, and trust. Cash flow gaps from 30–90 day client terms can strain operations, financing helps firms keep teams funded, deliver work on time, and scale confidently.

Best Lenders for Consultancy Firms in the UK

These lenders are known for products that fit consulting cash cycles, fast access, flexible terms, and strong invoice or revolving solutions. Always compare fees, covenants, and eligibility to find the right fit for your firm.

1. Iwoca

Iwoca stands out for its speed and flexibility. With approvals often in minutes, it is ideal for consultancies that need quick working capital to bridge invoice lags on retainers or sprints. Flexible repayment structures make it suitable for firms with uneven monthly revenue flows.

2. Fleximize

Fleximize offers unsecured loans up to £500,000 with terms as long as 60 months. This makes it a good option for consultancies investing in team growth, professional certifications, or technology upgrades. The blend of growth and working capital finance positions Fleximize as a versatile partner.

3. Time Finance

Time Finance provides both invoice and asset finance, advancing up to around 90% of invoice value in as little as 24 hours. With additional offerings like IT and office equipment leasing, it suits people-heavy consultancies scaling delivery capacity and taking on larger contracts.

4. Bibby Financial Services

Bibby Financial Services is one of the UK’s largest independent invoice financiers. It is a strong match for B2B consultancies working with clients on 30–90 day terms, especially those with recurring project invoices. Their experience in the professional services sector makes them a reliable partner.

5. Aldermore

Aldermore offers invoice discounting facilities that allow consultancies to retain client control while improving liquidity. This product fits established firms with predictable receivables, enabling them to boost cash flow without handing over client management to a third party.

6. Close Brothers Invoice Finance

Close Brothers Invoice Finance specialises in mid-market invoice finance, offering robust discounting and factoring solutions. It is particularly suited to larger consultancy engagements where revenue comes from multiple clients, providing stability and diversification against delayed payments.

7. Lloyds Bank

Lloyds Bank has dedicated professional practice and term funding products designed for service firms. From practice loans to overdrafts, these solutions support senior hires, partner funding, and office moves, key moments in a consultancy’s growth cycle.

8. Barclays

Barclays offers larger overdraft limits and straightforward unsecured loans, making it a practical choice for consultancies that need reliable working capital. It works well for bridging short billing gaps and funding client campaign bursts without locking into long-term debt.

9. HSBC UK

HSBC UK is a strong choice for consultancies serving international clients. Their combined offering of trade finance and working capital solutions helps firms manage overseas projects, multi-currency operations, and cross-border receivables with confidence.

10. Starling Bank

Starling Bank provides app-first overdraft facilities of up to £50,000. This digital-first approach appeals to boutique consultancies managing uneven retainers or ad hoc project costs, offering convenience and speed directly from their business banking app.

Why consultancy firms need finance

Consultancies look asset-light, yet they face real cash pressures. Income is lumpy, project costs arrive before client payments, and payroll must land every month. The right finance smooths cash flow, protects delivery quality, and funds growth without disrupting day to day operations.

The UK’s consulting market is expanding rapidly, reaching £20.4bn in 2023, but cash flow pressures persist. Across UK businesses, days sales outstanding (DSO) has risen by 6.6% over five years, meaning firms wait longer to be paid. Late payments restrict growth, 18% of SME consultancies couldn’t invest because invoices remained unpaid. Meanwhile, corporate stress is evident: the UK recorded over 25,000 insolvencies in 2023. Regionally, a funding imbalance persists, half of SMEs are outside London/South East, but they received just 15% of PE/VC deals.

1. Cash Flow Gaps from Client Payment Terms

Many clients pay on 30 to 90 day terms. Meanwhile the firm must cover salaries, contractor invoices, software seats, and travel. Facilities such as invoice finance and revolving credit bridge the timing gap between delivery and cash received, so partners can focus on utilisation and client work instead of chasing payments.

2. Payroll and Talent Costs

People are the product. Hiring senior consultants, data specialists, or niche contractors increases upfront costs before revenue from new projects ramps. Working capital facilities ensure payroll is protected during ramp up and onboarding periods.

3. Upfront Project Delivery Costs

Large programmes often require travel, research, subcontractors, data licences, and specialist tools. Drawdown finance spreads these costs across the life of the engagement, so the firm can take on bigger, higher margin work without straining cash reserves.

4. Seasonality and Market Cycles

Utilisation typically dips around holiday periods and year end. A flexible facility helps cover fixed costs in quieter months and prevents short term slowdowns from turning into operational stress.

5. Client Concentration Risk

Boutique firms often rely on a handful of key accounts. A delayed milestone or procurement hold can disrupt receipts. Access to a standby line reduces the shock and protects delivery teams from stop start decisions.

6. Growth, Marketing, and New Offerings

Entering new sectors, launching a data product, or opening a regional office requires cash before returns arrive. Term loans or larger revolving lines fund hiring, marketing, and business development while the pipeline matures.

7. Partner Buy ins, Mergers, and Acquisitions

Partnership models require capital for buy ins and equity rebalancing. Acquiring a niche boutique or a specialist capability can be transformative. Structured finance supports these events without draining operating cash.

8. Technology and Infrastructure

Modern delivery depends on CRM, project management, analytics, and AI tooling. Financing smooths the move to new platforms and spreads costs for multi year licences and data subscriptions.

Common Symptoms That Signal a Finance Need

- Debtor days rising while utilisation is steady

- Recurring use of director loans to cover payroll

- Strong pipeline but slow conversion due to onboarding costs

- High dependence on two or three enterprise clients

Quick View: What Finance Solves for Consultancies

For clear definitions of the tools mentioned above, see the Finance Dictionary. If you want help matching a facility to your firm’s stage and client profile, Funding Agent can assess options and lender fit.

What Finance Types Consultancies Use and Why

Consultancies do not need machinery or stock, but they do need reliable working capital. The finance types they use reflect their reliance on people, project delivery, and client contracts. Here are the main categories and why they matter.

1. Working Capital Facilities

These are the most common. Consulting firms face lumpy income and long client payment terms. Facilities like invoice finance, overdrafts, and revolving credit loans bridge the gap between delivery and cash collection. They keep payroll, subcontractors, and travel costs funded without disruption.

2. Term Loans

For growth projects such as opening new offices, launching new service lines, or hiring senior staff, term loans provide a lump sum repaid over 1 to 5 years. This allows firms to spread the cost of expansion over time while revenues catch up.

3. Invoice Finance and Factoring

Since invoices are often the main asset, unlocking them through factoring or discounting is an efficient way to generate cash. It suits consultancies with large enterprise clients on extended payment terms, turning receivables into working capital quickly.

4. Merchant Cash Advances

Although less common, some marketing or creative consultancies use merchant cash advances where repayments flex with revenue. This is attractive for firms with volatile monthly income or project-based billing models.

5. Asset Finance

Used less often, but applicable when consultancies invest in IT infrastructure, software licences, or vehicles. Spreading payments through asset finance preserves cash while securing needed tools.

6. Equity and Partner Capital

Many partnerships raise capital internally. New partners buy equity to fund growth, while external equity or angel investment may be considered for consultancies developing proprietary IP, platforms, or software tools that scale beyond billable hours.

7. Government and Backed Schemes

Government-backed loans and guarantees, such as those offered through the Recovery Loan Scheme, give consultancies additional routes to funding, often with lower rates or improved eligibility.

Quick Comparison: Finance Types

Each consultancy will blend these options depending on size, client base, and growth stage. To learn more about which facility matches your firm, see the Finance Dictionary or explore our guidance on Funding Agent.

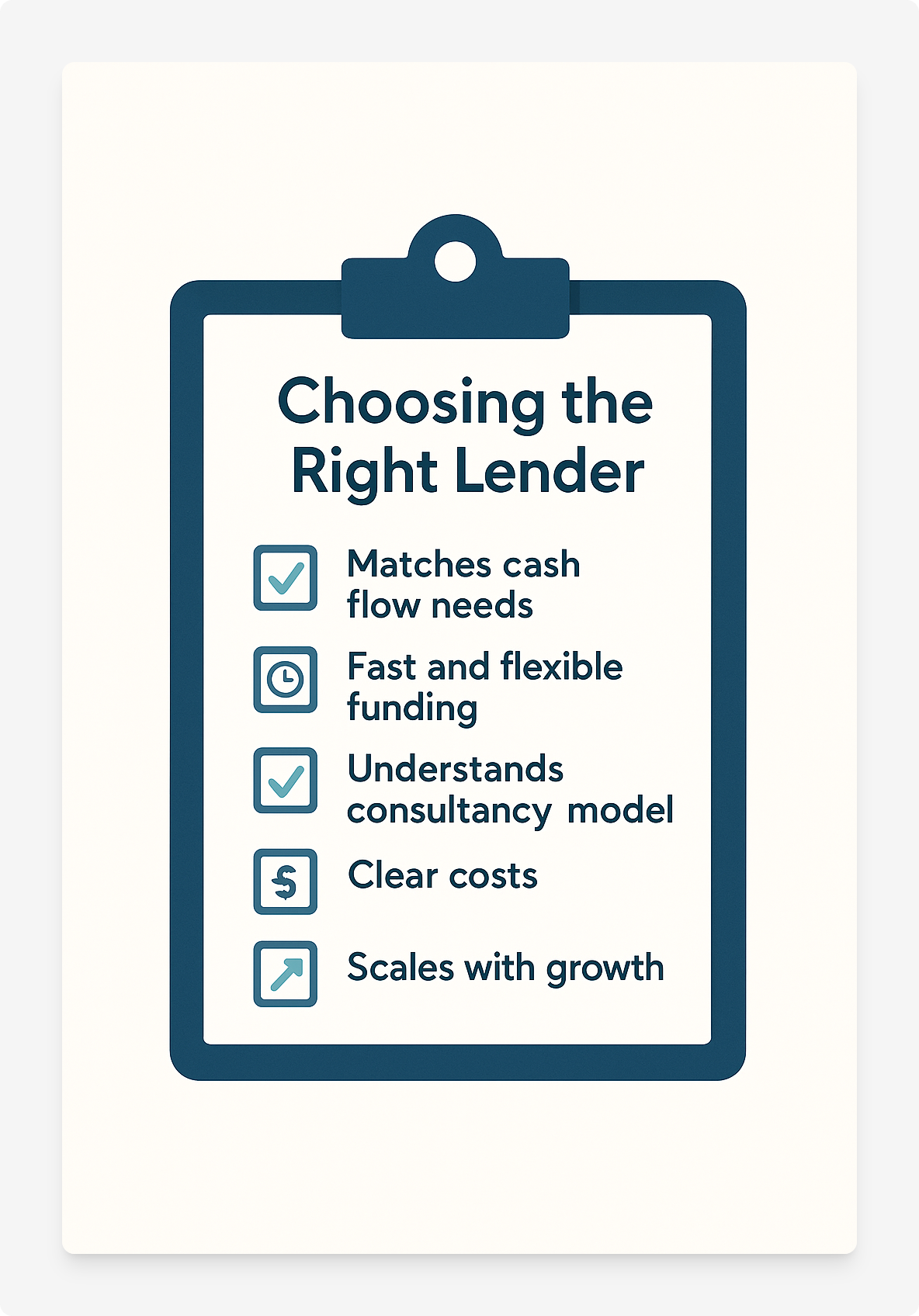

How Consultancies Can Choose the Right Lender

With so many finance options available, the challenge for consultancy firms is not only accessing funding but selecting the right lender. The wrong choice can result in costly fees, inflexible terms, or facilities that do not match the rhythm of client billing. Here are the main factors to consider when making the decision.

1. Match Facility to Cash Flow Profile

Consultancies with long debtor days need lenders who understand invoice finance and revolving credit. Firms expanding into new regions or service lines may prefer structured term loans. The first filter is aligning the lender’s product strengths with the firm’s cash flow reality.

2. Speed and Flexibility of Funding

Fast decisions matter when project kick offs require immediate outlay. Lenders like fintech platforms specialise in approvals within 24–48 hours, while high street banks often take longer. Firms should weigh speed against the stability and relationship benefits of traditional banks.

3. Sector Understanding

A lender that understands professional services will appreciate the reliance on people, utilisation rates, and client contracts. This sector fit can mean more tailored covenants and realistic repayment schedules, reducing strain on operations.

4. Cost of Finance

Interest rates, arrangement fees, and hidden charges vary widely. Comparing total cost of borrowing is crucial, not just headline rates. Platforms like Funding Agent help consultancies compare multiple lenders transparently.

5. Relationship and Support

Larger consultancies often value relationship banking with access to credit committees and advisory services. Smaller firms may prioritise streamlined digital platforms. Assess whether your firm benefits more from personal account management or online speed and simplicity.

6. Scalability of the Facility

As firms grow, so do financing needs. A revolving credit line that scales with turnover or an invoice finance agreement that grows with client volume is often better than fixed facilities that require constant renegotiation.

7. Reputation and Reliability

Lender reputation should not be overlooked. Researching reviews, default handling, and client satisfaction helps ensure your firm partners with a reliable funder, particularly when dependability during downturns matters most.

Quick Checklist for Choosing a Lender

- Does the lender offer the type of finance you actually need?

- Can they move at the speed your projects demand?

- Do they understand consultancy business models?

- Is the total cost of borrowing clear and competitive?

- Will the facility grow with your firm?

The right lender is not always the cheapest, but the one whose facility aligns with your operating model and growth plans. For support in comparing the best lenders and matching products to your consultancy’s needs, explore Funding Agent.

Conclusion: Finding the Best Finance for Your Consultancy

Consultancy firms may be built on expertise rather than physical assets, but their financial needs are every bit as real. Cash flow gaps, payroll obligations, and upfront project costs make external funding a vital tool for stability and growth. The UK lending market offers a wide range of options, from fintechs delivering quick decisions to high street banks providing long-term stability.

In this guide we have highlighted the top 10 lenders for consultancy firms in the UK, explained why consultancies need finance, outlined the types of finance they use, and offered a framework for choosing the right lender. The common thread is clear: the best facility is the one that matches your client contracts, cash flow cycles, and strategic ambitions.

If your consultancy is weighing up funding options, don’t navigate the market alone. Funding Agent provides clear, independent insights and access to lenders who understand professional services. Whether you need short-term cash flow support, growth finance, or structured partner funding, we can help you identify and secure the right solution.

Explore our Finance Dictionary for definitions of key funding terms, or get in touch to discuss your firm’s specific needs. With the right finance partner, your consultancy can focus on what it does best, delivering value to clients and scaling with confidence.