How to Qualify for a Working Capital Loan in the UK

.png)

Need to pay staff on time, buy stock before customer payments arrive, or cover a temporary cash gap? A working capital loan can solve these timing issues fast, but only if you know what lenders actually want to see.

This guide breaks down exactly what you need to qualify, how to prepare a strong application, and what to do if you don't fit the standard criteria.

What Lenders Actually Look For

Think of these as four gates. Pass them, and the rest becomes much easier:

Time trading: Most lenders want 6–12 months of trading history as a minimum. If you're looking for larger amounts, 24 months makes you significantly more attractive.

Turnover: Expect to show £50,000–£100,000 in annual revenue, backed up by bank statements, not just projections.

Credit health: Clean personal credit and manageable existing debt make you a safer bet. You don't need perfect credit, but recent issues will raise questions.

Clear purpose: Lenders prefer short-term, practical uses like stock purchases, payroll gaps, VAT bills, or covering slow-paying customers. Why? Because the money cycles back quickly.

If you're weighing up whether this is the right type of funding for your situation, it's worth understanding the difference between working capital loans and term loans, they're designed for very different business needs.

Build a Complete Application Pack

Lenders get nervous when information trickles in. Send everything upfront and you'll look organize, and get a faster decision.

Essential documents:

- 3–6 months of business bank statements

- Latest accounts or management accounts

- Recent tax return (if requested)

- ID and proof of address for directors/owners

- One-paragraph explanation: "We need £25,000 to purchase stock for Q2. Our regular customer payments will cover repayments starting in 60 days."

Rather than approaching lenders individually, you can save time by working with Funding Agent, we'll match your application with lenders who already specialize in your sector and business size.

Common Approval Blockers (And How to Handle Them)

It's better to address these upfront than let lenders discover them later:

Constantly overdrawn accounts: If your balance has been low or negative for three months straight, include a note explaining seasonality or upcoming invoice payments.

Very new businesses: Under 6 months of trading? You'll need more flexible products. Invoice finance, merchant cash advance, and revolving credit lines often work better for businesses still building their track record, you can explore all your financing options here.

Recent CCJs or missed payments: Many lenders will still consider you, but expect a smaller loan amount or a personal guarantee requirement.

Wrong loan purpose: Working capital isn't for property purchases or long-term fit-outs. If your project takes years to repay, you need a different product.

The 2025 Lending Reality

UK lenders know that many small businesses are using short-term cash flow finance in 2025. That's why they're scrutinizing bank statements more carefully and looking for evidence of repeat income, not one-off sales.

The lending landscape has changed significantly in the past year. If you want to see which providers are currently most responsive to small business applications, we've put together a comparison of the best working capital finance lenders for small businesses operating in the UK market.

Calculate Your Actual Loan Amount

Don't guess. Use this simple method:

- List all income expected over the next 30–60 days (cash + invoices)

- List all outgoings for the same period (payroll, rent, VAT, suppliers)

- Subtract outgoings from income

- The gap, plus a small buffer, is your sensible loan request

This calculation helps you avoid borrowing too much (and paying unnecessary interest) or too little (and running short again in a few weeks).

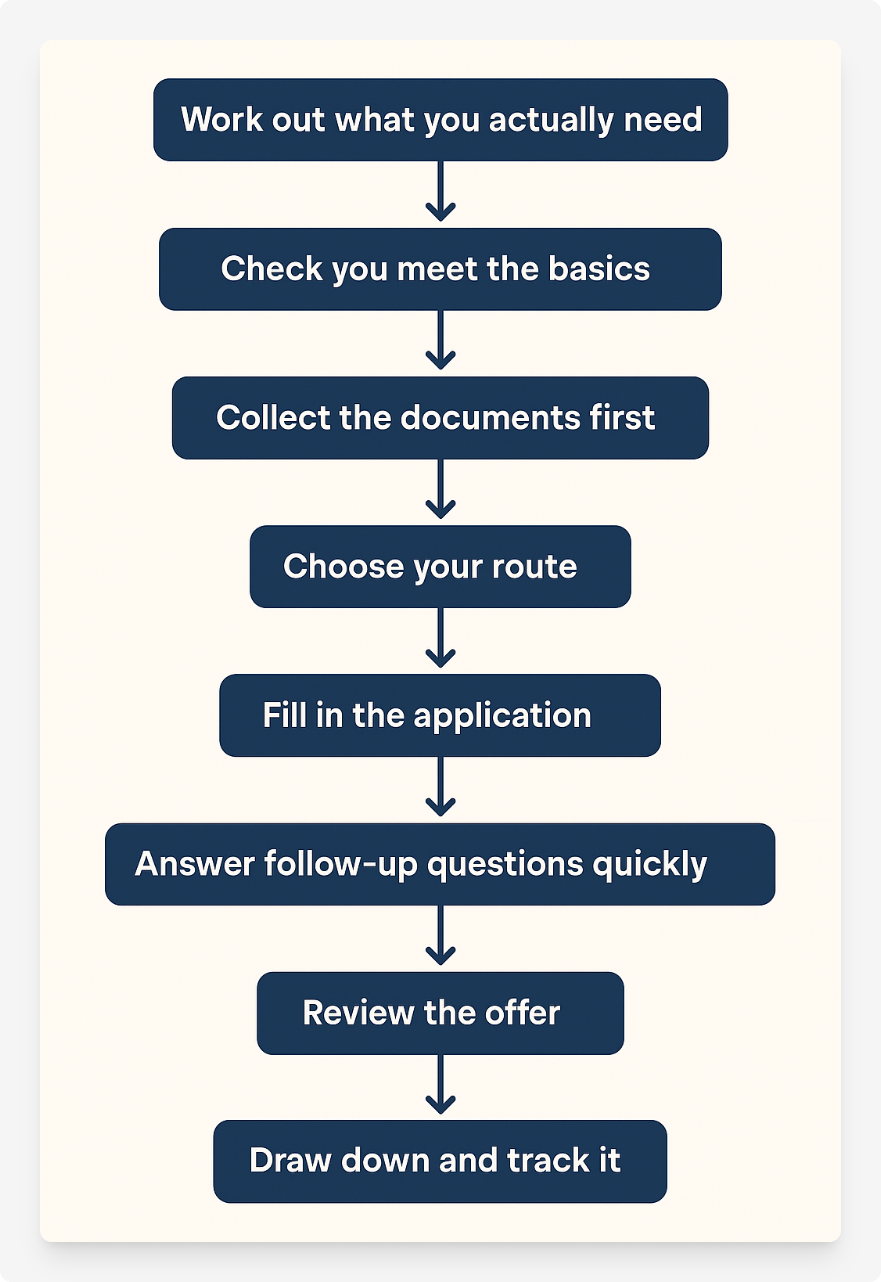

Step-by-Step: How to Apply for a Working Capital Loan

1. Work out what you actually need

List what's coming in over the next 30–60 days, then list what's going out. If outgoings exceed income, that gap is what you need to cover. Add a small buffer, that's your loan amount.

2. Check you meet the basics

Ask yourself: Have I traded at least 6–12 months? Is my annual turnover around £50,000 or more? Is my personal credit mostly clean? Is my loan purpose short-term (VAT, stock, or payroll)?

If you answer yes to most of these, continue to the next step.

3. Collect your documents first

Gather 3–6 months of business bank statements, your latest accounts or management accounts, ID and proof of address, and a short note explaining what the money is for. Having everything ready speeds up the process significantly.

4. Choose your application route

You can apply directly to a lender if you already have a relationship with them, or you can work with a broker who'll submit your application to multiple lenders at once. If you're exploring working capital finance for small businesses, you'll see the different structures available and can decide which approach suits your business model.

For broker applications, submit your details through Funding Agent and they'll handle the placement.

5. Fill in the application

Enter your business details, loan amount, intended use, and attach bank statements. Keep your purpose statement short and specific: "We need £20,000 to purchase stock for confirmed orders arriving in May."

6. Answer follow-up questions quickly

Lenders often request additional information, a clearer bank statement, proof of address, or explanation for a low-revenue month. Reply immediately to stay at the top of their queue.

7. Review the offer carefully

When your offer arrives, check: loan amount, total cost, repayment term, and whether a personal guarantee is required. If it fits your cash flow, accept it.

8. Draw down and track repayments

Once funds arrive, use them only for your stated purpose. Make repayments on time for several months. This builds trust, making it easier to access additional funding later if needed.

What If You Don't Qualify?

Not meeting the standard criteria doesn't mean you're out of options. Some businesses are better suited to:

Invoice finance: If you have outstanding invoices from creditworthy customers, you can borrow against them instead of waiting for payment.

Merchant cash advance: Businesses with consistent card payment revenue can access cash based on their future sales.

Revolving credit lines: These give you flexible access to funds without reapplying each time you need cash.

These products rely more on sales and invoices than trading history, which makes them more accessible for newer businesses or those with thinner credit files. You can browse all available financing options to find what fits your payment structure.

FAQs

Most lenders prefer 12 months minimum. Some will consider 6 months if your application is otherwise strong. Under 6 months? Submit through Funding Agent to reach lenders that work with earlier-stage businesses.

Yes, but expect smaller loan amounts, shorter terms, or personal guarantee requirements. Strong, regular cash flow significantly improves your chances.

Because working capital loans solve timing issues. Lenders need proof that money is coming in regularly, not just once per quarter, to feel confident you can make repayments.

Identify and fix the issue: missing documents, small defaults, or unclear loan purpose. Then resubmit, ideally through a broker who knows which lenders are more flexible with specific situations.