Funding Circle’s Deal With Waterfall and What It Could Mean for UK SMEs

.png)

Funding Circle has announced a new funding deal worth £700m with Waterfall Asset Management. The deal is backed by senior financing from Citi. Waterfall will also buy around £120m of existing Funding Circle loans.

Funding Circle says the goal is simple, increase the funding available for its shorter-term loan product and keep lending capacity more consistent over the next two years. That matters if you rely on fast funding for stock, payroll, VAT, or working capital.

This guide explains what the deal is, what it is not, and what to look at when you compare business finance options.

Quick summary

- Waterfall is providing a £700m forward flow commitment over two years, with senior financing from Citi.

- Waterfall is also buying an existing loan portfolio worth about £120m.

- This is private funding, not a government scheme and not a blanket rate cut for borrowers.

- For SMEs, the main impact is usually lending capacity and product consistency, not cheaper pricing overnight.

- When comparing offers, focus on purpose, total cost, and monthly cash flow across options like unsecured business loans and revolving credit loans.

What the Funding Circle and Waterfall deal actually is

Think of a forward flow deal as a standing agreement. An institutional investor agrees to fund or buy eligible loans as they are created, based on rules set in advance. Those rules can include loan size, term length, and borrower criteria.

For the lender, that creates a more predictable pipeline of capital. It can help the lender keep offering loans without relying only on its own balance sheet. For the investor, it creates a steady stream of loans that match the investor’s risk and return targets.

In this announcement, Funding Circle says Waterfall will support its shorter-term loan product over the next two years. Waterfall will also buy a block of existing loans, which adds immediate funding capacity. You can read the original announcement in the Funding Circle press release.

What’s in the announcement?

The £700m forward flow commitment

The headline number is £700m. That is the size of the commitment over two years. It does not mean £700m lands in the market on day one. It means Funding Circle can originate loans that meet the agreed rules, then those loans can be funded or purchased through the forward flow over time.

The c.£120m existing loan portfolio purchase

Waterfall is also buying around £120m of loans that already exist. That can free up capacity for Funding Circle to keep lending. It can also reduce the amount of capital tied up in older loans.

Why Citi is mentioned

Funding Circle says the forward flow includes senior financing from Citi. In simple terms, this helps fund the structure in a lower-risk layer. The investor and lender can then use that structure to support more lending activity, within agreed limits.

Why the long relationship matters

Funding Circle says it has worked with Waterfall since 2018 and that the partnership has passed £3bn of total lending through the platform. A multi-year track record can signal that the parties are comfortable with the underwriting approach and the performance data.

Why this matters for UK SME finance in 2026

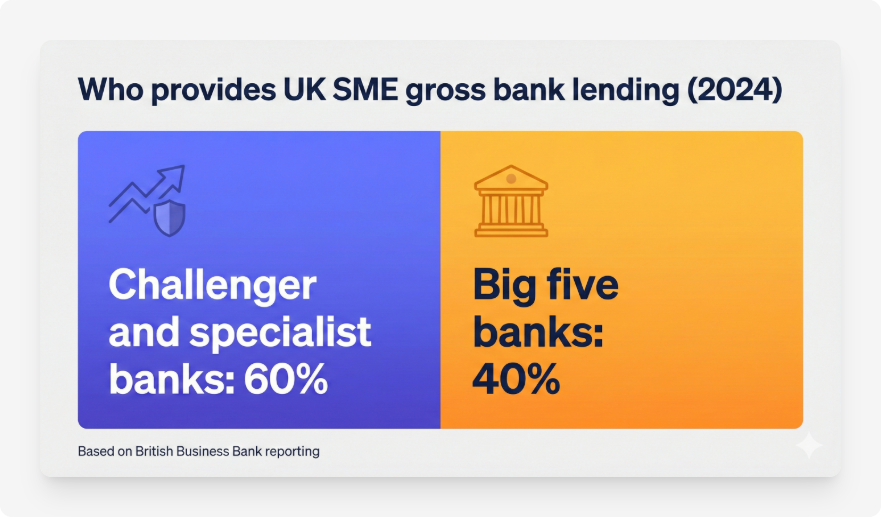

UK SME finance has changed a lot in the last decade. Big banks still matter, but challenger and specialist banks have taken a larger share of lending. The UK government has said that challenger banks account for 60% of annual gross bank lending to SMEs as of 2024. If you want the wider context, see the UK government summary on small business access to finance.

The British Business Bank reports a mixed picture. Fewer smaller businesses used external finance during 2024, but the total value of lending held up. In its reporting on 2024 gross lending, challenger and specialist banks provided about 60% of gross lending to smaller businesses. You can cross-check the figures in the British Business Bank release and the Small Business Finance Markets Report 2025.

In that context, large institutional commitments can be a sign of confidence in the lender’s model and data. They can also support steadier lending capacity, even when the wider market feels uncertain. If you are weighing bank lending against specialist lenders, this guide may help: bank loans vs alternative lenders.

What this means for your borrowing decisions in 2026

1) More funding does not automatically mean lower rates

A larger funding line can improve capacity, but it does not guarantee cheaper loans for every borrower. Pricing still depends on your risk profile. Lenders look at trading history, affordability, sector risk, time in business, and the loan term.

The best way to judge cost is to compare total repayable amount and the monthly impact on cash flow. A quick way to model repayments is a business loan calculator, or a more specific unsecured business loan calculator. If a quote looks attractive, check fees, early settlement terms, and whether repayments are fixed or flexible.

2) Consistent capital can mean more predictable lending

If a lender has a reliable funding pipeline, it may be less likely to pause lending due to internal limits. That can make outcomes feel more consistent over time, as long as you meet the eligibility rules.

This matters most for businesses that borrow in cycles, for example seasonal stock buys, short working capital gaps, or bridging VAT. If you want to improve your odds before you apply, start here: how to qualify for a business loan in the UK.

3) Compare structure, not just the headline price

Start with the job the money needs to do. A short-term need often fits a different product than a long-term investment. If you need flexible access, a revolving facility may fit better than a fixed-term loan. You can model the monthly impact with tools like the revolving credit facility calculator.

It also helps to understand loan types. For example: secured vs unsecured business loans, and what a revolving credit loan is.

If you want a side-by-side view of lenders and structures, these guides can help: Funding Circle vs Iwoca and Kriya vs Funding Circle.

Alternatives you might consider

Not every funding need fits a short-term loan. The best match depends on what drives your cash gap. If you want a simple decision path, start here: which financing is best for short-term business needs.

- If your issue is slow-paying customers, consider invoice financing. You can also read a plain-English explainer on what invoice finance is.

- If you are buying equipment or vehicles, look at asset finance. Here’s a quick guide on what asset finance is.

- If you need ongoing access to funds, explore revolving credit loans. You may only pay interest on what you draw, depending on the product.

- If you want a lump sum with fixed repayments, review unsecured business loans. These can work well for one-off projects with clear ROI.

A big funding announcement is worth noting. But what changes your business month to month is the product structure you choose and how well it fits your cash flow.

Final thoughts

Funding Circle’s £700m Waterfall deal is mainly a capacity story. It suggests continued institutional appetite for UK SME credit, and it may help keep shorter-term lending products available at scale.

For your business, the smart move stays the same. Start with the purpose of the funding, then compare structure and total cost, then stress-test the monthly cash flow. If you do that, headlines matter less and outcomes improve.

Sources

- Funding Circle press release, Funding Circle strengthens partnership with Waterfall Asset Management through new £700m deal (Feb 2026)

- British Business Bank, Small Business Finance Markets Report 2025 (report page)

- British Business Bank, challenger and specialist bank lending hits record share (Mar 2025)

- UK Government, small business access to finance (as of 2024)

- ICAEW, The Business Finance Guide (overview)