Growth Guarantee Scheme (GGS)

.png)

If you have Googled “government growth scheme”, you are usually looking for the UK’s Growth Guarantee Scheme (GGS), a government-backed programme that helps eligible UK smaller businesses access lending through accredited lenders. It is run by the British Business Bank on behalf of government.

This page is a practical explainer, it covers the key rules, the common misunderstandings (especially about the 70% guarantee), what lenders look for, and how to apply without wasting weeks on the wrong route.

Quick summary (most people just want these answers)

- What it is: A government-backed guarantee to lenders, designed to improve access to finance for UK smaller businesses looking to invest and grow.

- Guarantee level: Government guarantees 70% of the outstanding balance to the lender (after the lender completes its normal recovery process). You still owe 100% of the debt.

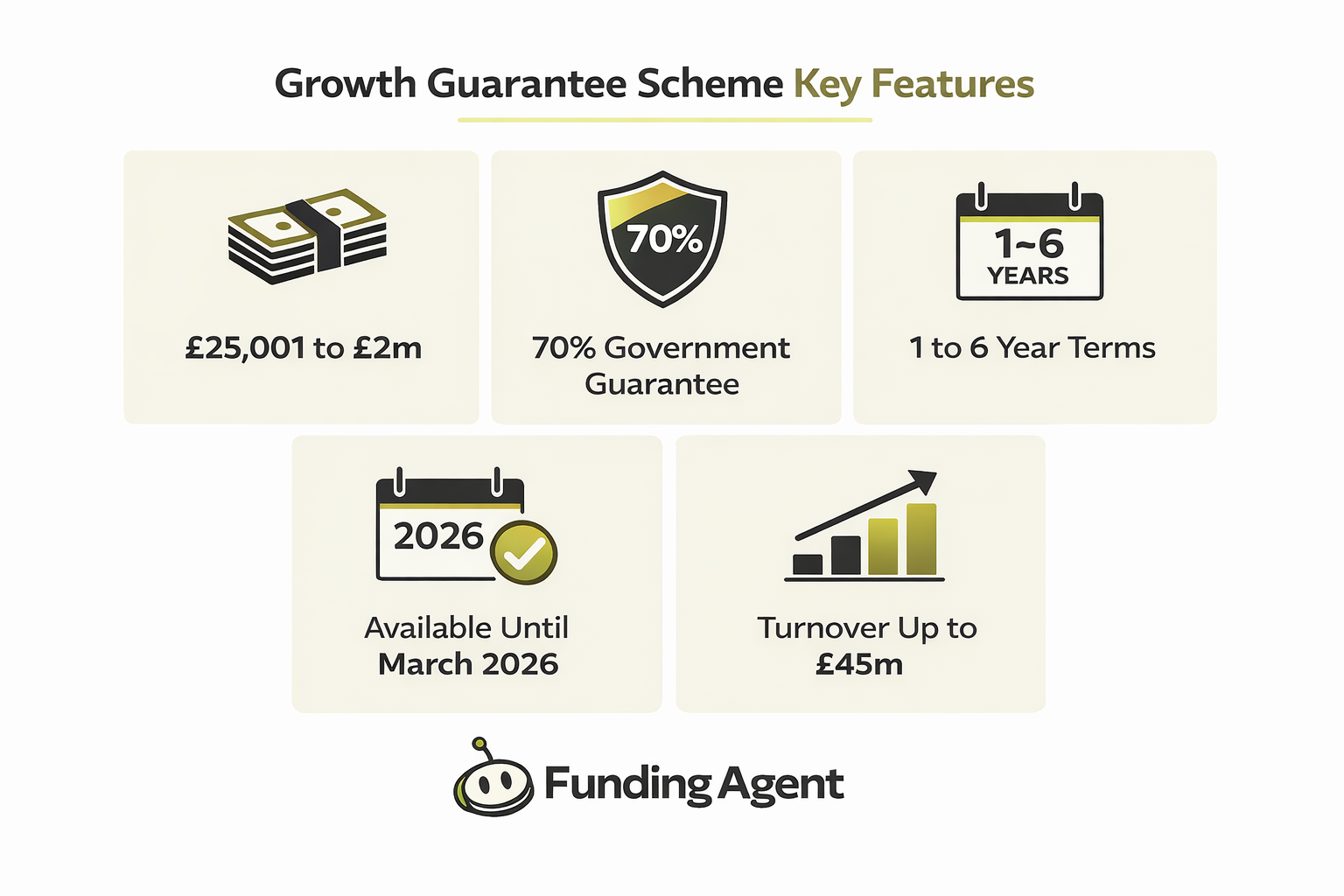

- Facility size: Up to £2m per business group in most cases (with separate rules for some Northern Ireland Protocol scope borrowers, commonly up to £1m).

- Turnover cap: Generally up to £45m annual turnover (group basis where relevant).

- Finance types covered: Term loans, overdrafts, asset finance, invoice finance, and asset-based lending (availability varies by lender).

- Terms: Term loans and asset finance can run from 3 months up to 6 years, overdrafts and invoice finance can run from 3 months up to 3 years.

- Security: A principal private residence cannot be taken as security within the scheme, personal guarantees may still be required.

Important timeline note: You may still see older sources saying the scheme runs until 31 March 2026. That was the extension announced in the 2024 Spring Budget, and it is widely referenced. ICAEW Later, the British Business Bank’s published performance data notes the scheme was extended to 31 March 2030 in the 2025 Spending Review. British Business Bank If you are writing a deadline into plans or forecasts, use the latest British Business Bank update.

Key scheme features (copy and paste friendly)

- Term loans and overdrafts: minimum facility size commonly starts at £25,001.

- Asset finance and invoice finance: minimum facility size can start at £1,000 (varies by product and lender).

- Maximum facility size: generally up to £2,000,000 per business group (with special rules for some NI Protocol scope borrowers).

- Guarantee: 70% to the lender, borrower remains 100% liable.

- Turnover: up to £45m (group basis where relevant). British Business Bank

How the 70% guarantee works (the bit most SMEs get wrong)

The Growth Guarantee Scheme is often explained badly online, which leads to two common myths: some people think the government is paying 70% of their loan, others think it means approval is guaranteed. Neither is true.

The simple way to think about it is: it is a risk-sharing mechanism for the lender. The lender still decides, sets the pricing, and collects the repayments. If things go wrong, the lender can claim under the government guarantee, but only after it follows its normal recovery process. British Business Bank

What the flow looks like in plain English

- Step 1: The SME applies to an accredited lender (directly, or via a broker).

- Step 2: The lender does normal underwriting, credit checks, affordability checks, and fraud checks, then decides whether to approve.

- Step 3: If approved under the scheme, the government provides the lender with a 70% guarantee against the outstanding balance (after recovery actions).

- Step 4: The business repays the facility in full under the agreed terms, and remains 100% liable for the debt.

If you only remember one line, make it this: The guarantee protects the lender, not the borrower. British Business Bank

What can you use Growth Guarantee Scheme finance for?

The scheme is broad on purpose: finance can be used for any legitimate business purpose, including investment and managing cash flow or working capital needs. The key constraint is affordability, you must be able to service the debt.

Examples that tend to fit well

- Working capital: smoothing payroll, VAT, stock buys, and supplier payments during slow customer payment cycles.

- Growth investment: marketing spend, hiring, opening a new site, expanding into export markets (as long as the deal is affordable).

- Equipment or vehicles: using asset finance when the purchase is tied to productivity or revenue generation.

- Cash flow backed by invoices: invoice finance where you need to unlock cash tied up in receivables.

If your reason is “I just need breathing room”, that can still be valid, but you should be prepared to show a clear plan for repayment and stabilisation. In practice, the lender will want to see how the facility improves cash flow, not just how it plugs a hole.

What types of finance can be covered under the scheme?

The scheme supports multiple products, but not every lender offers every product under GGS. If you are comparing options, it helps to decide which product type matches your use case first.

Term loans

Term loans are a lump sum repaid over a fixed schedule. Under the scheme, terms can run from 3 months up to 6 years (depending on lender and structure). If you want a simple overview of loan structures first, start here: Business Loans UK.

Overdrafts

Overdrafts can be useful for seasonal businesses, but are typically shorter term than term loans under GGS, commonly up to 3 years. If you are looking for flexible short term cash support, you may also compare with: Unsecured Working Capital Loans.

Asset finance

Asset finance is typically used when you are buying vehicles, machinery, equipment, or other assets, and want repayments aligned to the asset’s working life. You can read the basics here: Asset Finance, then model affordability with: Asset Finance Calculator.

Invoice finance

Invoice finance is usually the cleanest option when your problem is slow customer payments, not a lack of demand. Start with: Invoice Financing, and if you want quick numbers: Invoice Finance Calculator. Scheme-supported invoice finance and asset-based lending can commonly run from 3 months up to 3 years.

Unsecured business loans and other routes

Not every situation needs a government-backed scheme. If your business is strong, you may qualify for commercial options on equal or better terms. This is explicitly how the scheme is intended to work, if a lender can offer a commercial loan on better terms, they should. For a baseline comparison, see: Unsecured Business Loans.

Is the Growth Guarantee Scheme Still Available in 2026

Yes, originally launched on 1 July 2024 to succeed the Recovery Loan Scheme with an initial end date of March 2026, it was extended to extended to 31 March 2030 to provide four additional years of support for smaller businesses

The scheme is scheduled to run until 31 March 2026, subject to review or extension.

Availability may depend on:

- Lender allocation

- Government policy changes

- Economic conditions

Businesses considering funding should not delay purely because the scheme is available. Credit conditions can tighten quickly.

Growth Guarantee Scheme eligibility (simple checklist)

Lenders will still assess you like a normal credit application, but the scheme has a few specific eligibility rules. The British Business Bank lists the core criteria, and lenders may add their own commercial requirements on top.

Core scheme criteria

- Turnover: Up to £45m annual turnover (group basis where relevant). British Business Bank

- UK trading activity: You must be trading in the UK, and for most businesses generate more than 50% of income from trading activity.

- Viability: The lender must consider the business proposition viable.

- Not in difficulty: The borrower must not be in relevant insolvency proceedings and must not be considered a “business in difficulty”.

- Subsidy limits: You must confirm you will not exceed subsidy limits (previous government support may reduce what you can borrow).

What lenders usually want to see

This is not “official scheme wording”, it is how underwriting tends to work in the real world. If you show these clearly, you usually improve outcomes:

- Affordability: A sensible repayment plan that leaves headroom, not a plan that only works in a perfect month.

- Bank statements and management accounts: Lenders want to see trading reality, not just a story.

- Purpose clarity: What the money does, and how it improves the business’s cash position or capacity.

- Director and business credit context: Not always perfect, but explained, with a plan.

If you want to see lender coverage and compare routes quickly, you can browse: Funding Agent’s lender directory, or use the application flow here: Request Funding.

Loan limits and terms

Limits and terms are easy to get wrong because people mix up product types. The British Business Bank breaks this down by facility type.

Facility typeTypical term range under GGSMinimum facility size (scheme rule)NotesTerm loan3 months to 6 years£25,001Commercial affordability still applies.Overdraft3 months to 3 years£25,001Often used for flexibility, not long projects.Asset finance3 months to 6 years£1,000Linked to an asset purchase.Invoice finance3 months to 3 years£1,000Usually tied to B2B invoices and debtor quality.Asset-based lending3 months to 3 years£1,000Availability varies by lender.

If you want to sanity check affordability before you apply, it helps to model the cash impact with the relevant calculator: Invoice Finance Calculator or Asset Finance Calculator.

Security, personal guarantees, and what “your home is protected” really means

A key protection in the scheme is that a principal private residence cannot be taken as security within the scheme. That is helpful, but it does not mean the borrowing is “risk free”.

Lenders can still take personal guarantees at their discretion, in line with normal commercial practice. A personal guarantee is not the same thing as securing the facility on your home, but it is still a serious director commitment.

If you are unsure whether a term loan, asset finance, or invoice finance creates the cleanest risk profile for your situation, compare the structures first: Business Loans, Asset Finance, Invoice Financing.

How to apply (without wasting time)

You apply through an accredited lender (or via a broker who places you with one). The lender does its standard credit and fraud checks, and decision-making is delegated to the lender.

A simple application process that tends to work

- Choose the product type first, term loan vs asset finance vs invoice finance. This stops you applying for the wrong structure.

- Prepare a short “use of funds” note, 5 to 10 lines on what the facility does and how it is repaid.

- Gather documents, typically bank statements, latest accounts, management numbers, and basic director information.

- Compare lender routes, not just rates, also term length, security approach, and speed.

- Apply through the lender, or use a comparison style flow to get matched faster.

If you want to run a single application flow and compare outcomes, start here: Request Funding. If you want to browse providers and then choose who to approach: Lender directory.

If you are new to how Funding Agent works as a platform, this explainer gives the context: What Funding Agent is.

Why applications get declined (and how to improve your odds)

The scheme does not remove underwriting, it supports it. That means decline reasons are often the same reasons you would see on a normal commercial application, just with different risk sharing behind the scenes.

Common reasons

- Affordability is tight, repayments would pressure the business too much in average months.

- Unclear purpose, the lender cannot see how the facility improves stability or growth.

- Weak evidence, missing bank statements, outdated accounts, or numbers that do not reconcile.

- Business in difficulty, signs of insolvency risk, HMRC escalation, or severe arrears issues.

- Subsidy limit issues, prior government support reduces the eligible maximum.

Easy improvements that often help

- Show a simple repayment view, what the monthly repayment is, and what your cash headroom looks like after it.

- Match the facility type to the need, invoice finance for debtor delays, asset finance for equipment, term loan for projects.

- Be honest about bumps, then show control, a plan, and a timeline.

Advantages of the Growth Guarantee Scheme

- Access to higher borrowing limits

- Government backed lender confidence

- Wide product range

- Protection of principal private residence

- Available until March 2026

Potential Drawbacks

- Borrower remains fully liable

- Personal guarantees may apply

- Not automatic approval

- Rates can still reflect risk

Many SMEs misunderstand the 70 percent guarantee. It is not a grant and it is not partial forgiveness.

If GGS is not the best fit, here are the closest alternatives

Sometimes the best outcome is not “GGS at any cost”, it is the right structure at the right speed. Here are the common alternatives SMEs compare against:

- Commercial term loans: Business Loans

- Unsecured working capital: Unsecured Working Capital Loans

- Invoice finance: Invoice Financing and Invoice Finance Calculator

- Asset finance: Asset Finance and Asset Finance Calculator

If you like lender comparisons, these pages reference GGS in a practical way (useful for understanding how mainstream lenders talk about it): NatWest vs Barclays business loans and Paragon vs Close Brothers (asset finance).

Bottom line

The Growth Guarantee Scheme can be a useful route when a lender likes the deal but wants extra risk support. The guarantee helps lenders lend, it does not remove the need for good numbers, affordability, and a clear purpose. If you treat it like a normal application, pick the right product type, and present a clean repayment story, you give yourself the best chance of a good outcome. British Business Bank

If you want to compare options across lenders with one flow, start here: Request Funding. If you are still deciding the right structure, start with: Business Loans, Invoice Financing, or Asset Finance.